Iran war may blow Asian offshore wind back on course

- North Asia accelerates renewables agenda, with offshore wind as a key component

- Reality of offshore wind buildout complexities remain

- Southeast Asia emerges as brightspot

Iran’s chokehold of the Strait of Hormuz has revealed that Asia is particularly reliant on fossil fuels from the Middle East. Many are hoping the crisis will breathe new life into offshore wind projects across the region.

Asia offers an unexpected glimmer of hope for the offshore wind industry.

Energy security has trumped national agendas across the fuel-starved region, which gets over 60% of its oil imports from the Gulf, according to the International Energy Agency.

Offshore wind, with insatiable capital demands and execution risks, has seen spiralling unpopularity in contemporary US policy. But in Asia, which faces soaring gas prices and few other options, it stands a chance.

“Since the Middle East conflict began, Asia policymakers have increased discussions to accelerate the renewables agenda. This is especially apparent in North Asian countries, where offshore wind is the biggest lever,” said Romain Voisin, Head of Energy & Infrastructure Group Asia at Crédit Agricole CIB.

Korea, Japan, and Taiwan do not have substantial oil and gas reserves but they have extensive coastlines, accelerating the case for offshore wind, said Justin Feng, Asia Economist at HSBC.

Japan imports roughly 95% of its oil from the Gulf, making it Asia’s second-most dependent Gulf importer after Bangladesh, according to an HSBC research report. Korea and Taiwan each import over 70% of their oil from the Gulf.

Oil accounts for the largest share (nearly 40% on average) of the energy mix in Japan, Korea, and Taiwan, the report shows. That is followed by imported coal, natural gas, and nuclear. Renewable energy accounts for the slimmest portion, at 4.6% on average.

“Today, the market is demonstrating clear demand for diversified energy supplies to help reduce exposure to global fuel price volatility,” said Steve Mercieca, Managing Director and ASEAN Head of the Infrastructure and Development Finance Group at Standard Chartered.

Offshore wind is one component of this broader energy mix, particularly in markets where land availability constrains onshore development, he said.

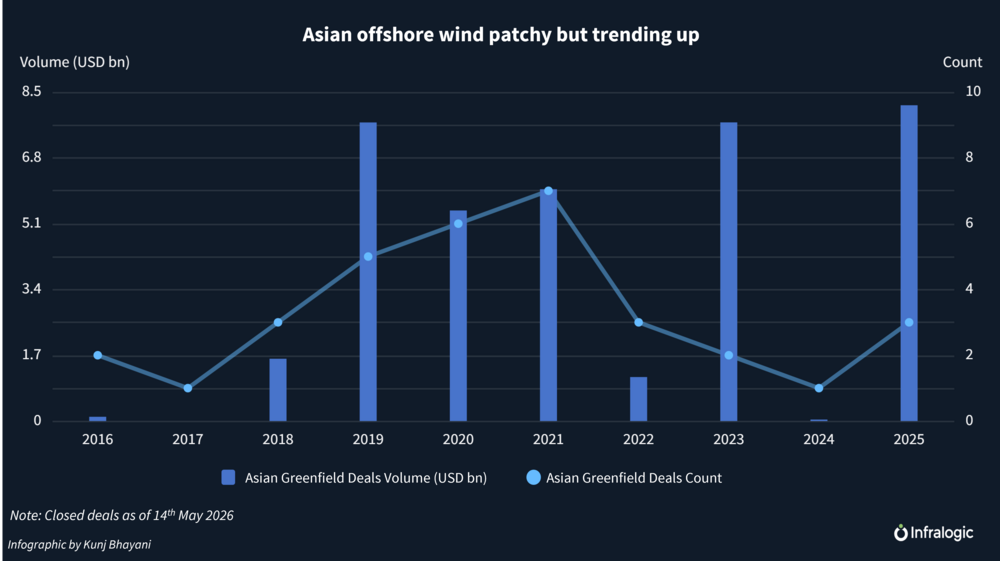

Excluding China, Asia’s offshore wind sector remains nascent, with activity mostly concentrated in the north. According to the Global Wind Energy Council, China alone has 48.4 GW of installed offshore wind capacity. Taiwan is the second-largest Asian market with roughly 3.6 GW.

Although China will likely continue its dominance, Asia is entering a turning point.

Auctions abound

Simon Engfred, Regional Lead Analyst APAC at Aegir Insights said “2026 presents a crunch moment: the success of several Asian offshore wind auctions will determine whether 2030 capacity goals can be met.”

Taiwan kicked off its latest tender offering 3.6 GW in March. According to a government ministry spokesperson, more than five developers have held discussions with the relevant authority.

“Taiwan has an established track record of project completions and round 3.3 terms look investor-friendly,” said Ryan Chua, Senior Managing Director at Stonepeak. The island, with a 12 GW pipeline, benefits from sustained policy visibility across administrations and early stakeholder engagement, he said.

Nadia Kalic, Sydney-based partner and Global Co-Head, Energy and Resources sector at Clifford Chance, agreed. “Taiwan’s early renewables build-out was anchored by a robust feed-in-tariff (FiT) scheme which provided long-tenor price certainty and consistency for investors, and as the market has developed FiTs have been complemented by corporate PPAs as an additional route to market and revenue stream,” she said.

Taiwan has also recently established the National Financing Guarantee Center, which guarantees an 80% project financing coverage ratio and encourages domestic firms to support offshore wind, the ministry spokesperson said.

South Korea is reviewing competitive bids for a 1H26 auction, with 1.8 GW of fixed and floating projects on offer.

The country’s development has been patchy, however. It brought Copenhagen Infrastructure Partners’ (CIP) 96 MW Jeonnam 1 farm, its first privately owned project, to commercial operations in May 2025. The project queue includes Equis’ Anma, which looks uncertain after CIP wavered on an equity cheque after the economy took a turn for the worst.

On the bright side, recent policy initiatives have been positive. The 2025 Special Act consolidated 28 separate approvals into a single ministerial process, marking “a real change to the risk profile, showing true intent to make it work,” said Stonepeak’s Chua.

“What’s needed now is a long-term tender roadmap with bankable offtake – expected this year,” said Chua. “It will matter a lot for whether political momentum converts into capital deployment,” he said.

Security issues around military permits remain, although they should be resolvable on a project-by-project basis, said Leow Kwang Heng, Head of Renewables, Project Finance Asia, MUFG. The government still needs to encourage domestic lenders to provide more local currency support, he said.

Japan, with an even more chequered history, is also set for a momentous year.

A 1.7 GW retender of the round one projects, slated for this year, is being closely watched by large Japanese corporates and international partners, said Peter Thompson, Director and East Asia Energy Business Leader at Arup.

Mitsubishi won all three projects awarded in Japan’s first round in 2021, before abandoning them last year, citing ballooning costs. “The cancellation was testament to the initial system being skewed; everything came down to price, on which Mitsubishi was extremely aggressive,” said Aegir’s Engfred.

“The government is expected to design the round one retender framework with a view to enabling project delivery, potentially including adjustments to the Feed-in Premium (FIP) structure and auction parameters,” according to Asako Haga, Tokyo-based Director, Structured Finance, Renewable Energy Project Finance at MUFG.

In addition, the government is considering changes to the framework for round two and three projects to reflect “materially changed market conditions” since the auctions, she said. Measures that address inflation and foreign exchange movements will be welcomed by developers, she added. Round two projects were awarded across 2023 and 2024; round three in December 2024.

Crédit Agricole CIB’s Voisin agreed. “Until now, a lack of inflation indexes in North Asia’s electricity tariffs have been a significant challenge for lenders and investors,” he said.

Japan’s round two and three projects, previously under FIP, will also be allowed to use the Long-Term Decarbonised Power Supply Auction, a 20-year capacity payments scheme, as part of the government’s rescue plan.

The clock is ticking. The market awaits further clarity on the round one rebidding rules and the expected retender timing, Haga said.

Supply disruption, force majeure protections

Asian offshore wind still has a long road ahead and the inflationary impact of the closure of the Strait of Hormuz is only adding to the sector’s woes.

Yet-to-mature auction designs and permitting processes, as well as grid bottlenecks are just some of the headaches. Adding another layer of uncertainty is the current issue of global shipping.

“Contractors are seeking to renegotiate prices to reflect increased volatility in shipping costs stemming from the Middle East conflict,” said Ee Lynn Tan, a Singapore-based partner at HSF Kramer. “Projects exposed to supply chain disruption may, as a result, face escalating costs.”

“We have been inundated with force majeure-related enquiries as parties move to ensure their rights and protections are contractually covered,” said Rob Palmer, Partner, Litigation, Arbitration, and Employment at Hogan Lovells.

Matt Bubb, another Hogan Lovells partner and APAC Head of Infrastructure, Energy, Resources & Projects, said “longer-term, it would not be unrealistic to expect project time extensions or under financing documents owing to conflict-induced supply chain effects.”

Standard Chartered’s Mercieca agreed, cautioning lenders to focus on ensuring robust procurement contracts in the short to medium term.

Reality check

Building offshore wind, which takes on average about eight years from pre-development to commercial operations in Asia (ex-China), will not solve the immediate energy shock, said Aegir’s Engfred.

In the meantime, Asia will keep its lights on with other sources.

“Putting aside political challenges, restarting existing nuclear plants is the low-hanging solution in North Asia,” said Adrian Wong, a Singapore-based partner at HSF Kramer.

Nuclear accounts for 15.7%, 5.6%, and 3% of Korea, Japan, and Taiwan’s energy mix, respectively, the HSBC report shows. That compares to 3.1% in China and 1.5% in India, the only other Asian countries with nuclear.

Offshore wind might be politically easier to justify than new nuclear, but in terms of pure cost and efficiency, nuclear is arguably preferable to offshore wind, HSBC’s Feng said.

“Despite the global push towards cleaner energy sources, fossil fuels including gas and coal will likely remain part of the global energy mix for much longer and continue to be strategically important for major export markets including Indonesia and Australia,” said Melissa Ng, a Singapore-based partner at Clifford Chance.

Coal is the second most-popular resource in Japan, Korea, and Taiwan’s energy mix, per the HSBC report.

Broadening natural gas supply is likely the most sensible and scalable solution, multiple observers agreed. That said, Asian spot liquefied natural gas prices have surged over 80% since the Iran war.

Rising gas prices narrows the cost differential against offshore wind – a silver lining for the growth prospects of the renewable energy sources, Arup’s Thompson said.

“Whatever happens, diversifying energy sources is key: be it gas or increasing battery storage for renewables,” said HSF Kramer’s Wong. Offshore wind is not the immediate solution but could present a longer-term option, he conceded.

Look south for saving grace

The good news is Asia is betting beyond its wind-abundant countries in the north. Southeast Asia is emerging with its own development path.

The Philippines has launched its first green energy auction exclusively dedicated to offshore wind. With 3.3 GW of fixed-bottom capacity on offer, it aims to award almost the same amount as Taiwan’s round 3.3.

“The Philippines is a fantastic breeding ground with a fully liberalised market, predictable processes, and a lack of scalable and competitive energy alternatives,” said Robert Helms, partner at CIP.

Investor confidence is high and power demand is growing, despite there being relatively limited offshore wind potential in the single-digit gigawatts, said Helms. He expects the country’s inaugural auction to be potentially oversubscribed, depending on how qualification criteria are applied.

In addition, Vietnam has an almost unlimited opportunity for fixed-bottom offshore wind farms, said Helms. However, concrete progress toward an investable, bankable regime is yet to materialise before investors can feel comfortable, he added.

“Discussions in Vietnam, albeit early stage, and the public tender in Philippines demonstrate that the momentum for offshore wind is going strong and moving beyond North Asia,” said MUFG’s Leow.

With energy security paramount to national policy, accelerating the construction of wind farms offshore might not be Asia’s worst idea.

[Editor’s note: The article has been amended post-publication to include Robert Helms’ full name and title and to update Nadia Kalic’s title.]

A service of

Shape your future with Infralogic. Today

Explore unlimited content like this, available only in the platform.

Already a client? Sign in