Sponsors brace for busy year as deal momentum builds – North America Private Equity Trendspotter

- Exit market challenges persist, but transaction volume rose 24% in 2024

- Favorable credit markets to buoy buyout activity

- Tech, healthcare buyouts dominate, with focus on AI-insulated companies

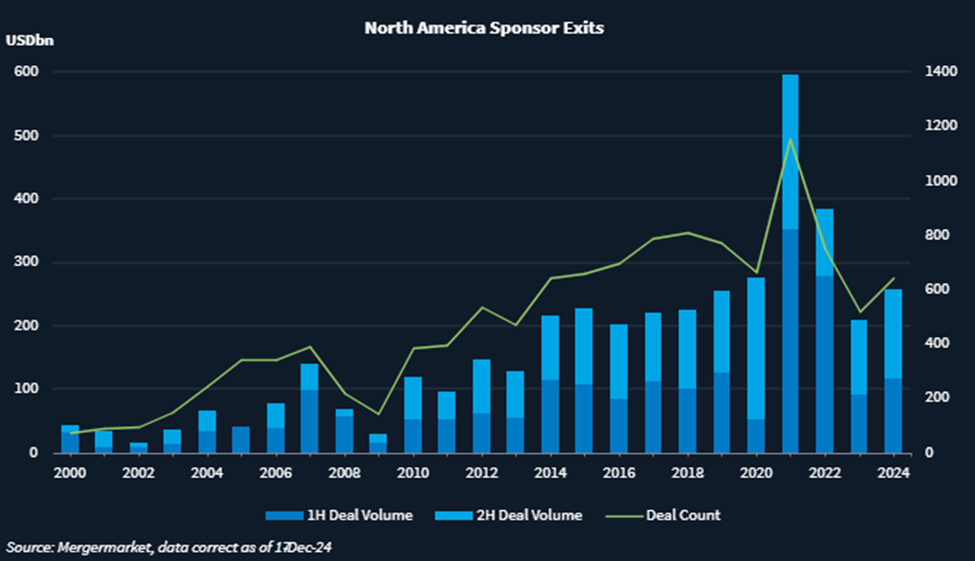

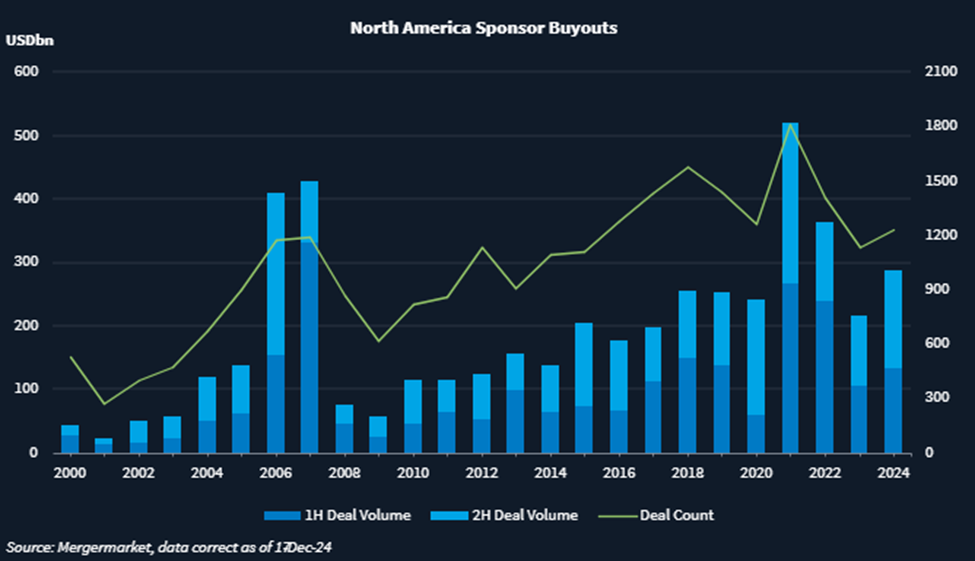

After a two-year slowdown in the cycle of private equity fundraising, deployment, and exits, 2024 represented a turning point. Sponsor-led buyout volume rose by 32% year-on-year to USD 286.6bn, making 2024 the third-best year in the last decade, following the record years of 2021 and 2022. While the exit market remained challenging, transaction volume reached USD 258.2bn, a 24% increase from the market trough of 2023.

Although these figures still pale in comparison to the market peak in 2021, momentum is gradually building as we head into 2025. Several factors point to a continued pickup in activity including clarity over interest rates, favorable financing markets, and the advent of a new administration in Washington deemed to be deal-friendly.

“I think it’s going to be pretty robust,” said Chris Gordon, partner and global co-head of private equity at Bain Capital. “Market dynamics are improving and we’re seeing fewer instances of where buyers and sellers can’t agree on price.”

Exit bottleneck

Wide bid/ask spreads were certainly one factor that stymied exit volumes last year. The largest exit was Berkshire Partners and Leonard Green & Partners’ sale of SRS Distribution to Home Depot [NYSE:HD] for USD 18.2bn in March, followed by the USD 13.4bn sale of of AssuredPartners by Apax Partners and GTCR to Arthur J Gallagher in December, a deal that is yet to close.

These deals reflect a key theme in exit deal flow in 2024: the preponderance of industry-leading companies that would command premium pricing in any market.

In a year marked by lingering uncertainty over the direction of interest rates — until the Federal Reserve slashed its benchmark rate by a half point in September — the persistence of valuation mismatches caused many processes to stall or fail to launch.

Looking ahead, there remains a degree of uncertainty around interest rates. However, last week, Federal Reserve Governor Christopher Waller was quoted as saying that rate cuts could come more quickly than expected.

“For businesses that are performing well, it’s an appealing time to sell unless you have high conviction that interest rates will drop significantly,” said Gordon.

Against that background, dealmakers say many sponsors are busy preparing transactions. Alex Temel, global co-chair of the private equity practice at Paul Hastings, is seeing deals that failed to get off the ground last year come back.

“The first two weeks of December were insane in terms of deal flow,” he said. “All those stalled sale processes resumed.”

Last month, it was announced that CD&R was selling greeting cards manufacturer American Greetings to Elliott Investment Management, with the deal expected to close in the first quarter of this year.

Sponsors say their exit pipelines are building. Justin Steil, a partner and co-head of the North America transaction team at MiddleGround Capital, said the Lexington, Kentucky-based sponsor could exit several portfolio companies in 2025.

“We’ve now owned a number of companies for a reasonable time frame that have performed well,” he said. “We don’t try to be market timers, and not everything has to be perfect for us to generate the kinds of returns we’re targeting.”

Credit competition

A favorable credit market is another factor expected to support increased deal flow in 2025.

Sponsors are benefiting from favorable pricing. MiddleGround, for instance, has recently executed credit amendments and refinancings for a number of its portfolio companies, according to Steil.

“We’ve got super conducive financing markets, on both the broadly syndicated side and the private credit side,” agreed Tom Amster, global head of the financial sponsors group at Macquarie Capital. “Those two markets are competing against each other now, driving down financing costs for the benefit of equity firms.”

Despite this competition, credit market participants are also increasingly working together to fill financing gaps.

“The market is finding this really nice balance between syndicated debt and private credit,” said Jeremy Goff, a managing director at credit investment firm Palmer Square. “Asset managers, banks and insurance companies are playing together and cooperating, and finding ways for these two worlds to exist.”

Tech, healthcare buyouts at the fore

The largest buyout in 2024 was the acquisition of Truist Insurance by investors led by Stone Point Capital and CD&R in February in a deal that valued the target at USD 15.5bn in enterprise value. This was followed by a deal that saw KKR [NYSE:KKR] take a 50% stake in Cotiviti Holdings alongside Veritas Capital, valuing the healthcare technology company at over USD 10bn.

Overall, technology was the leading sector for buyouts, with a deal volume of USD 115.2bn of transactions, contributing 40% to the total for North America. This notably included a USD 6.4bn equity investment in Vantage Data Centers Management led by DigitalBridge Group and Silver Lake Group in January.

Technology and healthcare are expected to feature prominently again this year. “Healthcare is very active, especially for technology companies servicing the healthcare space,” said Paul Hasting’s Temel.

Meanwhile, infrastructure-related sectors, including data centers and artificial intelligence (AI)-supporting infrastructure, are also becoming increasingly important. “Anything that supports AI will continue to be hot,” said Macquarie’s Amster. “Every company’s a tech company at some level, and now I like to say every company’s an infrastructure company.”

Across a broad swath of industry verticals, sponsors are focusing on companies that can use AI to enhance their margins. Some are even stepping away from transactions where companies could be negatively impacted by AI.

“The biggest trend for next year will be companies that are AI-insulated,” added Temel. “Sponsors are asking how AI and machine technology will impact companies, change margins, and affect labor needs.”

Internally, sponsors have ramped up their efforts to tackle the AI challenge. “We spend a lot of time in investment committees and with portfolio companies thinking about AI’s risks and opportunities,” said Bain’s Gordon.

Fundraising challenges

Leveraging AI at the portfolio company level is part of a broader focus on value creation in the last few years, in an environment characterized by a dearth of exits. “The industry shifted two years ago to focus on value creation, getting back to nuts and bolts, not just relying on cheap money and low interest rates,” said Glenn Mincey, global and US head of private equity at KPMG.

Sponsors turned to creative solutions to distribute capital back to their limited partners in a challenging environment for fundraising. Most notably, the secondary market has helped ease liquidity pressure. In 2024, total secondaries transaction volume reached a new record at around USD 150bn globally, according to market estimates. Sponsor appetite for continuation vehicles drove general partner-led secondary market deal flow up by 94% in the first half, according to Evercore.

The appetite for continuation vehicles is expected to remain strong, even as traditional exits pick up, according to market participants.

“General partners have had good experiences with GP-led deals, and many are completing their third, fourth, or even fifth GP-led transaction, validating the merits of this approach,” noted Jeff Keay, chair of the secondary investment committee and a managing director at HarbourVest.

KPMG’s Mincey agrees that continuation vehicles are an established part of strategic decision-making for any sponsor considering an exit.

“Dual-track processes will continue,” he predicted. “But it’s more than just private sale or initial public offering now; it’s also continuation funds and the secondaries market.”

A service of

Your M&A Future. Today

Explore unlimited content like this, available only in the platform.

Already a client? Sign in