LevFin Highlights 1Q25

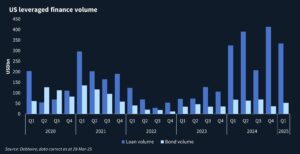

Leveraged finance (LevFin) issuance across the US and European institutional loan and high-yield (HY) bond markets reached USD 509bn in 1Q25 year-to-date (YTD), broadly in line with the first quarter of 2024 and 6% down on 4Q24. Market conditions remained largely positive for issuance during the first quarter, despite bouts of volatility arising from US President Donald Trump’s aggressive and unpredictable tariff policies, and wider macro and geopolitical uncertainty.

The year started with strong investor appetite for risk assets, leading to flourishing collateralised loan obligation (CLO) formations and weeks of consecutive HY fund inflows. As the supply of new-money paper remained muted, spreads continued to grind increasingly tighter amid strong demand, with loan issuers on both sides of the Atlantic riding another repricing wave.

However, rising global trade and geopolitical tensions, coupled with concerns over economic growth and inflation, soured investor appetite for risk, which culminated in a sell-off across debt and equity markets at the start of March. Consequently, spreads widened on the back of cooling investor sentiment, bringing a halt to the repricing streak in the red-hot loan market, with several issuers pulling opportunistic deals from the market.

Despite the recalibration of investor sentiment, market technicals remain favourable for loan and bond issuance. Yet beyond the recent launch of a jumbo EUR 7.45bn-equivalent loan and bond package backing CD&R’s buyout of Opella, Sanofi’s consumer healthcare products unit, the near-term supply of new-money paper looks relatively slim. The long-awaited resurgence in mergers & acquisitions (M&A) and leveraged buyout (LBO) activity has yet to materialise, with expectations now being pushed to the second half of 2025 and beyond.

Last year’s optimism over the prospect of Trump’s administration unleashing M&A activity propelled by deregulation, lower corporate taxes and higher growth has waned, as concerns mount over the impact of tariffs, labour force disruptions and government spending cuts on the US economy in 2025.

At its last meeting in March, the Federal Reserve (Fed) left benchmark rates unchanged at 4.25%–4.50% because of economic uncertainty, though policy makers are still expected to deliver rate cuts later in the year.

The European Central Bank (ECB) announced 50 basis points (bps) of cuts this quarter, lowering the deposit rate to 2.5%, while the Bank of England trimmed its base rate by 25bps to 4.5% in February. There are expectations of additional rate cuts in the Eurozone this year; however, these will depend on the impact of energy prices, plans for higher government spending on defence, and US tariffs on European exports on inflation and growth.

To continue reading and get access to more content...

A service of

Start your trial. Today

Explore unlimited content like this, available only in the platform.

Already a client? Sign in