Brazil prepares for government transition with projects pending

The first term of Brazilian President Jair Bolsonaro is coming to an end with a list of proposed infrastructure projects still under development. The federal government has been trying to tender as many projects as possible by the end of 2022, but some of the concession and privatization projects that the government has proposed during Bolsonaro’s time in office will remain ‘pending’ and could yet form part of the agenda of the winner of October’s national elections.

In June 2021, the then Infrastructure Minister Tarcísio Gomes de Freitas expected to tender a portfolio of projects with a BRL 261bn (USD 51bn) combined capex by the end of 2022, but his plans were not fully realized.

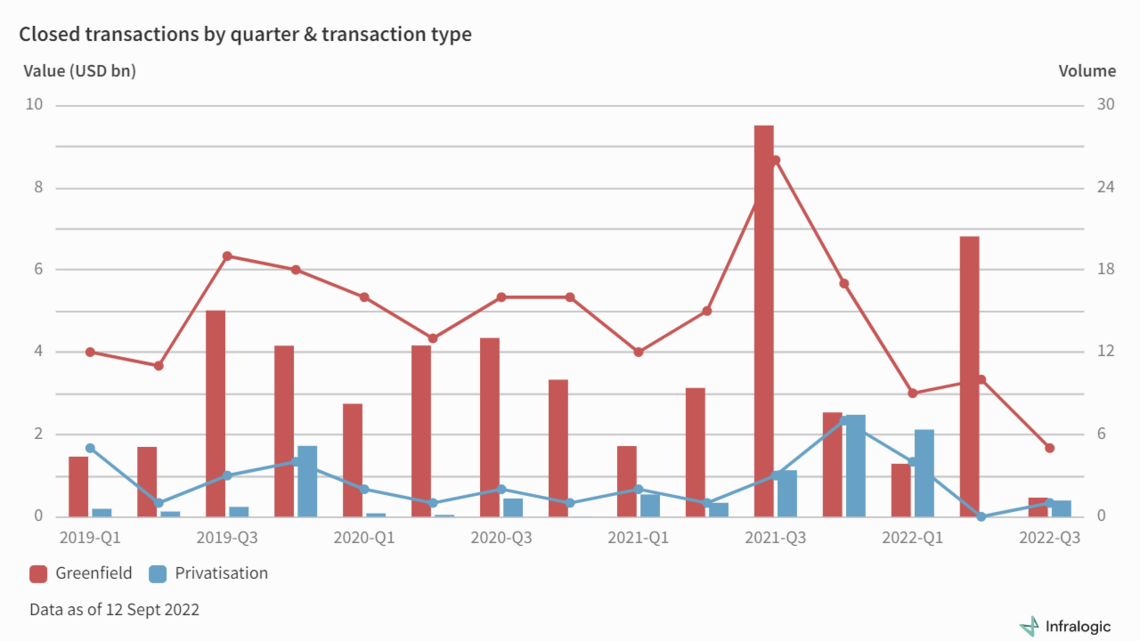

However, to date, Brazilian federal authorities have successfully awarded only 11 infrastructure concessions and carried out the privatizations of power company Eletrobas and port administrator Companhia Docas do Espírito Santo (CODESA) as of September 2022, initiatives that required USD 9.8bn in total capex, according to Brazil’s Investment Partnership Program (PPI).

Freitas’ successor Marcelo Sampaio acknowledged delays in bidding schedules and attributed it to conjunctural issues, such as the COVID-19 pandemic, high interest rates and the unfolding war in Ukraine.

“We could not proceed as quickly as we had hoped, we had difficulties in proceeding with some public consultations and hearings, and we have adjusted the schedules,” he said in an 18 August press conference.

“We postponed the bidding for some highway assets after market players warned us about the accumulation of auctions in a single period and the risk of investors not being able to evaluate and absorb so many projects,” he added.

Sampaio considered the global macroeconomic scenario in 2022 challenging but argued that Brazilian projects still represent an opportunity for international investors.

“When we talk about attracting non-Brazilian investors, we are competing with other countries, such as Mexico, Colombia and India. Brazil is in an advantageous position in relation to these countries. We experienced record deflation in July, foreign capital is entering the country month after month, and Brazil has become a safe destination for non-Brazilian investors,” the minister said.

The PPI is a portfolio of 151 federal projects, comprising 91 in the infrastructure market, as well as providing aid to states and municipalities to structure a further 56 projects.

The Program still expects to auction 25 federal infrastructure projects in 4Q22, before the change in government, and help local governments to tender another 22 projects in the same period, according to an August presentation.

The biddings planned for 4Q22 should attract a total of USD 18.4bn in investments, according to information from the PPI.

The retender of the São Gonçalo do Amarante (Natal) airport, two lots of highway concessions in the state of Paraná, the BR-381/MG highway, 13 port terminals and the privatization of the administration of the São Sebastião port, in São Paulo, and the Itajaí port, in Santa Catarina, are some of the projects that the federal authorities are pushing to auction by the end of 2022.

The PPI’s projections also comprise electricity supply and transmission auctions to be carried out by Brazil’s power regulator agency ANEEL in September and December, respectively.

Despite federal efforts to push the government’s concessions and privatizations agenda, market players are questioning the real viability of the remaining auctions scheduled for 4Q22.

“It will be difficult to tender all those projects in such a short period of time. Government transitions always cause uncertainties in terms of continuity, and the international scenario is not favorable,” Venilton Tadini, president of the Brazilian Association of Infrastructure and Basic Industries (ABDIB) told Infralogic. “It's hard to say what will or won't come out of this list.”

Although the incumbent president is running for reelection, Bolsonaro is trailing in polls of voting intentions. Rival candidate, and former President Luis Inácio Lula da Silva (2003-2011) is leading in the latest polls with a comfortable advantage. Lula has 45% of voting intentions and President Bolsonaro has 34%, according to the Datafolha institute.

Lula has selected former São Paulo Gov. Geraldo Alckmin to run as his vice-presidential candidate.

Alckmin, a center-right politician with a market-friendly approach, presented pro-private investment ideas for the infrastructure sector during a recent ABDIB forum, but highlighted that privatizations will not be a priority in a Lula presidency.

Regardless of political uncertainties, Tadini observes that the investors are low on appetite for greenfield or yellowfield projects due to the rise in construction and financing costs.

The increase of Brazil’s Selicinterest index from 2% in January 2021 to 13.75% in June 2022 and a slow economic recovery from the COVID-19 pandemic have forced investors to take a more cautious strategy, Tadini says.

“With high interest rates, we are seeing companies and investment funds more interested in brownfield opportunities than greenfield because the present value and the risks are lower,” he explains. “They are preferring to fund investments with existing cash flows rather than taking greenfield risks and leveraging huge amounts to generate revenue.”

The ABDIB’s president categorized the resumption of Brazil’s economic growth as “slow.” The country registered a 1.2% GDP rise in 2Q22 compared to 1Q22, accumulating a 2.5% growth in 1H22.

Besides the war in Ukraine, the slowdown of the Chinese economy and the high single-digit inflation seen in the US has also contributed to the difficult investment atmosphere in Brazil.

“People still say there is extreme liquidity in the world, but this is not true anymore. Resources have already gone to stronger countries and the local players are still digesting their recent investments,” Tadini adds.

Brazilian inflation also poses challenges by raising construction costs, requiring the revision of concession models. Transportation and sanitation projects are more sensitive due to increased demand for construction works, Fundação Getúlio Vargas (FGV) researcher Luiz Guilherme Schymura said.

“The infrastructure sector suffers from rising prices in vital items such as diesel oil, steel and cement. Pronounced increases in decisive inputs in the cost structure can cause total economic-financial imbalances in contracts in a relatively short time,” he added.

The cost of construction has been among the issues that have caused the postponement, remodeling, and low competitiveness in bidding processes for highway projects at both a federal and state level.

Brazil’s latest transportation auctions had a low number of participants. Spain’s Aena was the sole bidder for the main asset of the seventh round of airport concessions while Ecorodovias was the sole bidder for the Rio-Valadares highway concession.

Despite low competitiveness, Minister Sampaio considered the auctions a success and minimized criticism regarding the lack of completion of highly anticipated projects during Bolsonaro's first term, saying that the Ministry of Infrastructure is working to build an agenda for the nation, independent of political and electoral cycles.

However, projects that were promised and announced by members of the current government, such as the Ferrogrão railway, the retender of the Viracopos Airport and the privatization of the Port of Santos will inevitably be inherited by the next administration.

The issues around the postponement of those projects are not only economic. The tender of the 933km (579-mile) Ferrogrão railway concession, considered crucial for the outflow of agricultural commodities, was suspended by Brazil's Supreme Court due to environmental issues.

The PPI foresees launching tenders for 82 infrastructure projects from 2023, totaling over USD 30bn in investments.

The Santos Dumont and Rio-Galeão airport concessions, three lots of highways in the state of Paraná, the BR-364/MT/RO and BR-070 highways, and the privatization of the Port of Santos are among the projects that the PPI foresees tendering during the next presidential term, which starts on 1 January 2023.

Tadini does not consider the delays essentially negative for Bolsonaro’s presidential legacy but stresses the importance of good performance for the projects awarded during his tenure to secure the continuity and progress of concessions still in development.

“The projects are well structured, but the important thing is that they generate positive effects and avoid investors returning contracts,” he said.

José Virgílio Enei, partner and co-head of infrastructure at Machado Meyer Advogados, agrees that leaving pending projects is not detrimental to Bolsonaro’s legacy and foresees a continuity of Brazil’s concessions agenda regardless of who wins the elections.

“We saw significant progress for infrastructure projects in the past three years. This administration was able to reasonably meet deadlines but now the tenders are getting almost impossible because of the presidential and state government elections,” he said.

However, Enei observes that 2H22 has been more active in terms of transactions than in previous election years, which used to have a busy first half and a decrease in tenders and financing transactions in the second half.

“The market has surprisingly not stopped and is active in financing and M&A transactions, especially in the renewable energy sector. Despite the increase in interest rates, this scenario was predictable and considered in the projects,” he said.

Initial public offerings (IPO) were the only operations that did not regain momentum after the COVID-19 pandemic, Enei added.

“We don't see a clear preference for a candidate among our clients and clients believe that there will not be a big setback in terms of infrastructure development. What is in the pipeline should be tendered,” he explains.

Although predicting a consistent business scenario for 2023, the Machado Meyer partner highlights the aversion to privatization on Lula’s platform.

Enei thinks that there may be some confusion in differentiating the concepts of privatization and concession, as some concessions were debated politically as if they were privatizations.

“The concession of the Congonhas Airport was treated as a privatization. Would Lula have carried out the seventh round of airports concessions as we had? We don’t know,” he said.

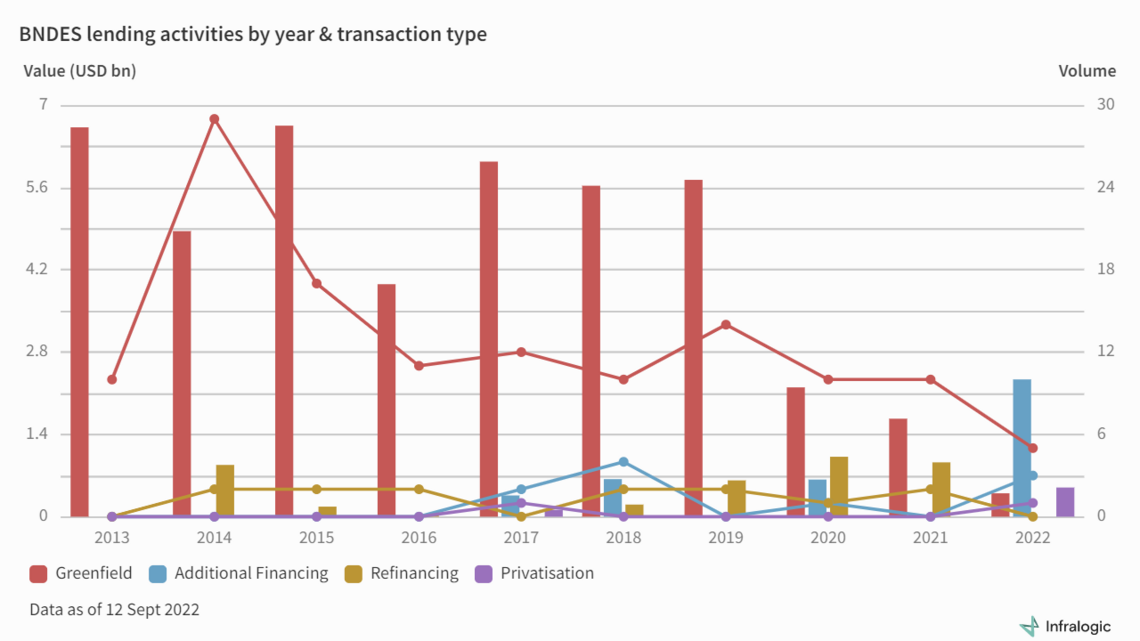

Brazil’s development bank BNDES’ role as a lender and project structurer is another open question for the next presidential term.

Tadini believes the reduction of BNDES’ role as a lender was too quick and ABDIB advocates for an increase in its activity to provide guarantees and to foment a wider pool of project lenders.

Enei thinks that in the case of a Lula return to the Planalto Presidential Palace, BNDES could be called to increase the disbursement of public resources through project financing, although not in the same volume that it used to disburse.

The development bank disbursed BRL 440bn for infrastructure projects between 2011 and 2017, according to a 2018 report.

“BNDES no longer carries out subsidized financing and is applying market rates to its loans, but an increase of its lending activities affects competition in the capital markets and contributes to the country's fiscal deficit,” Enei observes.

Fernando Fleury, partner of the project finance advisory boutique Almeida & Fleury, considers that the Brazilian capital markets have assumed part of the required infrastructure financing through bond issuances, but the volume is not comparable to what BNDES used to finance.

“The infrastructure bond market is thriving with an average of BRL 30bn in issuances per year, but this is a third of what BNDES used to finance and we don’t know if the bond market will sustain that volume in the long-term,” Fleury said.

Incentivized bonds dedicated to infrastructure projects totaled BRL 20.7bn in 1H22, according to a Ministry of Economy report.

Fleury observes that some of the projects which were financed through bonds would not pass BNDES’s criteria.

“A badly structured project ends sharing the risk with bondholders, but what is the limit of acceptability for brokers to offer these bonds to their clients?” he asks. “This mechanism will have to undergo a review of private financing architecture.”

Fleury considers that Brazil is still passing through a transition period for infrastructure policies. He observes that corruption investigations and economic difficulties led the country to abandon a model in which the federal government had a broader participation in infrastructure investments up to 2014.

“We had a model exhausted and, historically, it takes an average of 10 years to redefine the public policy model for the sector. After eight years, we still don't know what the new model is,” he said. “Bolsonaro came in with a very minimalist Vision of the role of the state and without a clear public policy behind important projects.”

Fleury considers that the risk of having an unclear role of the state overlaps the macroeconomic risks in the long term.

“Institutional risks derived from an ill-defined public policy are not essentially priced in but are fundamentally linked to the willingness of deal breakers to enter projects,” he said.

A service of

Shape your future with Infralogic. Today

Explore unlimited content like this, available only in the platform.

Already a client? Sign in