Newmont target Newcrest has let slip the dogs of war but can it manage their expectations?

Australia’s largest gold miner Newcrest Mining [ASX:NCM] chose to unleash its vociferous shareholder base in response to the indicative AUD 24.4bn (USD 16.9bn) all share takeover approach from US gold miner Newmont [NYSE:NEM, TSE:NGT]. Several, including the miner's largest shareholder, responded vocally telling the media unequivocally that the terms needed to be significantly improved.

Can Newcrest, which is currently being led by an interim CEO, now manage their expectations while in the crosshairs of the acquisitive mining giant?

The prospects of an agreed deal look firmly to hinge on whether their respective boards can agree to terms that their own shareholders think make sense. The regulatory and rival bid risks look manageable.

As this news service reported last week, antitrust and national security regulatory reviews, whilst not negligible, do not appear problematic. Meanwhile, the rival bid risks look low. Gold mining giant Sibanye-Stillwater Ltd [JSE:SSW] has said it is focused on building a geographically diverse green metals company. Mark Bristow, CEO of Barrick Gold [NYSE:GOLD, TSE:ABX], one of the perceived most logical rival bidders, has said he is focused on organic growth and Agnico Eagle [NYSE: AEM, TSE: AEM], another player with the scale to acquire Newcrest, appears interested in other M&A opportunities.

Whilst the deal may, in part, be designed to capture Newcrest’s material copper by-product at Cadia in NSW Australia and Red Chris in Canada, it looks largely to be about gold mining consolidation and gaining scale. Newmont already owns the Boddington and Tanami mines, the largest and third-largest gold mine in Australia, and consolidating Newcrest’s Cadia mine in NSW Australia and Lihir mine in PNG would put the four largest mines in Australasia under one group.

The deal rationale has its critics. Some analysts have questioned the extent of synergies that can be achieved due to the mines’ geographic spread. And Bristow, who has an antagonistic relationship with Newmont, has thrown in a grenade by questioning whether its “just to be bigger or for real value”.

However, shareholders that have spoken out in recent weeks seem more focused on the terms than the deal's rationale.

But that does not mean putting a transaction together will be easy. Our report last week suggested the two parties are some distance away from signing an NDA to allow Newmont access to Newcrest’s books so it can table an acceptable offer. That distance might be down to the different valuation expectations of the respective boards’, and both sets of shareholders.

Over the past few days, Newcrest has been meeting with shareholders in Sydney and Melbourne. According to one source with knowledge of the meetings, Newcrest is trying to drum up support to push for a higher offer. It will be interesting to learn how these meetings go.

Newcrest is in a bit of a leadership vacuum following the departure of former chief executive Sandeep Biswas who retired in December. Sherry Duhe, who joined the company in February 2022 as CFO, is the interim CEO while a global internal and external search for a replacement is underway.

All of these factors most likely explain why news of the Newmont bid first appeared in the Australian Financial Review’s Street Talk column on Sunday 5 February. That leak allowed Newcrest’s board to share the terms of the indicative bid approach with its shareholders. As the board probably anticipated, they had strong views, which they relayed to the press over the following few days.

Chief investment officer Simon Mawhinney of Allan Gray, the miner’s largest shareholder (7.36%), said the merger “might make sense but I am not convinced the relative value on offer strikes the right balance”. Investors Mutual portfolio manager Tim Wood said “the offer was not high enough”, adding that the proposed all-share offer comes with significant price risk on currency fluctuations. Argo senior investment officer Andy Foster argued a “massive control premium” is lacking. Pendal shared the same view: Newmont “need to pay up for it”.

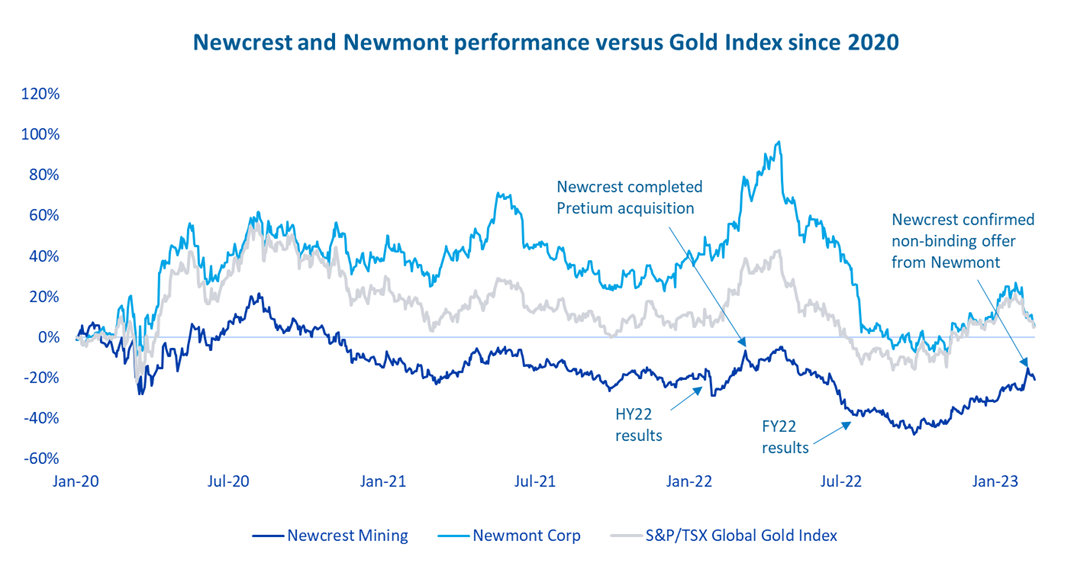

Newcrest shareholders may also argue Newmont’s offer comes as Newcrest shares underperform the S&P/TSX Global Gold Index and doesn’t sufficiently factor in generally positive sentiments on the gold price. Meanwhile, Barroenjoey analyst Dan Morgan has suggested Newcrest run a strategy day to convince investors of its worth and also suggested the company could carry out a strategic review of its non-core assets to enhance shareholder returns.

Evaluating the merits of what would be the biggest M&A deal this year whilst assessing and communicating the company's standalone prospects is a lot for an interim CEO run company to handle.

Consider also that Newmont appears to be using bear hug M&A tactics. As early as 6 February, "a source close to management" had told Reuters that it is open to slightly increasing its offer. Whether or not the deal makes strategic sense is open to question but 11 of Newmont’s 12 board members have M&A execution experience and the miner knows how to get deals done.

It has already told Newcrest, for instance, that it is “contemplating” the establishment of a Chess Depository Interest listing on the ASX for new Newmont shares to be issued Newcrest shareholders. In 2015, the inclusion of CDIs helped Iron Mountain [NYSE:IRM] secure support from shareholders of Australia’s Recall Holdings in the protracted negotiations around that scheme deal.

Whether Newmont has anticipated any resistance from its own shareholders is unclear. Flossbach von Storch, the Germany-based asset manager, which is a top 10 Newmont shareholder and a top three actively managed shareholder, has said the proposed deal makes sense but that it “did not want to see big premium’s paid”.

The proposed share exchange structure means the deal will require a Newmont simple majority shareholder vote. Under Section 312.03 of the NYSE Listed Company Manual, any issuance of common stock equal to or in excess of 20% of the voting power of the existing common stock requires approval from a simple majority of shareholders. This threshold will easily be breached by the terms of Newmont’s rejected revised exchange ratio of 0.380 Newmont shares for each Newcrest share.

On the plus side for Newmont, it has many of the same shareholders as Newcrest. Behind Allen Gray, these cross-shareholders include Blackrock, Van Eck, State Street, Vanguard, First Eagle. These funds, some of which are passive index funds, will be helpful in getting a deal across the line.

Nonetheless, shares in Newmont fell to USD 47.60 from USD 49.85 on news of the bid and have since slipped to USD 45.42 – the lowest close since November. This will not have gone unnoticed by its board or both sets of shareholders. Shares in Newcrest, meanwhile, jumped more than 10% to AUD 25.6 following news of the approach but have since drifted in sympathy to AUD 23.59, which is still above the AUD 22.45 undisturbed closing price on 3 February.

As of Newmont closing on 10 February, the rejected implied offer valued Newcrest at AUD 26.06 apiece. Now it values Newcrest at AUD 24.99, which is a lowly 11.31% premium to the undisturbed price. The deal is trading with a 5.89% spread but the market implied probability, using the undisturbed downside price, is just 45%.

So, how to resolve the bid-ask spread?

Newcrest and its leading shareholders are right to push for a bump to the offer price based on precedents.

Recent mining and resources deals have returned to paying premiums. Kinross Gold's [NYSE:KGC] USD 1.4bn acquisition of gold miner Great Bear Resources, which completed in February 2022, offered a 31% premium to Great Bear's undisturbed price. BHP’s [ASX:BHP] acquisition of Oz Minerals [ASX:OZL], which, admittedly is not a pure gold mining consolidation play and more a part of BHP’s transition toward green metals, paid a 49.3% premium to the target’s undisturbed price.

Even the ongoing USD 4.8bn cash and scrip sale of Ontario-based Yamana Gold [TSX:YRI; NYSE:AUY; LSE:AUY], which is set to be broken up by Agnico Eagle [TSX: AEM, NYSE: AEM] and Pan American Silver Corp [TSX: PAAS, Nasdaq: PAAS] after they gate-crashed a bid by Gold Fields [NYSE:GFI, JSE:GFI] achieved a 23% premium to its spot price on 3 November.

On a multiples basis, the Newmont proposal provided a 8.54x EV/EBITDA valuation for Newcrest. This is a little below the multiple of other billion-dollar gold miner deals in recent years, which have fetched a median EV/EBITDA of 9.2x. Among them, Newcrest’s USD 2.8bn acquisition of Pretium Resources in 2021 was completed at 8.97x. Kirkland Lake Gold paid 13.21x EBITDA to purchase Canada’s Detour Gold in a USD 3.7bn deal in 2019 while Newmont’s own USD 12.7bn acquisition of GoldCorp in 2019 valued the Canadian miner at 12.97x EV/EBITDA.

What Newmont can do to get a deal done

Newmont has been here before. After it announced the then approx. USD 12.5bn tie-up with Goldcorp in early 2019, its shares nose-dived around 10%. Newmont’s shareholders were put off by the perceived steep 17% premium over Goldcorp’s 20-day vwap. But the company subsequently managed to fend off a bid from Barrick and then overcame concerns from shareholders Paulson & Co and Van Eck by sweetening the Goldcorp deal with the “largest dividend in 32 Years”.

Newcrest and Newmont are both operating at low leverage of 0.65x and 0.48x net debt / EBITDA respectively. While Newcrest only has USD 565m cash on hand as of 30 June 2022, Newmont has USD 3.1bn.

Newmont can sweeten this deal, but will it be enough for the Newcrest board and shareholders?

Our analysts pick out hints of future material developments in M&A, ECM and Event-driven situations by combing through transcripts, stock exchange filings, analyst reports and news stories. This raw data is combined with proprietary insights and commentary to produce an exclusive report that offers short and long-term actionable ideas (no investment action should be taken without further investigation). If you have any ideas for coverage please email [email protected].

A service of

Your M&A Future. Today

Explore unlimited content like this, available only in the platform.

Already a client? Sign in