The US infra mid-market’s coming of age

Ardian Infrastructure has gone full circle. While just less than a decade ago its flagship funds raised a little under USD 1bn, its latest sixth vintage hit EUR 11.5bn (USD 12.79bn). But it hasn’t forgotten its mid-market roots, closing in 2022 its Ardian Americas Infrastructure Fund V at USD 2.1bn. The manager is also preparing to launch later this year a mid-market infrastructure strategy with a USD 5bn target focused on the US and Europe.

The move signals a broader shift among infrastructure asset managers towards the mid-market, both in Europe and in its less mature US counterpart.

Ardian is not alone. In 2021, fellow France-based manager Antin Infrastructure Partners launched its inaugural mid-market fund, Antin Infrastructure Partners Mid Cap I, also targeting deals in Europe and North America. The large-cap manager is now preparing to launch its second midcap fund in the second half of this year.

Eight years ago, much of the US infrastructure middle-market began shrinking. Managers that had once raised USD 1bn–USD 2bn vehicles steadily moved up‑market, growing into multi‑strategy platforms with funds many times that size. Ardian and Antin’s return to the mid-market shows that, despite that migration, large managers still see untapped value in the sector. The US mid-market has also blossomed since the likes of I Squared, Stonepeak, and indeed Ardian grew out of it over half a decade ago.

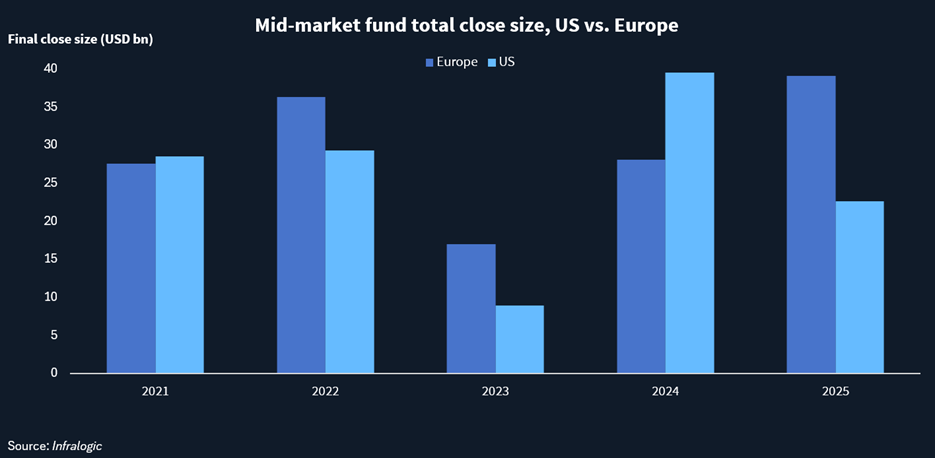

Fundraising activity in the US and Europe points to broadly similar levels of mid-market infrastructure opportunity, based on Infralogic data for funds sized between USD 1bn and USD 8bn. Between 2021 and 2025, European mid-market funds closed on USD 148.1bn, compared with USD 128.8bn in the US. Europe also recorded its strongest close year of the period in 2025, with USD 39.1bn across 15 funds, while US closes fell to USD 22.6bn across 13 funds from USD 39.5bn in 2024.

Also, since 2021, aggregate target fundraising sizes by mid-market managers have been nearly identical across the two regions, at roughly USD 103.9bn in Europe and USD 104bn in the US, while 2025 total target size reached USD 21bn in Europe and USD 23.5bn in the US.

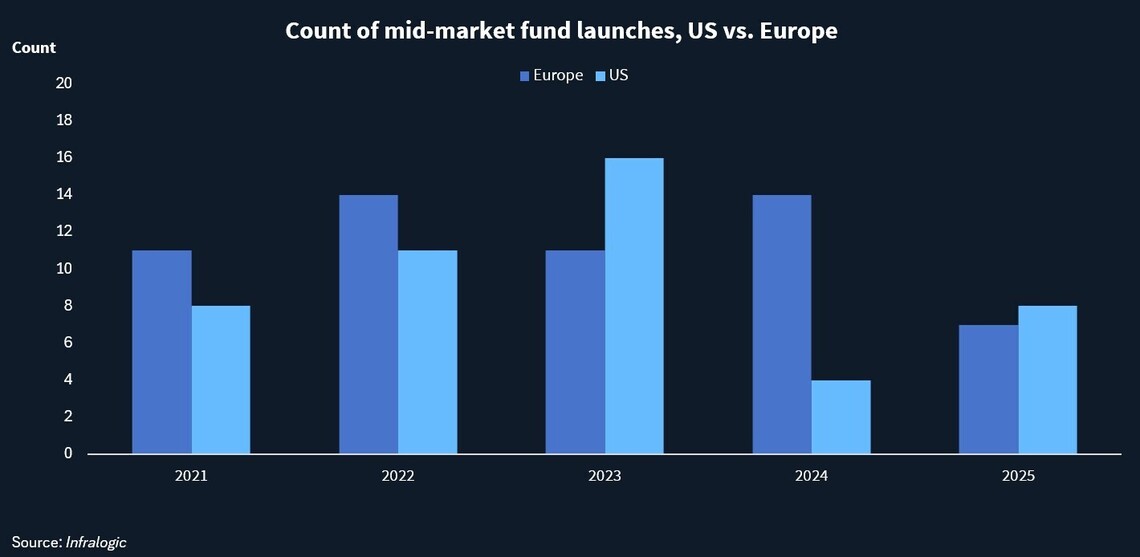

The data also suggests a broad manager base on both sides of the Atlantic, with 41 mid-market managers launching funds in Europe over the past five years, compared with 36 in the US. Last year, 11 mid‑market infrastructure funds launched in Europe compared with eight in the US.

The largest managers by target size were iCON in Europe, with USD 7.3bn across funds VI and VII, and EnCap in the US, with USD 9.3bn across three separate strategies.

Together, the launch and close data indicate that the US mid-market is comparable with Europe’s in breadth and scale, although Europe has converted more capital into closed funds over the past five years. In short, the attraction of the mid-market is broadly similar across both regions.

The US mid-market today

As the segment has changed, so too has the definition of “mid-market.” David Scaysbrook, co‑founder and managing partner at Quinbrook Infrastructure Partners, said now many LPs view funds in the USD 3bn–USD 5bn range as mid‑market, with USD 1bn–USD 2bn increasingly described as lower mid‑market. Some extend the definition even further to USD 7bn or USD 10bn.

“When I talked to LPs three or four years ago, the middle-market size was anything below USD 3bn,” said Guillermo Marroquin, head of North American Real Assets at Campbell Lutyens. When divided among a dozen or so deals, the mid-market investment falls around USD 250m.

“Today, when talking to LPs and GPs alike, the middle market is more about strategy,” Marroquin added.

Instead of relying on the numbers, LPs increasingly favor what mid‑market strategies can deliver: diversification, earlier‑stage exposure, and exit optionality, said Marroquin.

“There are a lot of LPs who have significantly greater interest in mapping the mid-market space than they have in the past,” said Jim Metcalfe, CEO and managing partner at mid‑market fund Astatine Investment Partners.

Fund managers have found certain sectors have blended well with the mid-market value-add strategy, including digital, environmental services, and transportation, shared Chris Beall, founder and managing partner at NOVA Infrastructure.

“The headlines are going to large, AI and hyperscale USD 30bn campuses with Meta or Google,” said NOVA co-founder Allison Kingsley. But “just because there are large scale data centers infrastructure investments, it doesn’t mean there aren’t small, middle market ones that might actually be more attractive and less risky.”

Kingsley gave the example of co-location, which allows for customer diversification compared to the mega-campuses with hyperscalers.

Another partner at a mid-market infrastructure fund shared that investing in energy and ancillary infrastructure around data centers is drawing interest from LPs that have otherwise said that they are over exposed to mega data centers.

Beall shared that the AI boom is also causing a renewed interest in power generation, both behind and in front-of-the-meter. While something the manager has invested in for a while, Beall said it is a way to play in the digital space while limiting exposure to AI and data center technology risk.

Mid-market drivers

“We’re getting to an inflection point. Now LPs are saying ‘okay we’ve invested in the big guys, and we need diversification, more types of strategies,” said Marroquin.

Mega‑cap funds, Marroquin added, tend to focus on large, mature assets and concentrated platform exposure, prompting LPs to reposition the mid‑market as a portfolio balancing tool.

The advantages of investing in mid-market assets have been highlighted by some difficult exit processes for larger assets. The attempted sale of Cubico Sustainable Investments has struggled to move forward since KKR dropped out of the process in summer 2025, and its owners OTPP and PSP are now considering selling the company for parts. Macquarie’s renewable platforms Corio and Cero have had unsuccessful sale processes with no clear exit timeline.

LPs are increasingly aware that mega‑funds are not selling many assets, he added, pushing investors to identify managers that can remain disciplined and return cash. “Midmarket is the place where you can get good exits,” said John Hanna, managing partner at Basalt Infrastructure Partners.

Data supports the perception. A May 2025 study by HarbourVest found that middle-market infrastructure funds distributed, on average, twice as much paid-in capital as large-cap peers of similar maturity across vintages from 2013 to 2022.

“LPs are saying: what we want from the middle market are the strategies where people are building, creating, institutionalizing and scaling businesses and assets,” Marroquin said. “Then on the back end, you have exit optionality – either selling to a strategic buyer or to a larger GP.”

The dynamic is playing out in live transactions. In February 2026, CVC DIF, Northleaf, and Landmark Dividend sold their stakes in US data center platform, Vault Digital Infrastructure, to Igneo Infrastructure Partners after seven years of growing the company. The transaction illustrates how mid‑market managers can scale platforms and exit to another institutional buyer.

Similar dynamics are evident in mid‑market energy infrastructure. In 2024, Astatine Investment Partners exited its stake in HEP Catalyst InvestCo, a Permian Basin midstream platform Astatine grew from a single asset into a multi‑project company before selling to joint‑venture partner Howard Energy Partners.

Other managers say the mid‑market also remains attractive for greenfield and development-led strategies, particularly in the US.

“There are more deals and opportunities in the lower middle-market relative to the amount of capital chasing deals of that size,” said John Ma, a managing director at Igneo Infrastructure Partners, which entered the US market in 2018. The segment is more of a buyers’ market than larger-cap infrastructure, where competition is more intense, Ma added.

He defined lower mid market as deals with equity of up to USD 250m, adding deals in this segment “tend to be smaller, more private, more bilateral, a lot of founder-owned businesses”. Returns, he added, need to be higher given the greater risk when “buying smaller, less mature businesses”.

Large infrastructure managers have not stood on the sidelines as LPs shift interest to middle-market strategies. Mega‑cap managers, like Ardian and Antin, have launched or continued mid-market or opportunity-style vehicles to access smaller, earlier stage investments.

“My view is that it just lends credibility to the space,” said Marroquin. “I don’t know that it necessarily crowds out other middle-market players.”

However, others draw a distinction between mid-market specialists and large platforms offering multiple strategies. Some managers cautioned that running mid‑market funds within global multi‑vehicle platforms can create incentive misalignment between teams and investors.

“Most of the carry is the big, flagship mega fund, and not the middle market funds. You have a misalignment between the core investment team and the investors,” said Allison Kingsley, founder and partner at NOVA.

That dynamic has contributed to a rise in spinouts from larger platforms in recent years, with senior investors leaving large platforms to launch mid-market focused firms. The AMP Capital infrastructure equity team’s transition into InfraBridge under DigitalBridge in 2023 is one example, with the strategy explicitly targeting mid-market opportunities rather than flagship-scale deals.

But whether those new entrants remain committed to the segment is an open question, she added. “The real question is whether they’re truly committed to the middle market, or whether they view it as a way station toward raising a USD 6bn or USD 15bn fund,” said Beall.

Challenges in the mid-market

But while LP interest in middle‑market strategies has increased, managers and advisors agree that the market has become more selective rather than expansive.

Despite renewed LP interest, the mid-market still faces challenges when it comes to investment teams’ records, slowdowns in fundraising, and PE and real estate mid-market competition.

“It’s been very difficult for generic fund managers,” said Scaysbrook. “LPs have been very selective, only bothering to back diligence managers with really strong track records.” He added that there is now “a selection bias toward midmarket specialists delivering value-add returns.”

Fundraising data reflects that selectivity. Infralogic data shows US mid‑market fund closings peaked in 2021 and 2022, before slowing sharply in 2023 and 2024. While 2021 saw 17 final closes, 2024 saw just four.

Hamilton Lane data also shows fundraising timelines have lengthened. As of May 2025, funds took an average of 31 months from launch to final close, double 2021 levels.

“It would be hard to come up with 10 middle-market US GPs that are on fund three or beyond,” said Marroquin, citing the maturity level of the market versus Europe.

A global LP noted that Europe has a deeper and more established pool of mid‑market infrastructure managers, offering a broader range of options and a “longer heritage of infrastructure-dedicated managers.”

By contrast, the US market remains more fragmented, with fewer dedicated mid‑market infrastructure GPs and a greater presence of sector‑focused or private equity‑style managers. While investors see opportunities in both regions, the LP said the “menu” of mid‑market managers is still more developed in Europe.

“The US is tough to cover,” said Basalt’s Hanna. “It’s a large, fragmented market. Track record and credibility are essential, and building a niche takes time.”

Competition also comes from spin‑outs, international managers, and firms pivoting from real estate or private equity.

“We also see real estate coming in and realizing that owning property and operating a project is very different… PE will come from asset light investing and realize it’s not the same to manage capital in an asset heavy business,” said Kingsley.

Looking into the second half of 2026, managers and advisors expect modest improvements in exits rather than a broad fundraising rebound.

Scaysbrook expects to see “a bit of improvement in the exit and liquidity scenario” as M&A activity picks up, while cautioning that LP behavior is unlikely to shift dramatically.

Metcalfe shares that optimism, with caveats around geopolitical risk.

“In the absence of this exogenous event, which we don’t have any control over, I think we’re extremely optimistic about a fundraising environment for this year,” he said.

With fewer mega‑funds in market, Marroquin added that the mix of capital in 2026 could tilt incrementally toward mid‑market strategies.

What remains clear is that LPs are no longer chasing size alone – and that the mid‑market’s appeal increasingly lies in execution, exits and discipline rather than scale.

A service of

Shape your future with Infralogic. Today

Explore unlimited content like this, available only in the platform.

Already a client? Sign in