Water P3s bubbling up in US

Water authorities in the US are starting to embrace public-private partnerships in response to expanded federal incentives, water shortages and the urgent need to replace aging plants and systems.

Earlier this month, the Fort Lauderdale city commission selected a group led by IDE Technologies, Ridgewood Infrastructure and Kiewit to develop a new water treatment plant for the South Florida city under a P3 agreement. The P3 follows a November decision by another Florida city, Riviera Beach, to use a P3 to build a new treatment plant.

Santa Clara, California, meanwhile, is running an expedited search for a partner for a purified water program and selected three finalists late last year.

“I know the community will benefit from it, and we’re really excited that we’re able to finally to take that next step to provide this community clear water and a safe water plant that will withstand the Category 5 hurricane that we’ve talked so much about,” Fort Lauderdale Mayor Dean Trantalis said after the vote to go forward with the P3.

Changing politics

For years, political and legal roadblocks have kept many local water authorities shy of exploring private financing options even though studies have argued that the aging water infrastructure in the US is ripe for P3s.

Only a dozen or so states allow P3s for various aspects of water infrastructure, but they include some of the largest—California, Texas and Florida. States including New Jersey and Arkansas expanded P3 legislation in the last decade.

Now more states, including Illinois and Mississippi, have legislation pending that would make at least some water P3s legal. And the market is likely to grow because of the intersection of need and opportunity, experts say.

By some estimates, the US needs to invest USD 80bn to USD 109bn per year to upgrade water infrastructure over the next two decades. Leaking water mains, outmoded, failing water-treatment plants and a scarcity of fresh water sources for growing areas are just some of what will require attention.

While last year’s federal infrastructure act provides some funding, the amount—USD 55bn over a decade—is dwarfed by the need, says David Totman, an officer of the American Society of Civil Engineers and an executive at water software company Innovyze.

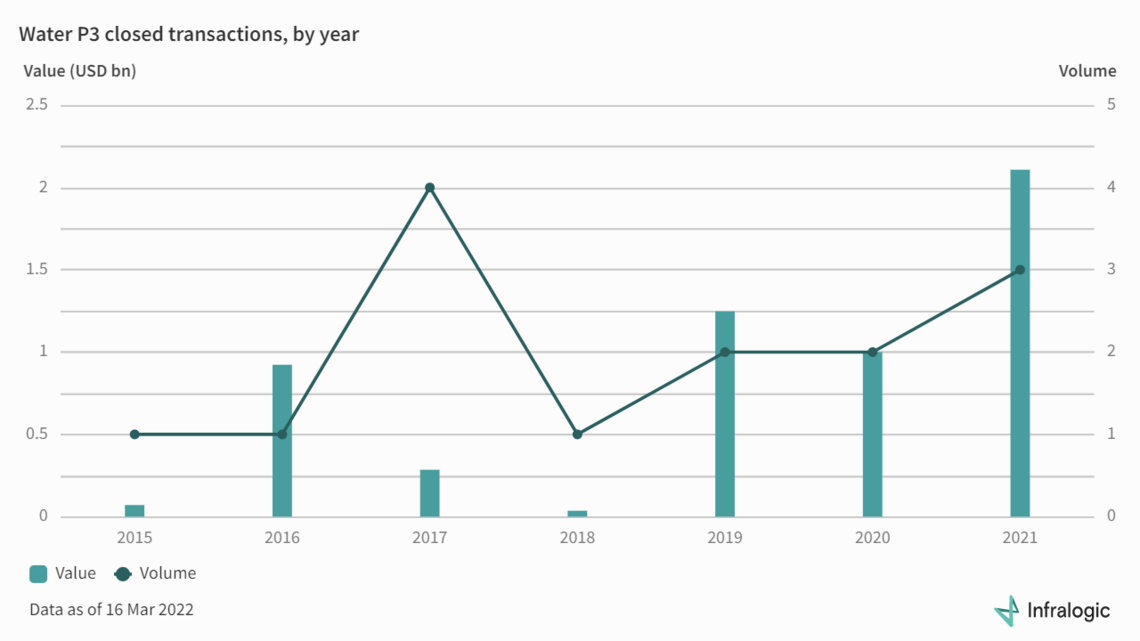

Infralogic has tracked 51 new water, wastewater or desalination P3 projects in the US since 2015, with the number of new projects launched coming in the high single digits or low double digits each year.

Of those projects, 10 of the transactions ended up being cancelled and another 10 were put on hold. The first year of the pandemic saw two projects cancelled, with another two cancelled in 2021, according to Infralogic data. A few of those projects, such as the Santa Clara purified water project, have since been resurrected.

As they gain a track record operating successful water P3s in the US and use these successes as case studies, companies are more able to convince political leaders the funding model is right for their communities’ water infrastructure, says Jeff Murphy, managing director for infrastructure at Ullico Infrastructure Management.. And with a “political champion,” a P3 proposal is more likely to move forward, he says.

Cities like Lake Oswego and Portland, Oregon, which are collaborating on a P3 project for stormwater, are opting for P3s to help manage the risks of cost overruns and construction delays.

“The capital investment costs are very high and sometimes having a major company, a major developer coming in, brings both the talent and then the funds” to do the work, says Seth Lehman, senior director for FitchGroup’s Global Infrastructure and Project Finance Group.

Sticker shock

Water infrastructure investment often lags because people expect to pay minimal rates for water, making it harder for municipalities to raise rates to fund infrastructure upgrades.

“It blows my mind that we will pay USD 4 for a 12-ounce bottle of water at the local convenience mart, but yet we scream when we pay USD 1.50 for 1,000 gallons of tap water,” Totman says.

“Rates haven't kept pace with inflation, so that's the trap that the municipal operations end up running into, is politically they don't have the will to keep rates where they should be,” says Ullico's Murphy.

Some water authorities, like San Antonio Water Systems, have been able to increase rates to fund P3s without much blowback. The Texas city used a P3 to build the Vista Ridge pipeline, which expanded the area’s water supply by 20%.

Fort Lauderdale boosted rates to support new infrastructure even before the city decide to proceed with a P3 after citizens became fed up with yellow water and other problems. Even so, Vice Mayor Heather Moraitis and Commissioner Robert L McKinzie voted against the P3.

“I still struggle with privatization of water,” McKinzie said at the March commission meeting, pointing especially his fears that city water employees would have to become employees of the private contractor. City officials have said the employees can remain on the city payroll if they wish.

52,000 local systems

Beyond politics, P3s for water sometimes have been slowed by the sector being broken up into 52,000 local public agencies in the US.

“It's a highly fragmented market, and because of that, it's harder to get off the ground,” says David Bird, vice president for project finance and development at Kansas-based Garney Construction, which focuses on water and wastewater infrastructure construction and built the Vista Ridge pipeline.

On the other hand, the smaller size of some water authorities also can make setting up a P3 an easier task, because “you can usually kind of get everyone in a room” to agree on how to proceed with a project, Ullico’s Murphy says.

Smaller water systems are finding it more difficult to meet the regulatory needs for water testing and decontamination, pushing them to consolidate or work with larger systems and consider P3s, water experts say.

Growth areas

Regions facing increasing drought, such as the West Coast and Texas, are looking at new ways to add to their water supply, including treating brackish water and using desalination plants. While both types of projects have been built using P3s, brackish water treatment is the less complicated of the two solutions and so more likely to see faster growth.

Increased federal funding for programs like loans under the 2014 Water Infrastructure Finance and Innovation Act could help to spur more P3s, while supporting current ones such as Rialto Water Services, an SPV owned by Ullico and Table Rock Capital and run by Veolia under a 30-year concession.

The transportation infrastructure loan program that WIFIA’s modelled after, TIFIA, has spurred scores of P3s in the transportation sector. Those in the water industry see WIFIA eventually helping to do the same for water because of its authorization to provide low-cost loans for water projects, including P3s.

As more financing becomes available through programs like WIFIA, recognition by the public that more needs to be invested in water and advocacy by political leaders should help to enlarge the market, some in the industry say.

Ultimately, key to the market is municipalities and developers successfully completing projects.

When one project is stalled or cancelled, that can have a ripple effect on the attractiveness of P3s. Until the market matures, companies hoping to invest or work in water P3s won’t be able to rely on them for a steady income stream.

“If the parties are less convinced that there's going be a project there right there, less certain that the politics will play out in the right way, people will be more reluctant to show up,” says Bird, who adds that this company could not survive only on the P3s it handles. “But if there's so few P3s in our space, people have to show up, no matter what.”

[widget id="12249" widget_title="Events | Infrastructure"]

A service of

Shape your future with Infralogic. Today

Explore unlimited content like this, available only in the platform.

Already a client? Sign in