Secular declines still taking the wind out of Windstream’s sails – 2Q23 Credit Report

OVERVIEW

Windstream Holdings II, LLC (WIND) faces an uphill battle as it attempts to reorient its business model away from secularly declining legacy services. In 2Q23 WIND’s total revenue declined 5.2% year-over-year (YoY) to USD 991m, its pro-forma adjusted EBITDA declined 1.7% YoY to USD 216m, and its liquidity declined 9.4% sequentially to USD 425m demonstrating that the company has yet to turn the tide against weak profitability and persistently down-trending revenue and EBITDA. Under our base case we project that the company will burn USD 122.8m of cash over the next twelve months (NTM) resulting in liquidity of USD 302m on 30 June 2024, and that it will deplete its liquidity in 2H26 as Growth Capital Improvement (GCI) and settlement payments from Uniti Group, Inc. (UNIT) roll off. However, the bifurcation of its Master Lease Agreements (MLAs) with UNIT to align the leases more closely with WIND’s Kinetic (ILEC) and Enterprise/Wholesale (CLEC) business units should help facilitate an asset sale to cover any liquidity shortfall.

WIND’s fiber-to-the-home (FTTH) initiative has yielded positive results and has improved the economics of its Kinetic/ILEC-focused segment (consumer revenue up 4.5% YoY to USD 321.5m and next gen fiber gigabit internet customers up 75% over 1Q22 to 340k), but it requires significant capital investment and thus far hasn’t been enough to offset sustained declines in other services. Stabilizing operations in its Enterprise segment (revenue down 19% YoY to USD 351m) is particularly critical, and it is unclear whether improving cost structure and lowering interconnection expenses while simultaneously converting customers to more profitable cloud-based networking solutions can mitigate secular declines. WIND’s future largely hedges on its ability to increase its share of the broadband internet market and overall trends in demand for broadband internet services.

WIND has clearly been laying the groundwork for a potential asset sale, and in February 2023 it was reported that WIND had retained advisors to shop a sale of its Wholesale business with an estimated valuation of between USD 1bn and USD 2bn. Using the Wholesale unit’s LTM contribution margin of USD 180m as a loose proxy for adjusted EBITDAR, we think it is feasible that a future sale could generate proceeds of somewhere around USD 800m to USD 1.5bn with a multiple in the 5x-8x range. However, it is unclear if there is an active sale process. WIND has weak asset coverage due to the 2015 spin-off of UNIT and associated sale/leaseback of a large portion of WIND’s telecommunications infrastructure assets, and the Wholesale business is one of the company’s relatively few monetizable assets.

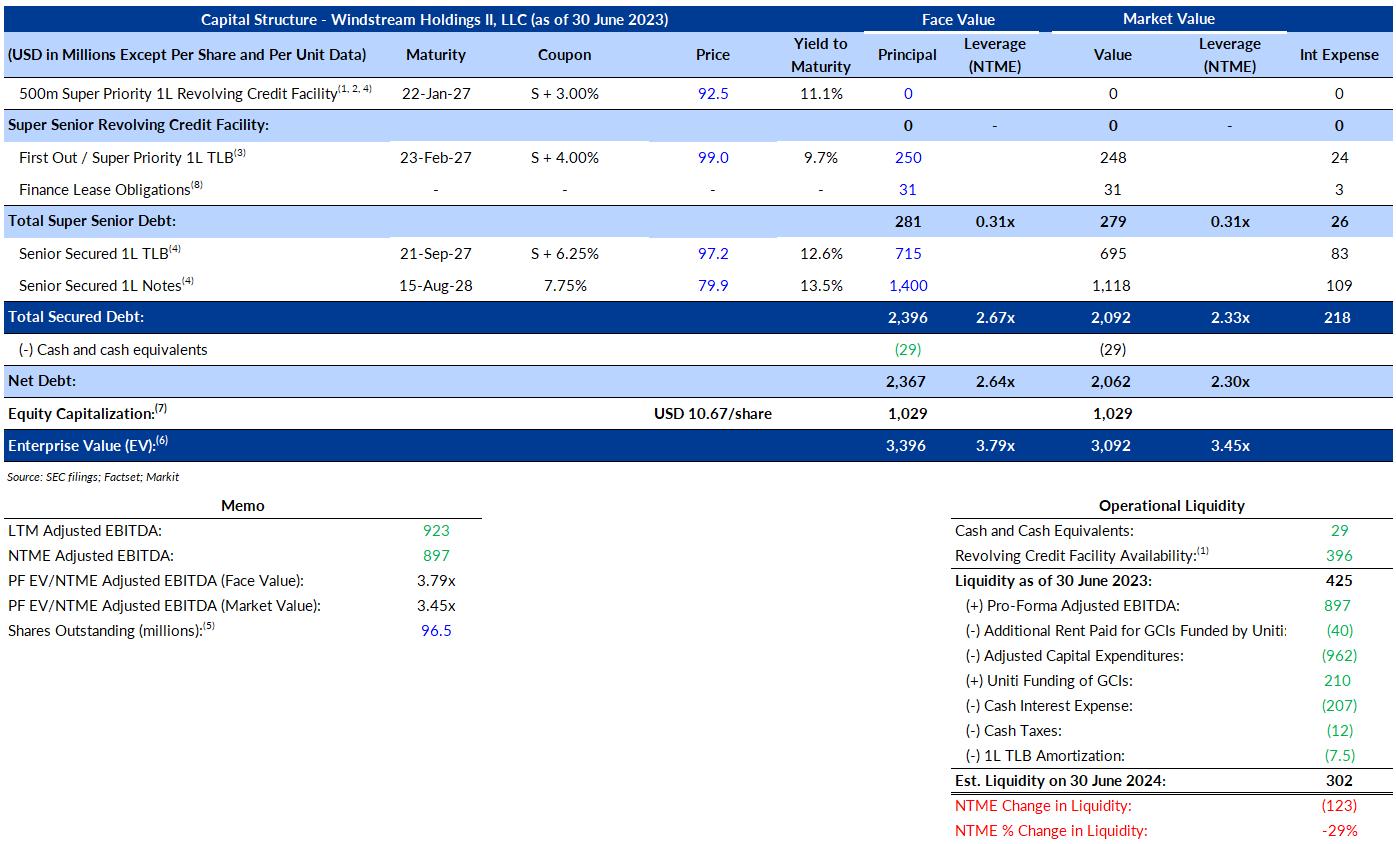

Chronic underinvestment and high leverage prior to the 2019 bankruptcy contributed to an erosion in WIND’s competitiveness, but the restructuring allowed it to reduce its debt by 63% to USD 2.15bn while associated GCI and settlement payments from UNIT have partially de-risked WIND’s FTTH upgrades allowing it to internally fund an overall increase in its capital intensity. WIND now has a period of several years to build on meaningful progress in some areas and prove its strategy can return it to profitability and positive free cash flow.

FINANCIAL PERFORMANCE

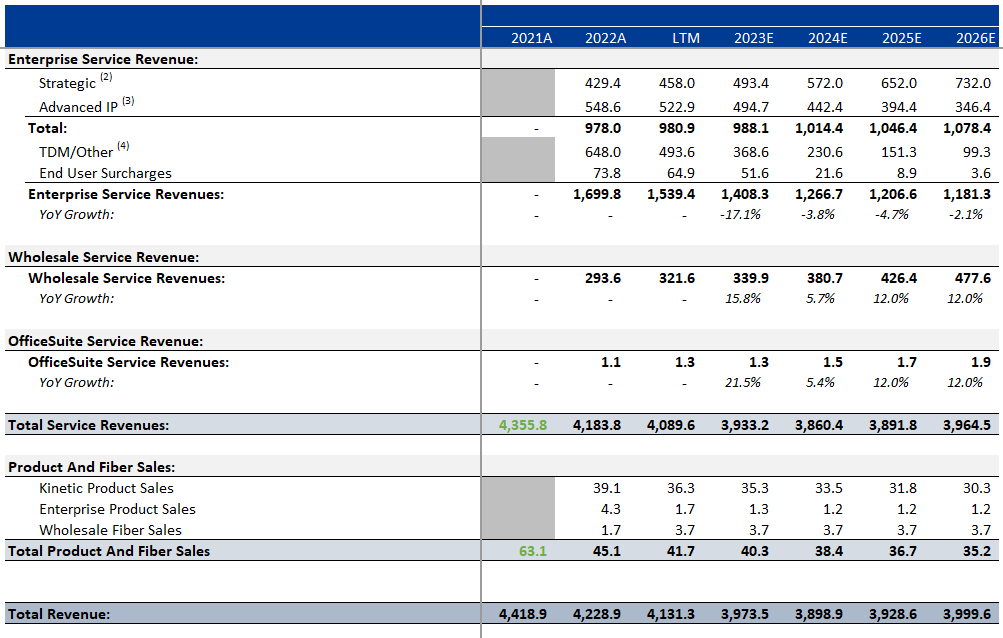

WIND’s investments under its FTTH strategy designed to overbuild its ILEC copper network with fiber were the foundation for a 3.7% increase YoY in Kinetic segment service revenues to USD 546.5m in the quarter. Likewise, the segment’s contribution margin increased by 6.8% YoY to USD 272.9m as a result of both revenue and margin expansion. We expect Kinetic revenues will increase by 1% over the NTM and continue modestly climbing to USD 580m by YE 2026. In 2Q23 WIND achieved net additions of 24.4k fiber gigabit internet customers, but total high-speed internet customers declined by 7.7k when offset by the net loss of 32.1k DSL customers. However, average revenue per high-speed customer increased by 6.7% YoY to USD 87.4 even while total high-speed internet customers declined by 1.9% YoY since fiber gigabit is a higher price and higher margin product. The strategy has thus far led to 24,000 fiber route miles constructed with 23.8% of the copper network overbuilt with fiber. Inflation in labor and materials costs and supply chain issues may adversely impact the company’s FTTH buildout.

WIND has been the recipient of various types of government assistance. Most notably this consists of Rural Digital Opportunity Fund (RDOF) support from the FCC for rural broadband deployments (for which the company was awarded USD 522.8m in RDOF support over 10 years, or USD 52.3m per year beginning in 2022), and State Universal Service Fund (USF) support which the company receives from eight state USF programs intended to subsidize the high cost of operating telecommunications networks in rural areas (for which the company received funding of USD 100.2m in 2022, USD 38.9m in 2021, and USD 75.1m in 2020 including funding to the predecessor entity).

WIND continued to see steep deterioration in operating results in its Enterprise segment, with 2Q23 revenues down 19.3% YoY to USD 351.4m and contribution margin down 36.3% YoY to USD 57.1m resulting from both margin compression and revenue declines. We expect Enterprise revenues will decline by an additional 9% over the NTM to USD 319m, and by 16% through YE 2026 to USD 294m. WIND has been able to meaningfully grow Strategic revenues (up by 14.3% YoY to USD 120.5m in 2Q23), but progress is still insufficient to offset large declines in revenues for legacy services. Strategic revenues constituted 36% of Enterprise segment revenues in the quarter, and we expect that proportion will increase to 65% by YE 2026.

Revenues in WIND’s Wholesale unit rose by 15% YoY to USD 84.3m (excluding intersegment revenues) while the segment’s contribution margin increased by 15.6% to USD 45.3m. We expect Wholesale revenues will increase by 12% over the NTM to USD 94m and rise further to USD 119m by YE 2026. As stated, strength in this segment is likely to play a critical role in the company’s efforts to both offset declines in its Enterprise segment and to generate liquidity through an asset sale.

On a consolidated basis we expect that total revenues will decline by 1.8% over the NTM to USD 973m but will rise modestly by 1% through YE 2026 to USD 1.0bn. Nevertheless, we expect WIND’s changing revenue mix and measures to cut costs and improve operating efficiencies will positively impact margins and lead to a 3.7% increase in pro-forma adj. EBITDA margin over the NTM, and that pro-forma adj. EBITDA will rise to USD 236m in 3Q25 (versus USD 216m in 2Q23) before falling to USD 225m by YE 2026 after settlement payments from UNIT end.

The MLAs with UNIT are structured as triple net leases and subject WIND to onerous cash burdens including rent of USD 714.4m over the NTM under our estimates (including USD 40.5m of additional rent related to previous GCIs). Additionally, any capital improvements funded by WIND and not subject to reimbursement (termed Tenant Capital Improvements; cumulative of USD 1.2bn of TCIs since 2015) become property of UNIT upon completion. We believe the April 2030 renewal of the MLAs will likely lead to a reduction in cash rent paid to UNIT which should help partially alleviate cash burn.

If the two parties are unable to reasonably agree on what constitutes fair market value of the MLAs following the 2030 expiration of the leases, then it will be determined by an independent appraisal process. Windstream has released documents into the public domain outlining its view that renewal rent could be reduced by upwards of 70% to around USD 200m, while UNIT has stated its view that Windstream’s calculations were incorrect and that cash rent following the renewal will be at least USD 600m and could be as high as USD 800m. The wide chasm between UNIT’s and Windstream’s relative MLA valuations make it virtually inevitable that the independent appraisal process will be required.

WIND has USD 965m of debt maturities in 2027 (including its USD 475m revolving credit facility) and USD 1.4bn in 2028, while 97% of UNIT’s debt matures between 2027 and 2030. Both parties will thus be pressured to negotiate a compromise in order to refinance or otherwise address their respective significant maturities.

VALUATION

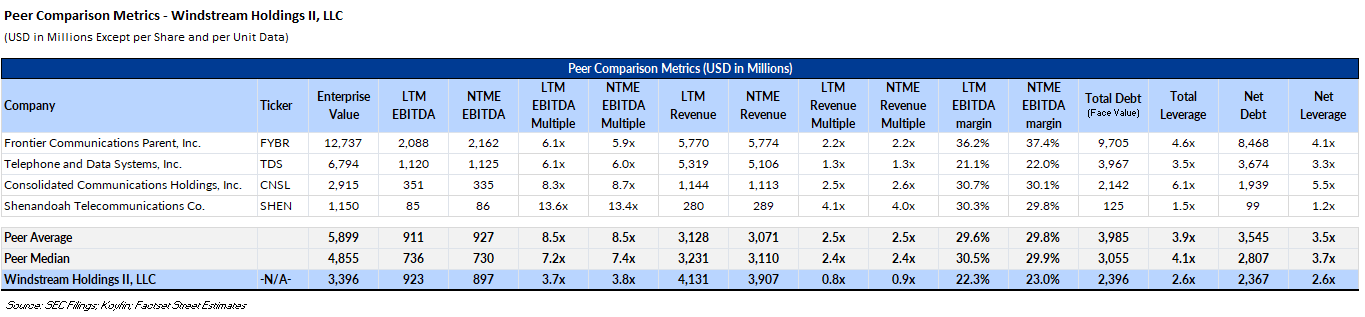

WIND is currently trading at an LTM EV/PF adj. EBITDA multiple of 3.7x which is lower than the peer median of 7.2x reflecting WIND’s relatively low EBITDA margin, its persistently declining revenue and EBITDA, and its weak asset coverage and onerous lease obligations resulting from the sale/leaseback transaction with UNIT

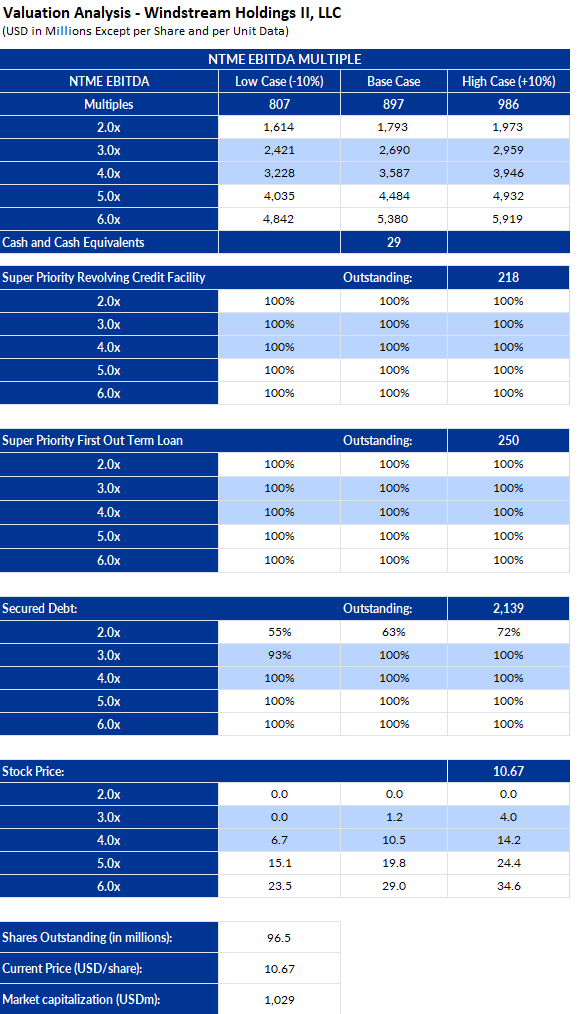

For our base case valuation, we use a NTME PF adj. EBITDA of USD 897m and an EV/PF adj. EBITDA multiple of 3x-4x. This multiple is in line with the company’s current valuation. Under this scenario the super senior revolving credit facility, the super priority first out term loan, the 1L TLB, and the 1L notes all receive a full recovery, and the implied market value of equity is between USD 1.2 and USD 10.5. This equity valuation is in line with the current bid price of WIND’s equity of approximately USD 9.5 per share.

COMPANY DESCRIPTION

Windstream Holdings II, LLC (WIND) is a Little Rock, AK-based privately held communications and software company that provides high-speed broadband internet, phone service, and digital TV packages to residential customers in rural areas across 18 states, as well as network communications and technology solutions for businesses and government agencies. The company began as a rural telephone service provider from the 2006 spinoff of Alltel Corporation’s landline business and merger with VALOR Communications Group, Inc. WIND operates in four segments: Kinetic, Enterprise, Wholesale, and OfficeSuite. It owns 100% of Windstream Services, LLC.

WIND emerged as a private entity following a litigation-induced chapter 11 restructuring process on 21 September 2020. In 2015, Uniti Group, Inc. (UNIT) was created as a spin-off from Windstream Holdings, Inc. (predecessor entity). Pursuant to the spin-off, WIND contributed telecommunications assets including fiber and copper networks and other real estate to UNIT and entered into a triple-net lease agreement through which the contributed telecommunications and distribution systems were leased back to WIND. Aurelius Capital Management (infamous for their battle with the government of Argentina) took positions in WIND’s debt consisting of a long position via bond purchases and a short position via credit default swaps. In 2017, two years after the spin-off and sale leaseback transaction, Aurelius issued a notice of default alleging the 2015 transaction violated WIND’s indentures. In February 2019, WIND filed voluntary petitions for reorganization under Chapter 11 after the Southern District of New York ruled that the spin-off and transfer of assets to UNIT violated the sale-leaseback covenant in WIND’s indentures and constituted an event of default. In accordance with the settlement, UNIT is obligated to pay WIND USD 490.1m in cash in equal installments over 20 quarters and to reimburse WIND for an aggregate of USD 1.75bn of Growth Capital Improvements (GCIs), both beginning in October 2020. Elliot Investment Management LP became WIND’s largest shareholder upon emergence from the restructuring.

Following the restructuring the amended master lease agreements are now bifurcated into two structurally similar but independent agreements, one governing network facilities within ILEC markets and one facilities within CLEC market areas. This bifurcation more closely aligns with WIND’s Kinetic (ILEC) and Enterprise and Wholesale (CLEC) business units and may help facilitate the disposition of either of these businesses in the future.

On 22 November 2022 the company amended and extended its revolving credit facility pushing the maturity to 2027 from 2024, and simultaneously issued the USD 250m super senior incremental term loan, using part of the proceeds to pay down USD 115m of outstanding revolver borrowings.

Nicholas Parker

A service of

Start your trial. Today

Explore unlimited content like this, available only in the platform.

Already a client? Sign in