Apollo off to the races in 2025 with over USD 2.4bn of equity deals

- Apollo ECM issuance hits USD 2.4bn in deals this year

- Aspen Insurance IPO, Lottomatica trades show calculated exit push in volatility

- OLB sale exemplifies case-by-case monetization play

At a time when many sponsors are growing nervous about returning capital to limited partners, few have acted as decisively as Apollo Global Management in utilising equity capital markets for disposals.

Apollo-linked ECM issuance so far in 2025 totals around USD 2.41bn across six deals. This includes three block trades in Italian gaming company Lottomatica and two US equity sell-downs in ADT and Sun Country Airlines.

* source: Dealogic

The sponsor has also been active in the US IPO market with the USD 457m New York listing of Bermuda-based insurer Aspen. Aspen, taken private by Apollo in 2019, specializes in complex and specialty reinsurance products across global markets. It returned to public markets in 2025, more than six years after delisting, raising USD 397.5m at the midpoint of its USD 29 to USD 31 range. The IPO, which valued the insurer at about USD 2.76bn, saw shares debut 10.8% higher, giving Aspen a market capitalization of roughly USD 3.05bn. Post-listing, Apollo retained an 82.1% stake.

The listing had been long anticipated and benefited from strong institutional awareness, having been on file publicly for some time.

Despite market volatility, the process attracted broad support from long-only and hedge funds, and the valuation was considered measured and appropriate for those challenging conditions, one ECM banker familiar said. The deal, anchored by large institutional accounts, was more than 10x oversubscribed.

The listing held firm despite the volatility that followed US President Donald Trump’s tariff announcements, helped by a well-structured transaction and realistic pricing. It was also the result of a long preparation cycle.

Apollo’s capital markets and syndication team is led by managing director Michael Shapiro, who sits within Apollo Capital Solutions (ACS) and is responsible for driving exits via IPO and co-investment strategies across the platform.

Prior to joining Apollo in 2021, Shapiro was a director on KKR’s public equity capital markets team, where he was responsible for leading the advisory and execution of equity transactions globally. He was previously a director in the ECM team at Wells Fargo.

Apollo is known for lining up execution paths well in advance, but also for moving quickly, and some will say unexpectedly, when conditions allow, the ECM banker and other market participants said.

Shapiro’s team plays a central role in that process, operating across Apollo’s equity, hybrid, and credit strategies. The team sits in on private equity investment committee meetings and works with deal teams to provide a capital markets overlay during underwriting, embedding exit strategy considerations right at the moment of investment.

This includes participating in leadership pipeline meetings and helping to shape execution plans, spanning IPOs, block trades, and other ECM tools. Apollo has shown an ability to execute by combining its value creation plans with capital markets strategy. Typically, once a deal closes, the sponsor introduces its deal teams to investors to start deepening these relationships and establish further credibility.

Apollo evaluates each deal across a wide range of options, including IPOs, strategic M&A, sponsor-to-sponsor sales, continuation vehicles, and minority stake sales.

“From a public markets perspective, we see this as a continuation of the private equity investment – almost a second life for the company,” Shapiro told this news service. “Our goal is to create value not just for our investing LPs, but also for the public market investors who support the companies at IPO, and to drive meaningful returns as the company transitions from private to public ownership.”

The sponsor could be active in the IPO market again, with the listing of German online automotive parts retailer Autodoc, as reported, in which it acquired a minority stake in April 2024.

Apollo owns its position via its Hybrid Value Fund. The Hybrid Value platform offers flexible capital, typically convertibles or preferred equity with warrants, to sponsors facing difficult exit environments. These bespoke structures offer win-win transactions for sponsors seeking liquidity with less onerous terms than traditional credit investments, he said.

However, regardless of its set-up, Apollo has shown itself to be nimble in pivoting when necessary.

One of the sponsor’s listing candidates for 2025 was German lender OLB, also known as Oldenburgische Landesbank, a perennial IPO candidate in recent years. A deal was being readied for launch in March to take advantage of Europe’s traditional pre-Easter window.

On the day the deal was set to be launched, Apollo and other shareholders opted instead to sell the business to Crédit Mutuel Alliance Fédérale. Sources close to the deal at the time were surprised, but market participants say the decision was in line with Apollo’s case-by-case approach and the optionality created by early IPO prep work.

With monetization windows tightening across the industry, Apollo has balanced urgency with preparation.

The assets they can monetize, they will. “Apollo is a highly engaged sponsor, which in our experience is always looking at the full spectrum of exit strategies, be it through ECM, M&A or minority investments,” said the same ECM banker who has worked with the sponsor.

Shapiro maintains direct relationships with mutual funds, hedge funds, and bank equity desks, engaging public investors soon after acquisition to build credibility and surface early feedback.

Market participants describe Apollo as constructive and active, often willing to adapt terms to suit market conditions.

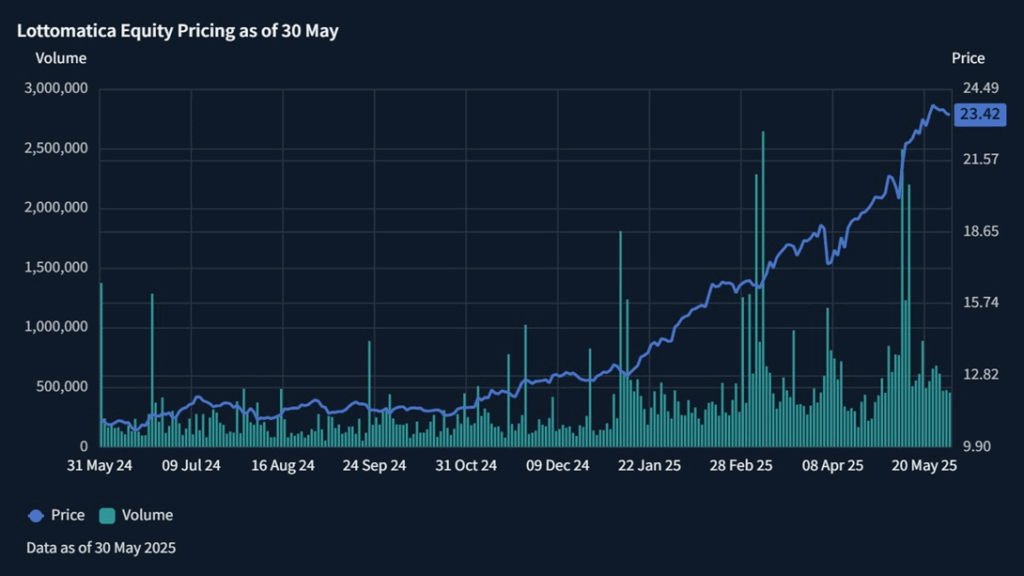

Lottomatica’s winning streak

The sponsor’s Lottomatica disposal in particular serves as a model for how to use ECM to quickly and efficiently sell down portfolio companies.

Apollo bought the company, then Gamenet, in October 2019 for EUR 950m from International Game Technology. It listed the company in April 2023 at a steep discount to Entain, seen at the time as its closest listed peer.

The deal was a mostly primary affair, with Apollo only selling 19.4 million shares, including a greenshoe, according to Dealogic, worth around EUR 174.6m at the offer price of EUR 9 a share. The structure of the deal was designed to get an aftermarket pop, but even with a steep discount the deal fell in the aftermarket. Even though the stock initially fell post-listing, Apollo saw the IPO as just the beginning of the monetization journey.

“Investors tend to see Apollo as very realistic on valuation,” said the banker. “It doesn’t tend to overplay.”

A second banker close to the Lottomatica deal, at the time bemoaned, that even at a screamingly cheap price, the European IPO market seemed inextricably broken. But in structuring the deal the way it did, Apollo was able to play a longer game, in the full knowledge that once the firm proved itself through its earnings as a public company, investors would see the value.

“We often see overlap among the investors who look at our various transactions, particularly over the last two years, as they’ve continued to have positive experiences. I think that really speaks to the performance of our Apollo Funds’ companies and the thoughtful approach we take to monetizations,” Shapiro said.

This thesis has proven right. Within a year, Lottomatica was up 17.3% from the IPO price and, as of May 2025, is up over 150% from the IPO price and has risen by around 75% this year. Apollo’s last sell-down, a deal on 9 May, was its sixth block trade of Lottomatica since the IPO.

* source: Dealogic

The secondary deals have provided EUR 1.7bn of proceeds for the sponsor, which, when combined with the smaller IPO proceeds, represents a huge return on its initial EUR 950m investment. Apollo still owns around 53.6 million shares in Lottomatica, even after the last block trade, worth a further EUR 1.2bn as of the Italian company’s closing price on 14 April.

The sponsor’s remaining stake is held in its Gamma Intermediate S.à r.l. vehicle, a company incorporated on behalf of funds managed by its 2017-vintage Apollo Management IX, at the time its largest fund ever raised at USD 24.6bn.

Since 2023, Apollo Funds have sold over USD 11bn of stock in the equity market globally, Shapiro said.

A service of

Your M&A Future. Today

Explore unlimited content like this, available only in the platform.

Already a client? Sign in