Macquarie pays GBP 1.36bn for OTPP’s UK airports

Macquarie Asset Management (MAM) agreed to invest GBP 1.36bn to buy OTPP’s stakes in London City, Bristol and Birmingham airports, said sources familiar with the deal.

The deal includes a GBP 10m upfront payment to OTPP for its 25% stake in London City Airport, plus GBP 180m of equity to be injected into the airport operator over time to help restructure its debt, said the sources.

Most of the investment – about GBP 1.17bn – will pay for the Canadian pension fund’s 55% stake in Bristol Airport and 26.5% stake in Birmingham Airport, added the sources.

The sale of OTPP’s stakes in Bristol and Birmingham airports valued the two assets at a multiple of around 16 times their latest combined annual EBITDA of around GBP 200m, sources added.

MAM and OTPP announced the deal on 18 June, without revealing financial terms. Both declined to comment on the price.

The deal took place as OMERS and AIMCo also consider selling their combined 50% stake in London City Airport.

Frontrunner Blackstone-backed Mundys exited the process shortly before non-binding offers were due earlier in June.

MAM’s investment also comes as London City Airport works with Rothschild to restructure its debt pile to cut opco leverage from around 14 times its GBP 46m of EBITDA in 2024 to around 7x, according to other sources familiar with the talks.

OTPP and the other current shareholders, which also include Wren House, bought London City Airport from Global Infrastructure Partners in 2016 for a figure said to be around GBP 2bn, including debt.

MAM’s latest acquisition values London City Airport at a multiple of over 20 times its EBITDA, including debt after the restructuring, according to sources.

The airport in East London has struggled with its high leverage, as well as years of missing growth following COVID and a difficult shift from business to leisure travel.

Annual passenger numbers rose from 4.5 million in 2016 to 5.1 million in 2019, but have failed to recover from the pandemic, coming in at 3.5m in 2024. Its EBITDA has also remained flat over the past decade.

LCY debt restructuring

MAM, which was advised by Macquarie Capital and Deutsche Bank, is due to use half of its GBP 180m equity injection into London City Airport to help pay down its opco debt, sources said.

In total the airport is seeking some GBP 320m of equity from its shareholders to reduce its GBP 640m opco debt pile, which has maturities starting in 2026, sources said.

“The debt is no longer sustainable at those levels,” said one source, given the lack of growth.

Shareholders and lenders are looking to agree the restructuring in the coming weeks. This will adjust the company’s finances to the “current reality” of passenger numbers, compared to ambitious pre-pandemic expansion plans, added the source.

The rest of MAM’s new investment will repay OTPP’s share of around GBP 350m of holdco loans that were provided by Export Development Canada (EDC) in various tranches between 2016 and 2022, according to sources.

EDC’s public records show that in 2022 it upsized an earlier loan to London City Airport’s Jersey-registered holding company Londonia Bidco Limited to around CAD 200m-CAD 300m (GBP 106m-GBP 160m), and its loan to Londonia Midco Limited to CAD 500m-CAD 750m.

A spokesperson for EDC declined to comment on discussions over a possible refinancing, saying the institution “is obligated to protect commercially sensitive information”.

OTPP’s portfolio deal

OTPP, which was advised by Evercore, last month also agreed to sell its 39% stake in Brussels Airport to Flemish investment fund PMV, for an equity value of EUR 2.77bn.

It also sold its stake in Copenhagen Airport to the Danish state earlier this year, together with co-shareholder ATP, for around DKK 32bn (EUR 4.3bn).

The two deals were agreed after MAM made an initial approach late last year for OTPP’s entire European airport portfolio, including the Brussels and Copenhagen hubs.

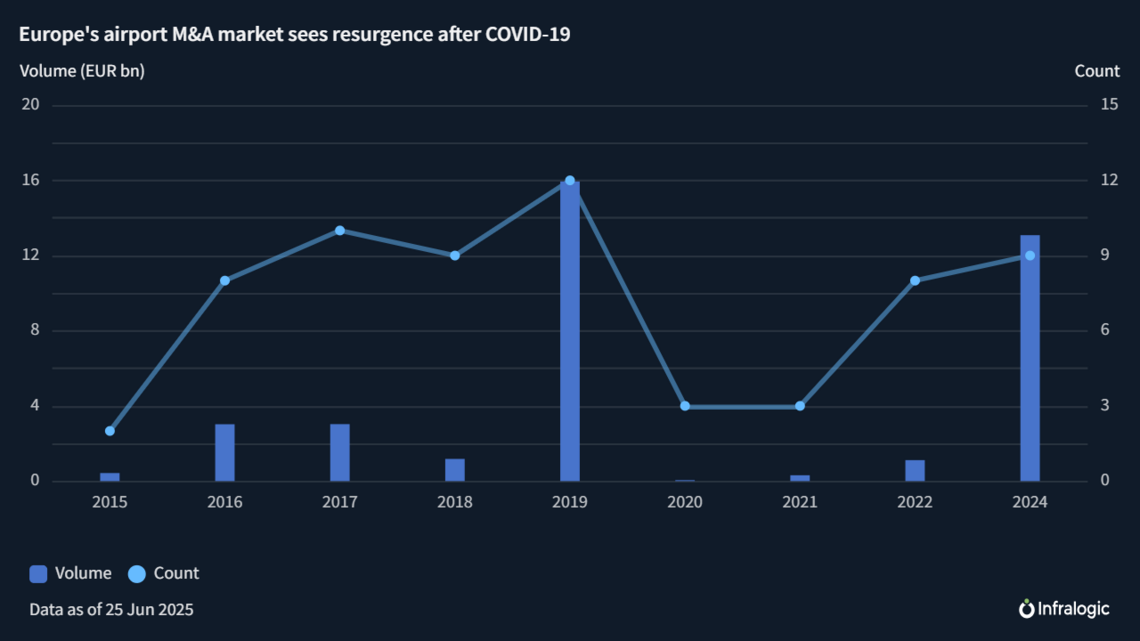

Airport M&A across Europe is picking up as passenger traffic across the continent finally exceeded pre-Covid levels in 2024, according to data by Airports Council International Europe, a trade body.

While larger airports and those focused on leisure travel and low-cost airlines are bouncing back faster, smaller airports and hubs that cater mostly to business customers are struggling.

“Beyond our positive headline results, nearly half of Europe’s airports remained below their pre-pandemic traffic levels last year,” said ACI Europe’s Director General Olivier Jankovec in February, presenting the 2024 traffic data. “We are now in a multi-speed European airport market where competitive pressures just keep rising.”

Capturing leisure traffic

London City Airport has historically focused on capturing business travel from the UK capital, but this has been slower to recover after Covid.

It has shifted to leisure betting that wealthy Londoners will be prepared to pay higher fees to fly from an airport easier to reach, compared to other airports such as Luton or Stansted that lie further afield. This, however, is yet to reflect in passenger numbers.

The operator is also trying to attract low-cost carriers for example by seeking approval to serve Airbus A320neo aircrafts, a favourite of airlines such as easyJet. London City Airport said in January it “sees the possible introduction of the A320neo as key to building its leisure offering”.

Last August it won government approval to add three extra flights in the first half hour of operations during the week, as well as lift an annual passenger cap from 6.5 million to 9 million.

Its request to operate flights on Saturday afternoons was rejected, however, and the airport still closes at 12:30pm on Saturdays.

Another possible avenue of growth is capturing more short-haul flights from airlines seeking to relocate from London Heathrow, as the UK’s largest airport nears capacity.

The UK has been Europe’s busiest market for airport M&A deals lately.

PSP-backed AviAlliance bought AGS Airports, which operates Aberdeen, Glasgow, and Southampton airports, from Macquarie and Ferrovial for a roughly 23x multiple last year.

Global Infrastructure Partners (GIP) sold a 50% stake in Edinburgh Airport to Vinci earlier that year for around 20x, while Ardian and Saudi Arabia’s Public Investment Fund (PIF) acquired a stake in London Heathrow.

Deals for smaller airports are also ongoing, including InfraBridge’s sale of its stake in Newcastle Airport, and Rigby Group’s divestment of Bournemouth, Exeter and Norwich airports.

A service of

Shape your future with Infralogic. Today

Explore unlimited content like this, available only in the platform.

Already a client? Sign in