Australian private equity investors await better exit opportunities

For private equity (PE) investors in Australia, waiting for the exit window to open is a bit like staying in the Eagles’ Hotel California. “You can check out any time you like, but you can never leave.”

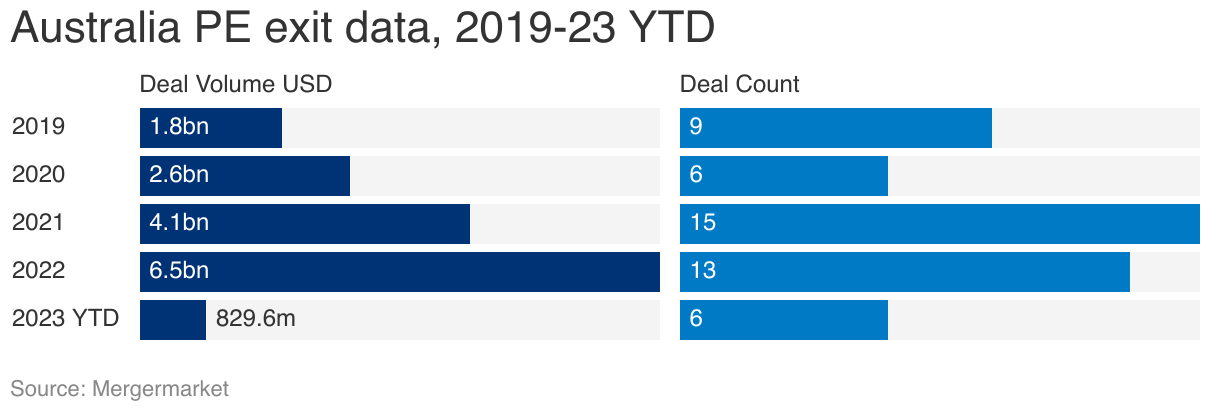

According to Mergermarket data, Australia’s private equity exit deals in 2023 year-to-date (YTD) slumped to a 10-year low in volume and a five-year low in deal count. The six deals totalling USD 829.6m represented a dramatic drop compared with USD 6.46bn and USD 4.09bn for the same period in 2022 and 2021 respectively.

With the first half almost up, it is hard to expect 2023’s full year numbers to catch up with those of previous years: USD 13.2bn in 2022 across 26 deals and USD 13.8bn in 2021 across 38 deals.

Australian PEs traditionally hold their portfolio companies for three-to-five years before an exit, either through a public float or a sale, but the norm may be shifting. Of the 49 PE-backed companies with a Likely-to-Exit (LTE) score higher than 50 in Mergermarket’s LTE model – a proprietary algorithm that predicts the likelihood of an exit in the next 12-to-24 months – more than half have been held for at least four years and 22 have been held for five or more years.

Remember when Quadrant Private Equity managed to list online beauty retailer Adore Beauty on the ASX in October 2020, one year after the sponsor first invested? Those days are gone.

Foggy prospects

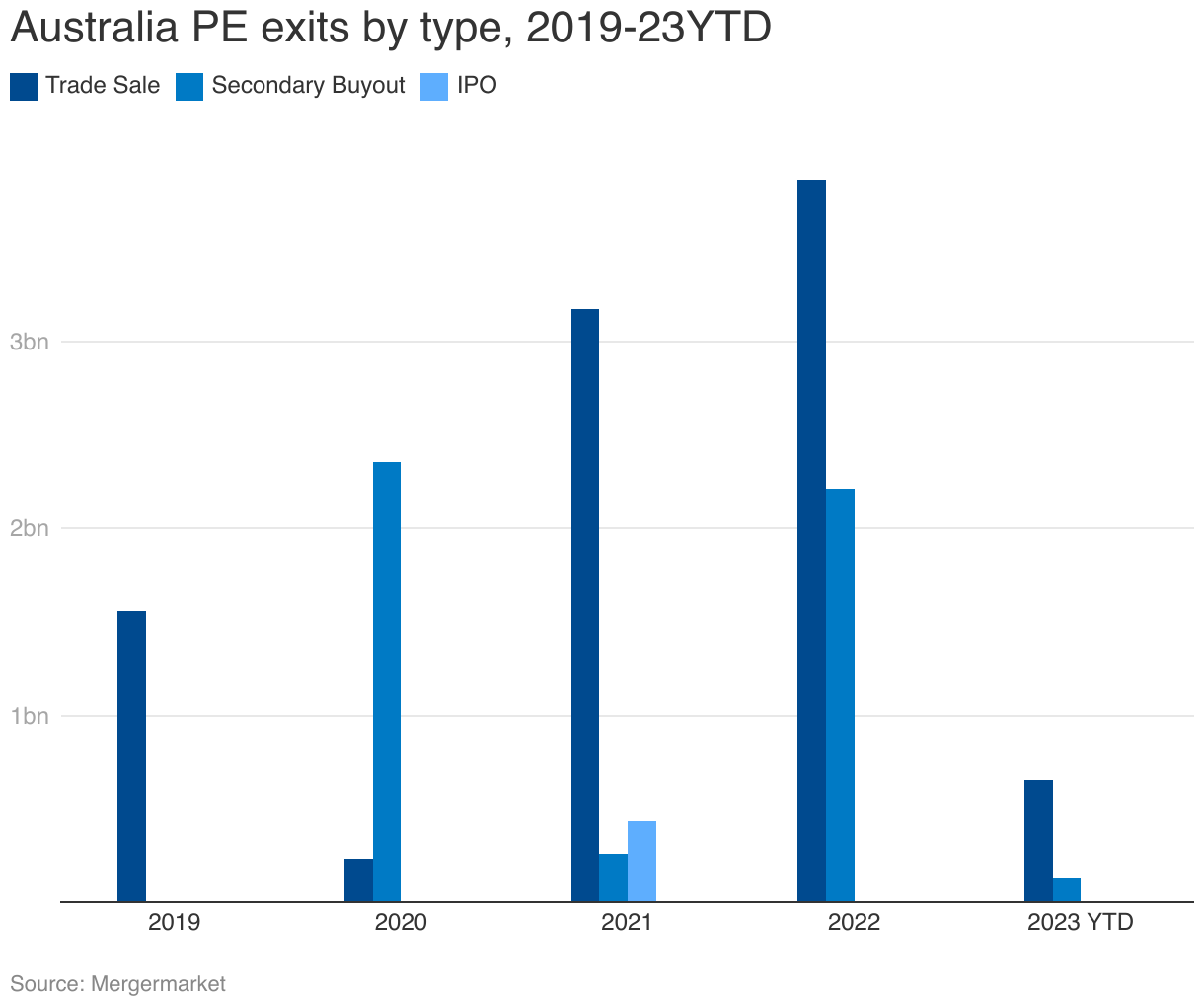

The weakness of the IPO market is one reason. Australia has not seen a float worth more than AUD 100m since the start of 2022. The last sponsor-backed company to debut on the ASX was Siteminder, a hotel booking software business backed by Technology Crossover Ventures (TCV), in October 2021.

Another factor restraining large private equity exits is the lower availability of debt, particularly US Term Loan B debt, according to a Sydney-based PE dealmaker. Although local banks are open for business, larger deals require a greater quantum of debt beyond the capacity of Australia’s “big four” banks, he says. A private credit source recently noted that debt providers are now looking more at refinancing instead of lending on new deals.

The largest exit this year is the AUD 635m (USD 443m) sale of Onsite Rental Group by Next Capital to Malaysian investment holding firm Sime Darby [KLSE:4197]. In the previous two years, 11 exits worth more than USD 1bn took place.

Economic uncertainty caused by rising interest rates and softer consumer sentiment has also made it harder for PE managers to find an exit path.

Waiting in the wings

While they wait for the right time to exit, PE managers often refinance buyout debt or put in more equity. Last month, medical device distributor Device Technologies held talks to refinance the AUD 388m in secured amortizing loans due 2024 used in Navis Capital Partners’ 2019 buyout. Also last month, Real Pet Food Company’s sponsors injected AUD 248m in equity to partially pay down AUD 475m in debt due 2024 and to fund growth.

Some PEs are also exploring continuation funds to roll over their assets, as flagged by Mergermarket last September. Crescent Capital planned the formation of a continuation fund to acquire and hold its healthcare staffing business Healthcare Australia, local media reported in March.

Even when sponsors appoint advisors for an exit, they take their time to launch a process. The sale of Guardian Childcare and Education will not officially start until the second half of 2023, even though Partners Group first appointed Morgan Stanley as sellside advisor in February.

The Growth fund alone has appointed sellside advisors for four portfolio companies in the past three months: GoGet, CompassCorp, Quantum Radiology, Ekera Dental, as reported. How long they drag their heels will be telling.

| Portfolio company | Financial Sponsor | LTE score* | Sector | Years held |

| Hy Gain Feeds Pty Ltd | Adamantem Capital Pty Ltd | 81 | Consumer & Retail | 5 |

| Teg Pty Ltd | Mercury Capital (Australia) | 80 | Consumer & Retail | 3 |

| Tribe Breweries Pty Ltd | Advent Partners Pty Ltd | 75 | Consumer & Retail | 5 |

| Affinity Education Group Ltd | Quadrant Private Equity Pty Ltd | 74 | Business Services | 1 |

| Craveable Brands | PAG Asia Capital Ltd | 71 | Consumer & Retail | 3 |

Source: Mergermarket

*Note: Mergermarket’s Likely To Exit (LTE) predictive algorithm is based on a number of key industries, holding behaviors, and deal flow criteria. The algorithms assign a score to each exit opportunity, with a higher score corresponding to a higher likelihood of an 12- 24 months transaction.

A service of

Your M&A Future. Today

Explore unlimited content like this, available only in the platform.

Already a client? Sign in