Missed Congeniality: Phantom mandates warp M&A pipeline, beauty parades

Investment banks, advisory firms and vendors have always made informal soundings with vendors and buyers alike to drum up new business. Nothing new there.

But against the backdrop of the rising cost of capital, dried up deal flow and consequent fee pressure, such conversations are increasingly accompanied by a whiff of Oscar-worthy theatricality on both sides of the pond.

To spur buyside interest and provoke vendors into considering otherwise unplanned sale processes, some bankers are testing market appetite for assets while maintaining the charade they have a formal mandate, dealmakers have told Mergermarket.

The result is a distortion of the dealmaking landscape and, with it, the fairness of the traditional beauty parade, advisors have argued.

Informally shopping assets is “giving the impression [to market participants] that there is a process when, in fact, it is the banks trying to position and get ready for a sale process,” said one consultant that works on due diligence.

“On occasion, we’ve had instances where two investment banks have reached out to us on the same asset and asking us who would be the buyers – which makes us think – who is advising?”

Of course, there are risks attached. “Some advisors are burning bridges because of this – it’s super dangerous and a very risky business, but the opportunity cost is massive. You can see why people want to do it,” said one senior banker.

Given the choice of stoically accepting the moribund deal conditions – and perhaps less stoically the consequently reduced fee and bonus pools – or rolling the dice, some advisors are clearly opting for the latter.

Perhaps it’s a generational thing? “It's seen more among the younger crowd,” said another, seasoned, banker. “This in some cases can really burn relationships,” he cautioned.

Attempting to seek the upper hand by pitching assets at ludicrously rich valuations and subsequently overstating how much buyside interest they could really gather is one tried-and-tested route of riling clients, he added.

Of course, reputational damage with clients is only one side of the coin, two further bankers argued. It’s not just about getting caught – there is simply an ethical barrier to any decent advisor indulging in sharp practice, they both noted.

Nonetheless, combining the claim – or implication – of a formal mandate with the promise of some financing muscle can be effective in bringing both sides to the table, one of these bankers conceded.

In some instances, banks are not only claiming to hold formal mandates but are also attempting to offer assurances to prospective sellers by raising the possibility of staple financing packages, the same banker said. With appetite for risky bonds and loans tied to leveraged buyouts still comparatively muted, the offer of staple financing can sway possible deals, he added.

No fee lunch

The latest wave of affect is mostly derived from the heavy drop in opportunities for banks to land new advisory roles – and the associated fees.

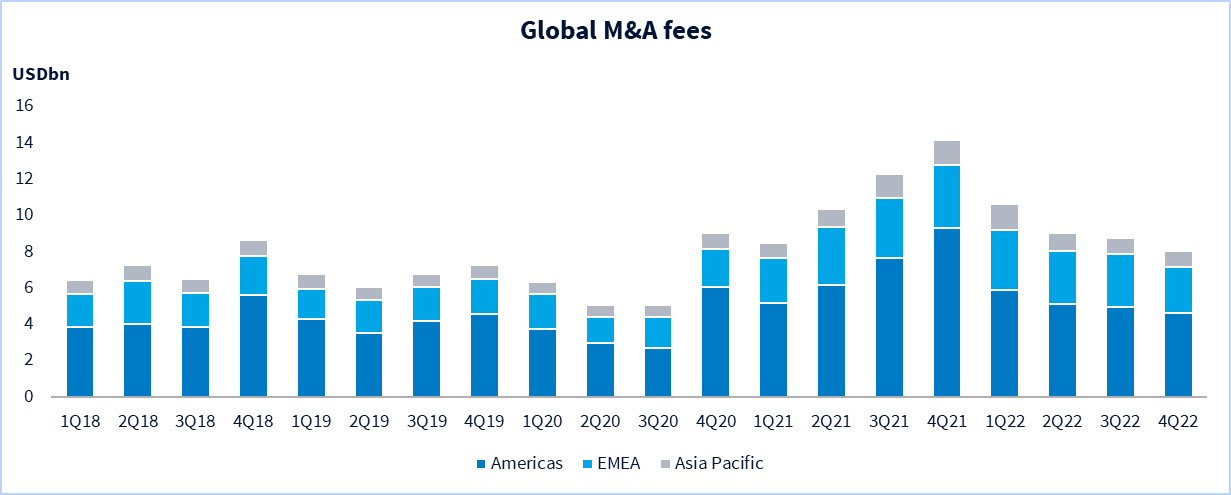

Global dealmaking fees for M&A – a reflection of the volume of advisory mandates from both buyside and sellside roles – totalled USD 8bn in 4Q22, the lowest collected in a quarter since 3Q20, according to Dealogic data. At USD 16.8bn, fees collected in the second half of 2022 dropped 14.6% compared to the USD 19.7bn reaped in the first six months of the year.*

Source: Dealogic (Data correct as of 2nd March 2023)

So the motivation for some bankers and advisors to overstate their mandate status in an effort to get parties talking is clear.

Yet while vendors and sellers will complain over the use of offbeat methods to drum up business, some benefits of informality appear to work both ways. Indeed, shopping assets around off-books seems in part to in fact be driven by a number of wannabe vendors.

“No one wants to be officially for sale for the time being, so you end up with a situation where the sellers just go to one banker, or their preferred or trusted advisor, and says ‘I’m not officially for sale, but please sound out the market and if you find interest at this price, then I am a seller,’” said one banker.

If news of the bank’s efforts in such circumstances breaks in the wider financial community, the vendor can clutch their pearls with plausible deniability.

“A lot of sponsors are keen for banks to be actively shopping assets”, said one of the bankers. “It saves them the work [of having to make an appointment]. But the risk is that the sponsor will then say ‘okay, you mandate the buyside and we’ll appoint [another bank] to do the sellside,'” they added.

Further distorting the standard dealmaking playbook is the narrowing of beauty parades, as both buyers and sellers try to limit noise around a potential transaction, according to several bankers.

“The main difference between now and 18 months ago is that there are very few beauty contests for pitches, where the seller invites ten investment banks and chooses from them. Because when you do that, nine of them will be disappointed and could spread around in the market that your company is for sale,” according to one banker.

While the macroeconomic environment remains so chilly, the devil will make work for idle hands – and bankers with a penchant for amateur dramatics – to do. But putting assets out there “for your consideration” without vendor backing may yet see a client jump the stage to give you a slap.

by Charlie Taylor-Kroll, Ryan Gould, Dominic Pasteiner, Rachel Lewis and Min Ho, with analytics by Jonathan Klonowski

*As per Dealogic methodology, 90% of the fees charged for an M&A transaction are allocated upon completion.

A service of

Your M&A Future. Today

Explore unlimited content like this, available only in the platform.

Already a client? Sign in