M&A Highlights 2024: Return to growth

Powered by Mergermarket data, M&A Highlights reviews M&A activity across North America, EMEA and APAC in 2024. All data correct as of December 16, 2024

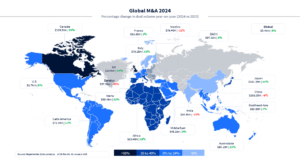

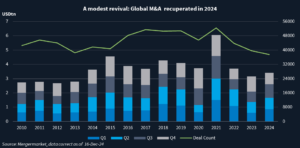

Global M&A recovers from decade low

Global dealmaking enjoyed a modest recovery in 2024 but remained suppressed historically.

M&A volume reached USD 3.4tn, up 8% from 2023’s 10-year low.

Despite the cautious recovery, the portents for a stronger 2025 are good after central banks in the US and Europe began dropping interest rates and some political certainty returned following a record number of elections around the world.

Donald Trump’s win as US president, combined with the Republican party’s sweep in Congress, have left dealmakers anticipating a rise in US dealmaking in 2025 thanks to the promise of lower corporate taxes, deregulation and leadership changes at key regulatory agencies. Fueling the optimism is the expectation that inflation can be tamed and that the Federal Reserve can achieve its soft economic landing.

“People are excited,” said Louis Lehot, a partner at Foley & Lardner. “But I would not say the pipeline is full. People are going to wait until the beginning of the year to see who is in charge” of the regulatory agencies.

The technology, financial services, manufacturing, oil and gas, and healthcare sectors are all expected to benefit.

Corporates Go Big

North America took 49.8% of global deal volume, up from 49.1% in 2023. Europe, Middle East and Africa took 24.7%, up from 24.2%, and Asia Pacific 22.7% in 2024, down from 22.9%.

Larger deals continued their recovery in 2024, with the number of USD 2bn-plus transactions increasing 20% year over year. The number of mega deals – defined as those valued at USD 10bn or more – increased to 37 from 35 in 2023.

Corporates continued to be in charge, as financial sponsors shied away from mega transactions. Nine of the year’s top 10 deals involved large strategic acquirors. The other deal was the USD 38bn corporate spinoff of General Electric’s [NYSE:GE] electricity business, called GE Vernova [NYSE:GEV], to existing shareholders.

The year’s biggest deal was the USD 58.4bn bid for Japan-based Seven & I Holdings [TYO:3382], owner of the 7-Eleven convenience store chain, by Canadian grocery group Alimentation Couche-Tard [TSX:ATD] in September. The deal propelled global retail sector M&A volume to USD 114bn, up 124% year over year.

In August, Mars paid USD 36.1bn for Kellanova [NYSE:K], maker of Pringles and Pop-Tarts, in the biggest transaction in nearly a decade for North America’s food sector.

Two upstream oil and gas deals featured in the top 10: Diamondback Energy’s [NASDAQ:FANG] USD 28.1bn bid for Endeavor Energy Resources in February and ConocoPhillips’ [NYSE:COP] USD 22bn offer for Marathon Oil in May.

Zurich-based Amcor’s [NYSE: AMCR; ASX: AMC] USD 17.7bn all-stock offer for Evansville, Indiana-based consumer packaging company Berry Global Group [NYSE:BERY] in November underscored one upcoming shift in cross-border M&A: European companies making bigger moves to acquire US-based businesses as a way to sidestep Trump’s import tariffs, a trend that also featured during his first term.

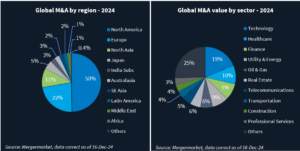

The tech sector accounted for 19% of global deal volume, up from 17% last year, but down from 24%-25% in 2022 and 2021. The healthcare sector came second with 10% of deal volume, while the finance sector came third with a 9% share.

Global buyout volume increased 34% year-over-year to USD 626bn, while exit volume rose 25% to USD 418bn, as financial sponsors returned to the dealmaking table, but that is still some way off the record levels seen in 2021.

To continue reading and get access to more content...

A service of

Your M&A Future. Today

Explore unlimited content like this, available only in the platform.

Already a client? Sign in