Geopolitical shock to execution risk: Why Gulf investors need human intelligence

- Conflict shifts focus to operational and infrastructure risk

- 1Q26 dealmaking persists but weakens to post‑2020 lows

- Intelligence‑led due diligence becomes critical in managing deal execution

The war in Iran has abruptly altered the Gulf’s long‑standing perception as a stable operating environment. But while it disrupted 2025’s M&A momentum, investment flows into the region have continued, albeit at a slower pace.

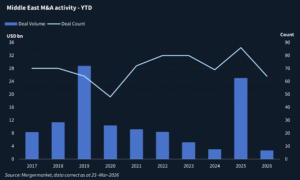

According to Mergermarket, the number of deals recorded in the Middle East fell to 64 in 1Q26 from 86 in 1Q25, the lowest first quarter tally since 2020.

The decline in investment is also due to regional sovereign wealth funds cutting costs and shifting strategy.

In 2025, Saudi officials urged the Public Investment Fund (“PIF”) to scale back domestic spending. As part of its new 2026-2030 strategy, the PIF has paused several megaprojects, including the futuristic city, The Line, and is refocusing investment on strategic sectors, while scaling back in other areas such as real estate. In early 2026, PIF’s Governor Yasir Al‑Rumayyan stated that the fund would place greater emphasis on attracting global asset managers rather than pursuing direct PIF investment.

Now, the critical challenge for investors in the Gulf is distinguishing headline‑driven geopolitical noise from genuine operational risk.

The first question investors are asking is whether operations can remain safe, predictable, and commercially viable over the next quarter and over the longer term. While most sectors in the Gulf remain functional, attacks on energy infrastructure have forced companies to increasingly rely on alternative logistics routes and to navigate more restrictive insurance requirements. Their concerns centre on the vulnerability of energy and shipping corridors, and on whether staff and supply networks can function reliably under current conditions.

Information Friction Rises

At the same time, information is harder to verify. As illustrated by recent shifts in regional due‑diligence practices, existing and potential investors in the Gulf depend more heavily on on-the-ground human‑source insights and forward‑looking scenario analysis to understand potential disruptions.

Since the escalation of the conflict in early 2026, public corporate registries in the UAE and Saudi Arabia – normally reliable sources for basic corporate filings and licensing documentation – have become intermittently inaccessible. Corporate filings are frequently delayed, and several commercial databases have stopped updating records, forcing investigators to corroborate even basic information through alternative channels.

Several Gulf courts, particularly in the UAE, have temporarily shifted to remote hearings to maintain continuity of legal processes, and while this has helped prevent system level disruption, it has also required due diligence teams to adjust how they obtain and authenticate court records.

As a result, reliance on human‑source intelligence and manual document retrieval from registries, free‑zone authorities and regulators, has increased. And despite longer lead times, site visits and in‑person enquiries are taking on greater importance.

From Conflict Shock to Prolonged Investment Risk

Meanwhile, investors are increasingly questioning whether regional infrastructure can remain functional over extended periods, whether export volumes are sustainable, and what alternatives are available should the Strait of Hormuz and surrounding maritime routes remain disrupted.

The conflict has already undermined the Gulf’s long‑standing image as a safe operational haven. If hostilities persist, the region risks further reduction in foreign investment, delayed expansion plans, and increasing difficulty in attracting highly skilled labour.

As noted by the International Energy Agency, disruptions to energy markets are likely to outlast the direct military exchanges themselves, even if US bombing in Iran stops soon.[1]

Although a prolonged conflict runs counter to Gulf states’ interests, the demonstrated vulnerability of critical energy assets is prompting regional governments to press the United States to sustain an extended military posture, with the objective of sufficiently degrading Iran’s strike capabilities and deterring further attacks.[2]

The escalating security environment is already producing immediate investment repercussions. Financing and insurance for energy, logistics, and shipping projects have become more constrained, while several Gulf-based energy companies have faced credit rating downgrades following direct strikes on LNG and gas infrastructure.

Despite the volatility, the Gulf’s fundamental administrative and commercial infrastructure remains intact. Overland routes through Oman and Saudi Arabia continue to absorb rerouted freight volumes and currently offer the most reliable alternative to disrupted maritime routes.

Gulf governments have also demonstrated meaningful capacity to absorb attacks, restore partial operations quickly, and maintain continuity in critical sectors such as finance, energy distribution, telecommunications, and logistics.

What Investors Should Do

For investors, the implication is clear: while the Gulf remains operationally viable in the near term, sustained uncertainty around security and energy flows is reshaping risk assessments and compressing the region’s margin for error, necessitating more rigorous due diligence and a reassessment of assumptions that previously underpinned long‑term investment decisions.

To manage exposure effectively, investors should focus on the following:

- Map supply chain dependencies, with particular focus on exposure to high-risk maritime routes, free zones and ports, and alternative overland corridors.

- Increase reliance on human‑source intelligence, to compensate for degraded access to digitized records and to validate the operational condition of critical assets.

- Assess risk at a granular level, focusing on specific cities, ports, corridors, and logistics clusters rather than relying solely on national‑level indicators.

- Enhance institution-level due diligence, covering regulatory position, government touchpoints, compliance history, access to insurance, and operational resilience.

- Embed dynamic regional monitoring into diligence, evaluating how shifts in conflict dynamics could affect individual assets, operations, and transaction timelines.

The conflict involving Iran is reshaping operational realities across the Gulf, but it has not brought the region to a standstill. As the gap widens between geopolitical headlines and actual execution risk, the ability to distinguish perception from operational fact has become decisive.

In this environment, adaptive, forward-looking due diligence, grounded in verified, multi‑source information, remains the most reliable means of separating manageable exposure from genuinely disruptive risk. Investors who rely solely on desk-based analysis increasingly risk misanalysing that exposure. The competitive advantage lies with those who can validate information on the ground, maintain monitoring, and anchor investment decisions in operational reality rather than geopolitical noise.

Blackpeak is trusted by top financial institutions globally, with a specialized due diligence approach to comprehensively assess risks; from discreet investigations to desktop research, industry interviews, and site visits. We ensure each opportunity is leveraged for optimal outcomes and delivers to you actionable insights that drive informed decision-making.

Want to learn more about how Blackpeak can help you?

Get expert guidance now by connecting with one of our specialists.

[1] https://www.ft.com/content/09524a74-db3c-4aef-b4f7-51eda3068320?syn-25a6b1a6=1

[2] https://apnews.com/article/trump-iran-saudi-arabia-mbs-gulf-war-uae-89f690b952fe28d3140c537b70fa5051

A service of

Navigate complex markets and risk with confidence. Today

Global due diligence specialists helping you stay ahead of uncertainty.