Squeezing the middle: a gap in the infrastructure mid-market is tempting big and small

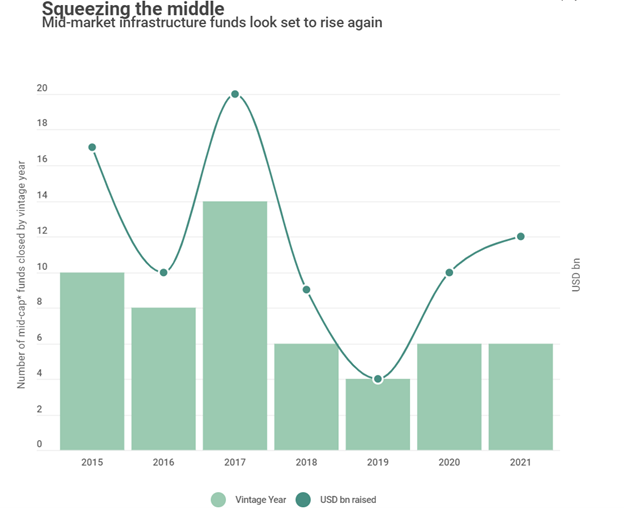

According to Infralogic data, the number of closed mid-market infrastructure funds (raising between USD 1bn and USD 3bn) over the past 7 years peaked with the 2017 vintage, when 14 mid-market infrastructure funds launched or hit their first close. It declined in the following two years.

The mid-market gap hasn’t gone unnoticed. GPs are now rushing to fill in the increasingly competitive space. Eleven mid-market funds have already hit final close in 2021 so far. While the more mature European market is already pretty crowded, North America still has some wiggle room.

“We've seen newer entrants in the last two or three years, but not one of the newer guys has really established themselves,” says a placement agent source.

Stay to play

New infrastructure managers typically play in the mid-market until they are ready to scale up. Some stay for the ability to enter new markets unnoticed.

“A buy-build strategy is much easier to do if your initial investment is in the hundreds of millions, not a couple of billions,” says a fund of funds source.

With USD 100-300m equity checks, a mid-market fund spends less to build assets that can be sold for much higher prices when the time is mature.

“It tends to be the more value-add managers who started off as a bit more mid-market focused being the first mover into certain niche sectors like healthcare,” says the fund of fund source.

More entrepreneurial risk also means higher returns, up to high teens or low 20s IRR, say sources – “That's nonexistent in the mega funds,” says an LP consultant.

Don’t wake the giants

Major infra funds such as GIP and Brookfield, EQT, Stonepeak, and KKR are not going to lose sleep over the mid-market space.

To the extent that they’re able to make investments in the USD 200m range, they still have a foot in the door and it’s not like LPs are shunning them in favor of smaller players.

But they’re not going to pass on the potentiality of higher returns either.

Antin Infrastructure Partners is the first of the major managers to raise a dedicated mid-cap fund, closing on EUR 2.2bn in June of this year. Antin IP’s CEO and managing partner Alain Rauscher described the mid-cap segment as “increasingly underserved and… a significant opportunity”.

Without calling it “mid-market”, smaller sector-specific funds have followed a similar trajectory too.

I Squared, for example, is currently in the market with an emerging markets infrastructure fund, targeting USD 2.5bn.

Others are likely to follow.

With a consolidation of capital into well-known names accelerated by the COVID-19 pandemic, a continued gap in the mid-market may be filled by those same big funds, instead of newer players.

A service of

Shape your future with Infralogic. Today

Explore unlimited content like this, available only in the platform.

Already a client? Sign in