North America PE Trendspotter: Buyouts start to bounce back, market awaits exits revival

- 1H24 buyout activity in North America increased 45% versus 1H23

- PE exits remain low but secondaries and continuation vehicles become popular alternatives

- Further PE deal and exit rebound expected in 2025

North American private equity (PE) activity began to stage a comeback in 1H24, according to Mergermarket data. But with exits yet to come through in any significant quantity from assets sitting at high valuations in 2020- and 2021-vintage funds, market participants are not expecting a rush back to the dealflow volumes seen in 2021 and 2022.

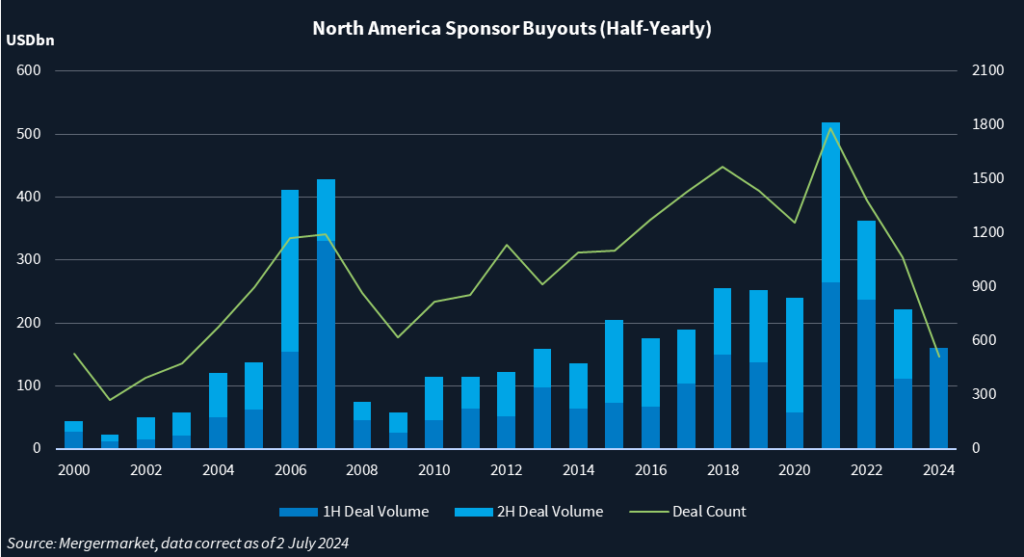

Sponsor buyout activity in North America totaled USD 160.9bn in disclosed deal volume in 1H24, according to Mergermarket data, a 45% increase versus the same period last year. Buyouts in 2Q24 totaled USD 89.7bn, an 83% rise compared to 2Q23 and the greatest deal volume seen since the USD 108.7bn achieved in 2Q22.

Leading the resurgence were blockbuster takeovers including Silver Lake and Mubadala Investments’ USD 14.8bn acquisition of Endeavor Group in April and the USD 12.3bn acquisition of Truist Insurance by Stone Point, Clayton Dubilier & Rice, and Mubadala in February.

Tech buyouts race accounted for 44% to the overall buyouts volume in 1H24, led by private equity giant KKR’s [NYSE:KKR] USD 10bn purchase of a stake in health tech firm Cotiviti from Veritas Capital.

Key assets in the auction pipeline for the rest of 2024 include Bridgepoint-backed financial software provider Kyriba, Carlyle-backed power generation company Cogentrix, KKR-backed GeoStabilization, and Lone Star Funds’ exploration of an exit of resins and specialty materials maker AOC, as reported by this news service.

But PE still has a long way to go to recover from the dealmaking drought, cautions David Humphrey, global head of TMT and co-head of Bain Capital’s North American PE team.

Deal activity has made a slower comeback than Bain anticipated, he said. “Some of the headwinds to more transaction activity are still – especially for larger transactions – helping buyer and seller expectations to meet.”

Exit wave still to come

PE exit activity rose by 10% in 1H24 versus 1H23, to USD 98.8bn in disclosed volume, led by Berkshire Partners and Leonard Green & Partners USD 18.2bn sale of SRS Distribution to Home Depot.

Still, when compared quarterly, the sector totaled USD 44.3bn in 2Q24, falling below the totals of 4Q23 and 1Q24 which recorded USD 53.1bn and USD 54.4bn respectively.

Sponsors are still monetizing assets that they purchased during the large spike in activity during 2020 and 2021, meaning that the majority of assets being sold on the market right now were likely purchased in 2018 and 2019, he noted. Bain recently realized a portion of its stake in growth cybersecurity business ExtraHop Networks, purchased in 2021, and also monetized a portion of its position in cloud infrastructure software business Nutanix.

So far the market has seen less realization of the 2020 and 2021 vintages, Humphrey added, but he expexts to see more of that wave should equity and credit markets remain strong. he adds.

That pressure to make more exits has led an increasing number of GPs to turn to the secondary market in the form of continuation funds, or GP-led secondary deals.

“It’s a smaller part of our business but I think as a result, it’s one that will see actually significant growth in the coming years on a relative basis,” says Mark Chamieh, managing director and global head of business development for PGIM Private Alternatives, said of the firm’s budding secondaries arm. PGIM purchased Swiss secondaries manager Montana Capital Partners in 2021 to enter the sector.

“We find investors like the fact that they have a way to negate the J-curve when they’re investing the funds…and I think generally they like the return dynamics of the secondary space for PE,” he adds.

“Continuation vehicles have certainly picked up, and continue to pick up as an exit avenue for GPs,” says Jared Davidson, a managing director at private capital advisory firm Asante Capital. “I think a number of LPs have gotten comfortable with them so long as there is alignment and no conflicts of interests between GPs, LPs and secondary buyers.”

Continuation funds in the pipeline include one by NewSpring Capital‘s vehicle for two assets held via its Growth Capital strategy, as reported.

Tough times for fundraising

Despite these emerging liquidity solutions, the slow exit environment has helped fuel a shift in power from GPs to their investors as LPs become more selective in the face of lower distributions.

“Because of the absence of an IPO market and the absence of significant exits, funds are having a hard time returning capital to limited partners, and that’s got to turn around,” says Alan Wink, managing director of capital markets at Eisner Advisory Group Eisner’s Wink. “With interest rates still relatively high, these LPs have alternatives where they can put their money.”

There has been a “flight to quality” as investors reassess how much risk they are willing to take now that the period of frothy valuations in 2021 and 2022 has come to a close, he adds. Only top performers are raising capital from LPs in the current environment.

The largest fundraises in 1H24 included Silver Lake’s closure of its seventh flagship fund at USD 20.5bn in May, Vista Equity Partners’ reported USD 20bn close of its eight flagship fund in April, and TPG’s reported USD 15.6bn fundraise, which closed in April.

While these megacap vehicles have closed successfully, the cutthroat fundraising environment has been particularly felt by middle-market buyout shops, says Asante’s Davidson. LPs are less willing to take on new relationships in this market segment and have already “made their picks” in many cases, he said. The firm has been seeing GPs have success with cross-border offerings, however, such as US GPs raising capital outside the US and vice versa, he added.

Nevertheless, sentiment has started to shift over the last few quarters, he noted. A survey conducted by the private markets placement firm found that 75% of LPs expect higher distributions in 2024 compared to 2023, and 72% of LPs plan to increase their PE exposure.

Even with the slowdown in fundraising, GPs are under pressure to deploy more capital. “Because M&A, and therefore deployment, has subsided over the last few years, financial sponsors have quite a bit of dry powder to put to work,” says Davidson.

Looking forward to 2025, Bain Capital’s Humphrey predicts that “we will see some continued increase in deal activity and, for at least a period of time, continued good economic outlook.”

“We’re just finding that it’s an environment right now where it requires a little more creativity to make deals happen,” he says. “You’ve got to have real insight and you’ve got to be able to support the businesses to drive growth because you’re gonna be buying them with higher cost capital structure than it would have been a few years ago.”

A service of

Your M&A Future. Today

Explore unlimited content like this, available only in the platform.

Already a client? Sign in