New directions: AI ubiquity, risk exposure, and pursuing scale in global tech M&A

9th December 2025 01:40 PM

This report, published in association with Morrison Foerster, features a survey of 300 tech dealmakers from around the globe. It aims to gain their insights into what precisely is driving tech M&A strategies in the near and medium term.

Key findings include:

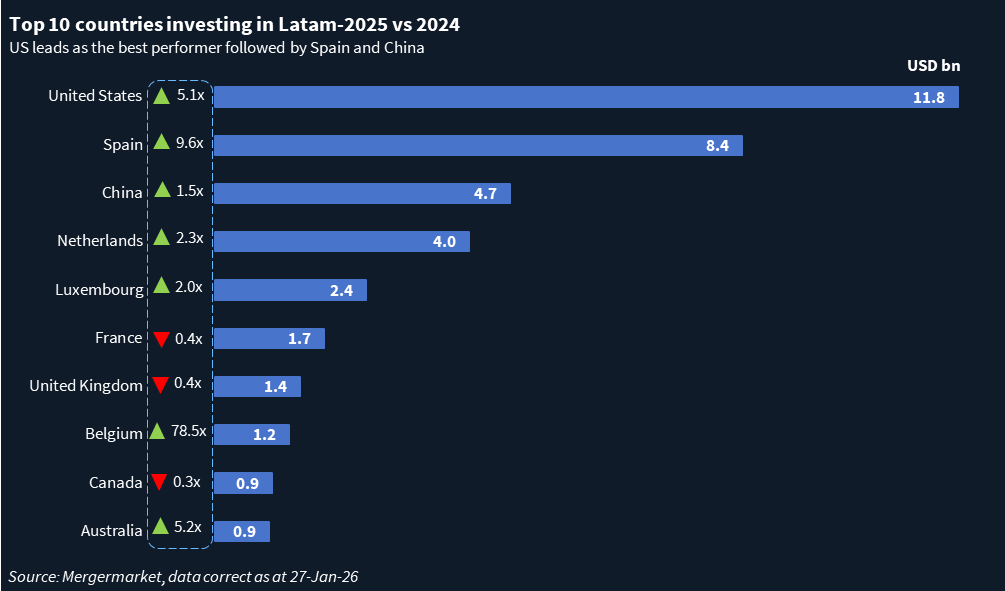

- Deal Value Soars. According to Mergermarket, the aggregate value of all deals announced globally in the computer software, hardware, and semiconductors subsectors through the first three quarters of 2025 reached $845.9 billion, up 72.2% year-over-year. Deal volume, however, continues to trend down—acquirers announced 6,551 transactions in these subsectors in Q1-Q3 around the world, down 9.3% from the same period in 2024.

- Startup Season. Respondents continue to indicate a marked preference for targeting young companies (those operating for between two and five years) in M&A. This year, startups are clearly in the lead, garnering 50% of first-choice votes. Dealmakers are looking to capitalize on the high-growth opportunities of industry disruptors in subsectors such as AI and cybersecurity.

- Return to Form. More than half of survey respondents (57%) expect tech M&A deal volumes to increase over the next 12 months. Nearly two-thirds (64%) expect the average value of tech M&A transactions to rise over the same time period.

- Limiting Risk. PE dealmakers expect to be increasingly likely to employ minority investments (97%) and contingent consideration/earnouts (84%) in their tech M&A strategies over the coming 12 months. Their corporate peers intend to focus much more on joint ventures (84%) as they continue to pursue growth while limiting their risk exposure.

- Europe at the Forefront. Respondents expect Europe to offer the best opportunities for tech M&A over the next 12 months, with the region garnering 30% of first-rank votes, the largest such share.

- Seeking Clarity. Respondents believe the greatest obstacle to the continued growth and uptake of AI technologies will be increasingly strict regulation (40% of top two votes) and a lack of transparency in the industry (38%).

- AI Unstoppable. Respondents believe the AI space presents the best opportunities for dealmaking over the next 12 months—70% of respondents identify it as a top-three subsector, superseding cybersecurity (54%), which had claimed the top spot in the two most recent editions of this survey.

- Leveraging AI. The sectors that our respondents believe are currently best leveraging the power of AI are, unsurprisingly, technology (68% of top-three votes) and business services (61%).

The report is also available at mofo.com

In association with

A service of

Your M&A Future. Today

Explore unlimited content like this, available only in the platform.

Already a client? Sign in