Sponsors rack up more key-takings than IPOs among 2020-2021 European buyouts – Dealspeak EMEA

- Buyout overhang forces sponsors into structured exits as valuations lag

- High entry multiples drive brutal CAGR maths for returns pathway

- Creative exits among DPI pathways amid 2026 exit pressures

With key-takings outpacing IPOs by almost two-to-one, it’s clear sponsors have been struggling to derive hoped-for returns from buyouts transacted in the frothy early years of the 2020s.

Undertaken at peak multiples – and just ahead of a rates cycle that threw focus on value creation – GPs still have to deliver realisations from two-thirds of these 2020-2021 investments.

The size of this overhang now determines the ultimate route to traverse it.

Against the backdrop of fund lifecycles, maturities and LPs’ liquidity requirements, sophisticated structuring and price accommodation will be necessary to sidestep valuation gaps and avoid the worst consequences of vintage risk becoming a reality.

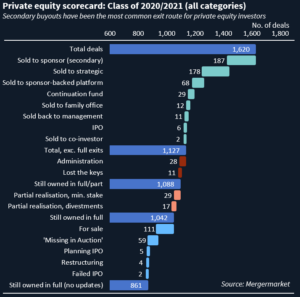

Across 1,620 financial sponsor deals struck in 2020 and 2021, there have been 11 key-takings against just six IPOs, according to data compiled by Mergermarket. Some 1,042 assets are still owned in full.

With these assets edging out of the standard private equity holding period, it’s clear 2026 is crunch time to deliver DPI across these assets.

Indeed, market conditions may have made it hard to exit up until now, but AI disruption further complicates GPs’ path to success: a quarter of these 2020-2021 investments featured targets in the technology sector.

Some attempts to offload these assets at a valuation sufficient to generate reasonable returns have already flamed out: 61 have tried to sell or list and subsequently failed. Groups such as BC Partners-owned Davies Group, White Bridge’s Named, and Apax/Carlyle’s PIB Group all faced high bid-ask spreads.

Even success comes with a caveat. Of the six listings that got away, only L Catterton’s IPO of Birkenstock achieved a market capitalisation of more than EUR 5bn – and just over two years since its debut, the stock remains 10.4% below its issue price.

Put together, public markets allocator-caution over facilitating larger sponsor exits from this investment class is understandable.

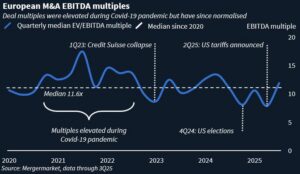

Purchase prices across the class of 2020-2021 were juiced by sky-high multiples, alongside EBITDA figures often heavily adjusted for coronavirus-related one-offs – and these deals were financed by some of the lowest debt financing costs in a generation.

In the third quarter of 2021, median EV/EBITDA multiples peaked at 17.5x – well above a five-year median of 11.6x since the start of 2020.

he maths to deliver strong returns are consequently daunting.

To hit an IRR of 20%, sponsors will typically need to have delivered revenue CAGR in the region of 15%-25%, alongside a doubling of EBITDA, to offset multiples contraction over their typical three-to-five-year hold period.

In a period of inflation and higher rates, wage and supply-chain pressures, and geopolitical instability, that’s no mean feat.

“A lot of companies in those years took three years to grow into their valuations,” said one banker.

“This is not just about multiples and adjustments but also that many took longer to deliver on growth plans in an era of a higher cost of capital.”

Most of the companies that sponsors have managed to exit cleanly are – unsurprisingly – those that managed the heavy lifting on EBITDA.

MPM Products expanded EBITDA from GBP 12m at 3i’s entry in 2020 to around GBP 30m at exit to Partners Group last year – despite temporary tariff‑related market disruptions. At the upper end of the spectrum sits Namirial, which grew EBITDA from roughly EUR 12m under Ambienta’s ownership to around EUR 65m at its sale to Bain Capital.

The prospective IPO of TK Elevator could also put sentiment on a more positive footing. Even if sellers Advent, Cinven and RAG-Stiftung list the group at an EV/EBITDA multiple below the 17x at which it was originally acquired, they could be set for a solid return after a six-year hold period.

The prerequisite for a smooth exit is undoubtedly operational capability – it is the dividing line between success or failure.

In that race, managers who had been focused on value creation even when multiple expansion did most of the work have enjoyed a head start.

Others have been less fortunate. Companies unable to execute their M&A plans, or falling foul of operational mistakes, have been likelier to trip covenants, resulting in key-takings. One notable example, Carlyle’s loss of END Clothing to Apollo, resulted from the failure of a new stock management system.

When sponsors have achieved enough with their portfolio companies to secure an exit, they are nonetheless having to be more creative than ever to complete them.

From the class of 2020-2021, there has been four times as many continuation fund solutions as IPOs, as sponsors sought to lock in high IRR and distributions ahead of fresh fundraising attempts. Thus far predominantly formed of trophy, single-asset funds, we expect the multi-asset restructuring tool to return as a liquidity mechanism as sponsors look to broaden their exit options for the 2020/2021 class of deals.

Even the largest and cleanest exits – secondary buyouts and strategic M&A – have frequently relied on structural optimisation to square valuation gaps.

Vendor equity rollovers, deferred consideration, vendor loans, earnouts and short-dated instruments have become standard features of deals, allowing sellers to preserve headline pricing while buyers seek to protect returns. These mechanisms push some risk into the future, but they also allow assets to change hands – something paper valuations alone cannot.

Expect more of this throughout 2026.

The blunter instrument is price. With distributions already constrained and GP activity likely to narrow, some assets will have to come to market – quietly, selectively and often at discounts that would have been unthinkable four years ago.

Can an LP forgive a markdown or a bad vintage? The answer is surprisingly unanimous: it depends how much the GP overpromised in the first place.

In the end, this is a story of accumulated strain: portfolios that should be exiting, funds long on assets and short on liquidity, and markets behaving as if time were abundant when it is not.

What follows now is not a clean reopening of the window, but an overdue reckoning with what needs to go through it.

This article is the first in a series examining how private equity investments made during the 2020-21 cycle are playing out. Subsequent pieces will break down sector trends, sponsor-specific outcomes and the state of the equity capital markets.

A service of

Your M&A Future. Today

Explore unlimited content like this, available only in the platform.

Already a client? Sign in

A service of

Start your trial. Today

Explore unlimited content like this, available only in the platform.

Already a client? Sign in

A service of ![]()

Shape your future with Dealreporter.

Explore unlimited content like this, available only in the platform.