Sterling Group credits sector focus, operations-centric approach for 2025 exit spree

- Recent sale of ADG to Lowe’s is sponsor’s fourth exit of 2025

- Services-centric investment strategy resists economic instability

- Sales to larger financial sponsors are most prolific exit channel

Sterling Group might claim to defy the notion that private equity firms are struggling for liquidity in an uncertain economic environment.

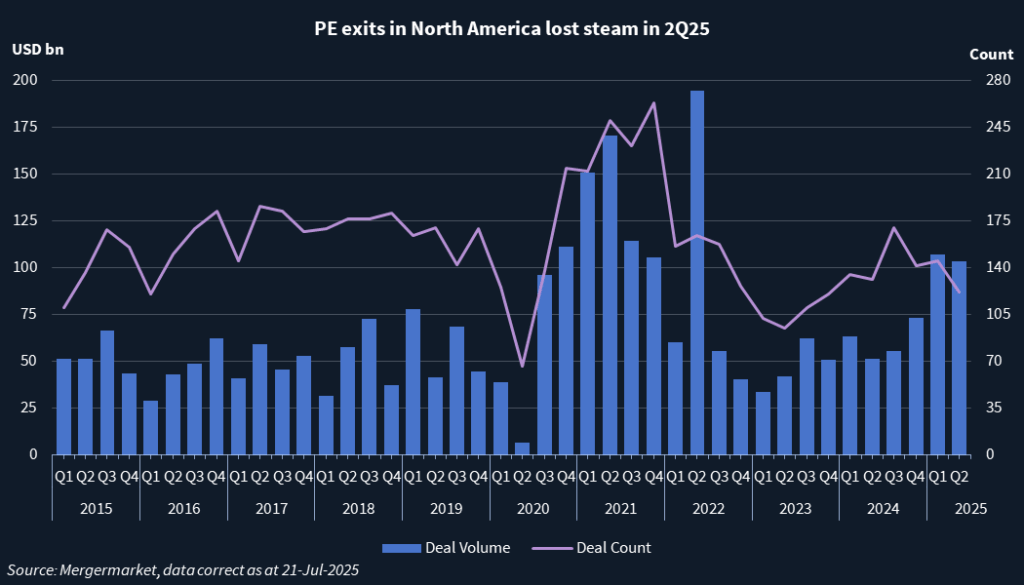

Sponsor-backed M&A exits in North America dropped from USD 107.1bn in 1Q25 to USD 103.4bn in 2Q25, according to Mergermarket data, as tariff turbulence shook the world. Bain & Company warned in its private equity mid-year report that the trend of recent vintages lagging historical benchmarks in terms of distributions could be exacerbated if conditions did not improve.

But Houston-based Sterling has already wrapped up four exits this year, starting with its sale of pavement marking services Frontline Road Safety to Bain Capital in January. Most recently, distribution services provider Artisan Design Group (ADG) was offloaded to retail giant Lowe’s in a USD 1.3bn. That deal was finalized in June.

“We are in a tough market right now,” partner Greg Elliott told Mergermarket in an interview. “You have tariffs, and this uncertainty makes it really tough to get things done, but there are bright spots, and those bright spots are where we’re playing.”

This is an explicit reference to sectors. Sterling is interested in aviation services, utility services, building products, packaging and infrastructure services, and it sees tailwinds in each one. Long-term growth opportunities are believed to transcend any near-term volatility.

The firm is currently deploying its sixth flagship fund, which closed in April 2024 on USD 3.5bn, beating a target of USD 2.75bn. It expects to make 12-14 investments in total. The first one was announced last week: Sterling has agreed to buy Precision Concepts International, a packaging solutions provider, from ONCAP Management Partners.

Operational ethos

Sterling was born in 1982, starting out as a scrappy independent sponsor with its sights trained on opportunities in industrials, and a predilection for corporate carve-outs and investing in family-owned businesses. In broad strokes, it has stayed quite true to these roots, even as assets under management have surpassed USD 9bn.

Many investment committee members have spent decades at the firm. Elliott joined in 1994 and then returned in 2008 following an interlude at Texas-based sponsor CapStreet Group and Encore Aviation, an aircraft charter and maintenance business that eventually became Landmark Aviation.

This longevity means the operational ethos is deeply entrenched – and the firm doubles down by insisting that everyone has hands-on experience of company management.

“Almost all of our investment team has grown up at Sterling, and we require each investment professional to go live and work in a portfolio company for at least a year,” explained Elliott. “They’re reporting to the CEO, and they’re learning how to drive real change in businesses.”

Sterling spent the first 18 years working on a deal-by-deal basis, launching its first institutional fund in 2000. Since then, the firm has raised a new vehicle roughly every five years – the four-year gap between Funds V and VI being a notable exception.

The LP is mostly institutional and global, and it has remained consistent across vintages. When Sterling stepped up from USD 2bn in Fund V to USD 3.5bn in Fund VI, existing LPs absorbed the additional capacity, according to a source familiar with the situation.

The firm’s operational philosophy is captured in a playbook known as the Seven Levers, which outlines distinct areas of development for portfolio companies – from commercial growth and technology adoption to M&A. This filters through to Sterling’s internal set-up, with a partner holding overall responsibility for execution in each of these areas.

In the case of Frontline Road Safety, a pavement marking services business acquired in 2020 via Fund IV, multiple levers were pulled over the course of four years. The sponsor established a new management team and corporate headquarters, which was integral to the completion and integration of 17 bolt-on acquisitions, family-owned companies.

“We were trying to find the best road stripers in the US that are known by states and contractors to be really high-quality businesses,” said Elliott. “Those are the ones that we went after and purchased, and we built them into a much larger business.”

Building conviction

Corporate carve-outs and acquisitions of family-owned companies remain Sterling’s prevalent deal types. Elliott estimates they account for about 75% of investments to date. Transactions tend to be in the USD 100m to USD 1bn range, with the sponsor cutting equity checks of USD 50m to USD 350m.

Carve-out volume has declined in recent years, but Elliott expects it to pick up as more companies potentially look to prune themselves of tariff-exposed unit they may feel better off without.

“There are so many variables there with tariffs and potentially higher inflation,” he explained. “Times of uncertainty and market dislocations have historically resulted in great carve-out opportunities.”

De-globalization intrudes on the family-owned space as well, with Sterling tracking more opportunities that can be linked to difficulties re-orienting supply chains. The sponsor is actively reaching out to owners it has met over the years, asking whether they need help addressing these types of challenges.

Each investment thesis is predicated on being able to look past these issues and identify growth drivers.

Elliott cited road services as an example: as much as 20% of the US road network is in poor condition, which means there are safety issues to address. To this end, Sterling has acquired two regional contracting companies and formed a dedicated payment preservation platform. Much like Frontline, the component businesses operate as regional divisions of a scaled national operation.

In utility services, the firm acted early on the anticipated rise in electricity demand created by the rollout of data centers to support artificial intelligence applications. Finding that up to 70% of the power grid is more than a quarter of a century old, it looked for targets in electric utilities maintenance. This resulted in the 2021 acquisition of PowerGrid Services.

“We feel like in this market, you need to make your own luck, so we’re working hard to be very creative and finding platforms in each of these buckets,” said Elliott. Earlier this year, Apollo Global Management agreed to buy a majority stake in PowerGrid Services for an undisclosed sum and support its continued growth. Sterling retained a minority interest.

The path to exit

Exit planning begins as soon as an asset is brought into the portfolio. Part of this process involves outlining the potential universe of buyers within the sector and engaging with them early on.

“We’re outlining the industry, we’re getting to know the strategic buyers because you have to develop those relationships,” said Elliott. “Those Lowe’s of the world need to have someone who really wants to stick their neck out to make the acquisition.”

Many of the buyers Sterling sells to are large sponsors, with sales to strategic investors in the minority; Elliott estimates there is a 70-30 split. Of the four exits announced this year, three were sales to other financial sponsors. ADG was the only asset to go to a strategic investor.

Sometimes, being proactive on exits leads to an early liquidity event. West Star Aviation, an Illinois-based maintenance, repair, and operations (MRO) business housed in Fund V, is a case in point.

During a three-year holding period, Sterling helped grow EBITDA from about mid USD 30m to USD 100m. This was achieved by consolidating non-original equipment manufacturer (OEM) vendors and renegotiating pricing, as well as by executing two add-on acquisitions. Greenbriar Equity Group bought the business for around USD 1.5bn, as reported.

The compacted timeline for West Star – the shortest hold of the four exits so far this year – is atypical. According to Elliott, it was a natural consequence of realizing a five-year value creation plan ahead of schedule.

“We’re doing all the preparation work to make that process go smoothly,” he said. “It’s not just ‘time to sell, let’s put some lipstick on it’. That’s not the way it works.”

A service of

Your M&A Future. Today

Explore unlimited content like this, available only in the platform.

Already a client? Sign in