TMT deal activity expected to surge, bigger deals on horizon – North America TMT Trendspotter

- M&A volume jumped 40% to USD 502bn in 2024

- AI, fintech, and healthcare IT to see significant activity in 2025

Dealmakers expect a surge in M&A for the North American technology, media and telecommunications sector in 2025 thanks to a more business-friendly environment following last November’s US presidential election.

Mergers and acquisitions in the North American TMT sector saw a rebound in 2024, with volume jumping by 40% year over year to USD 502bn, according to Mergermarket data.

This year is poised to be even better due to declining interest rates, moderating inflation, a solid economy, and the prospect of lower corporate taxes and more favorable regulation under a second Donald Trump presidency, advisers said. Activity is likely to begin slowly but gather pace in the spring once dealmakers are more comfortable with the business outlook, they said.

“People are getting their shopping list ready,” said J. Neely, a senior managing director at Accenture.

To be sure, TMT dealmaking volume last year was still 59% below 2021’s USD 1.22trn and 22% below 2022’s USD 641.6bn. The largest deal in 2024 was the pending USD 33.6bn acquisition of simulation software company Ansys [NASDAQ:ANSS] by Synopsys [NASDAQ:SNPS] last January, followed by the pending USD 20.3bn acquisition of fiber internet provider Frontier Communications [NASDAQ:FYBR] by Verizon Communications [NYSE:VZ] in September.

In the year ahead, “strategic buyers are definitely going to feel more comfortable doing bigger deals,” supported by a more favorable regulatory environment, ample capital on the sidelines, and strong stock performance, said Wayne Kawarabayashi, head of mergers and acquisitions and COO at tech-focused investment bank Union Square Advisors.

M&A interest in tech-company boardrooms has become more robust since the summer, when requests for banks to present market views and strategic alternatives “really picked up,” Kawarabayashi said. But after November’s elections, sellers gained “even more clarity, even more confidence and a willingness to transact,” he said.

Artificial intelligence, cybersecurity, financial technology payment systems, governance risk and compliance, data analytics, and healthcare technology are all areas that will see significant activity, said Kawarabayashi, echoing several other advisors.

Watching Washington

Timing for the wave of deals is in question. Many expect a slow start to the year as companies wait to gain clarity on business performance and Trump’s regulatory picks.

“People are excited, but I wouldn’t say that the pipeline is full,” cautioned Louis Lehot, a partner at Foley & Lardner, during a roundtable discussion in December. The M&A “floodgates” will not open until there is a more sustained interest-rate environment, the window for initial public offerings reopens and the dust settles on the new heads of the regulatory agencies, he said.

Trump chose Gail Slater, who is known for tough enforcement actions against Big Tech but otherwise seen as moderate, to lead the Department of Justice’s trustbusting division, while his choice of Andrew Ferguson to chair the Federal Trade Commission signals a more business-friendly approach to enforcement.

Regulators are likely to move away from exploring novel theories of anti-competitive behavior –prevalent under Lina Khan’s tenure as FTC chair – and toward more traditional antitrust scrutiny, said Accenture’s Neely.

Furthermore, while the IPO market remained largely shut in 2024, there are signs of a reopening. Fintech company Klarna’s US IPO, anticipated in 1H25, points to a more robust market. Others looking to go public likely will wait to report 2024 financials in late February before making a move, said a tech banker.

“If the numbers are great and spending hasn’t slowed, we will definitely see VCs continue to fund companies. On the back of that, we will see more software M&A … probably in late 1Q25 and early 2Q25,” said the banker.

Exit pressure

Pent-up demand for liquidity means that venture capital and private equity firms will look to exit portfolio companies in greater numbers in 2025.

The pace of exits will rise, particularly among venture-backed startups that raised capital at frothy valuations during the height of the market in 2021, Kawarabayashi said. “If they’re continuing to burn capital it’s harder to keep funding them at valuations that still make sense, so there’s going to be pressure to exit.”

The venture capital obsession with AI investments has made it tougher for startups specializing in other technologies to attract capital. “A lot of companies are struggling and need to find a new home either with private equity or a bigger strategic,” Kawarabayashi added.

General partners in venture capital and private equity funds are under pressure to distribute proceeds to their investors. That pressure has grown more acute as the number of exits has declined in the last two years – a function of a persistently wide valuation gap between buyers and sellers.

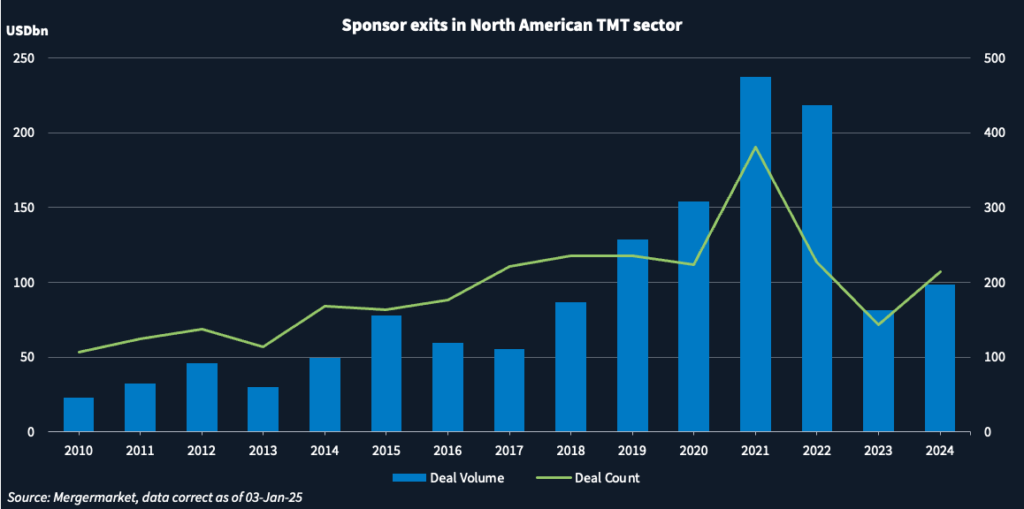

Sponsor-led exits of North American TMT firms totaled USD 98.36bn in 2024, a 21% increase compared to 2023, but still down 59% from 2021’s high and 55% from 2022, according to Mergermarket data. Last year’s biggest exit in TMT was Veritas Capital’s sale in February of a 50% stake in Cotiviti to KKR [NYSE:KKR], valuing the healthcare-data firm at USD 10bn.

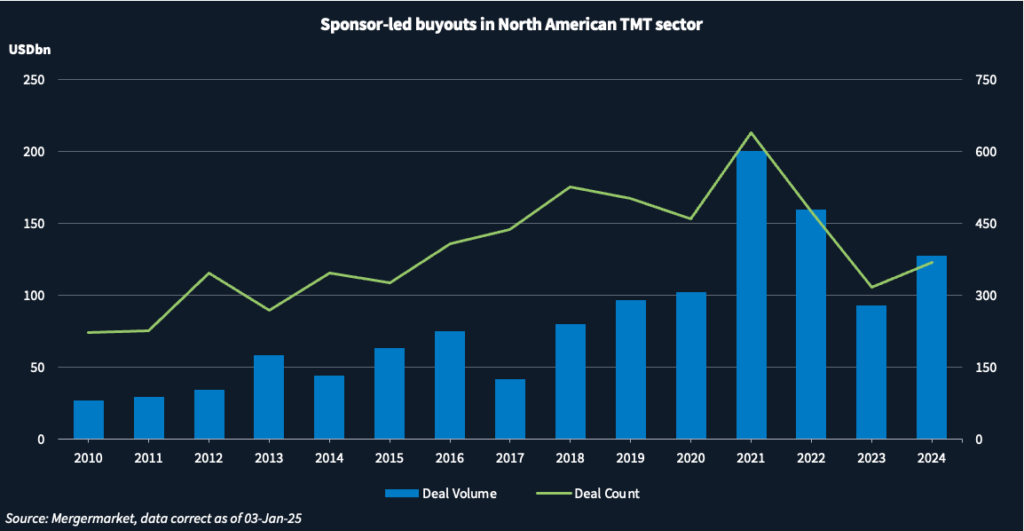

Sponsor-led buyouts of North American TMT companies increased 37% to USD 127.5bn in 2024, making it the third-best year on Mergermarket record since 2010 after the highs of 2021 (USD 200.46bn) and 2022 (USD 159.54bn).

Eyes on AI

AI continues to be on everyone’s minds. Key in 2025 will be the use of AI in specific verticals, such as healthcare or defense, said Natasha Allen, a partner at Foley & Lardner.

Vertical-specific application vendors like Harvey in legal, Cursor in software development and AlphaSense in financial services are companies to watch, according to Mergermarket’s top tech trends for 2025.

‘Agentic software’ companies that can independently perform complex tasks and make decisions will also garner attention, according to the report.

Fintech is another area of TMT that should experience an uptick in activity, especially as the incoming Trump administration continues to nominate crypto- and fintech-friendly regulators.

After regulatory uncertainty and other macro factors dampened M&A activity in recent years, a broad range of strategic acquirers – including traditional financial institutions – want to accelerate fintech adoption within their organizations, said Daniel Kahan, partner at King & Spalding.

Several high-quality fintech names could go public in 2025, including Stripe and Chime, according to Mergermarket‘s list of tech startups expected to have a liquidity event. Crypto-related companies like Chia Network, Circle Internet Financial and Kraken are among those looking to capitalize on the pro-crypto views of the incoming Trump administration.

A service of

Your M&A Future. Today

Explore unlimited content like this, available only in the platform.

Already a client? Sign in