HR Tech M&A clocks overtime amid vendor fatigue – Dealspeak North America

- Dayforce take-private sets new record, Workday expands

- Point solutions face pressure to consolidate

- Frontline workers, payroll are dealmaking hotbeds

A wave of high-profile deals is reshaping the human resources technology landscape, signaling renewed investor appetite and strategic urgency across the sector.

In the past five weeks, three major transactions have left executives giddy.

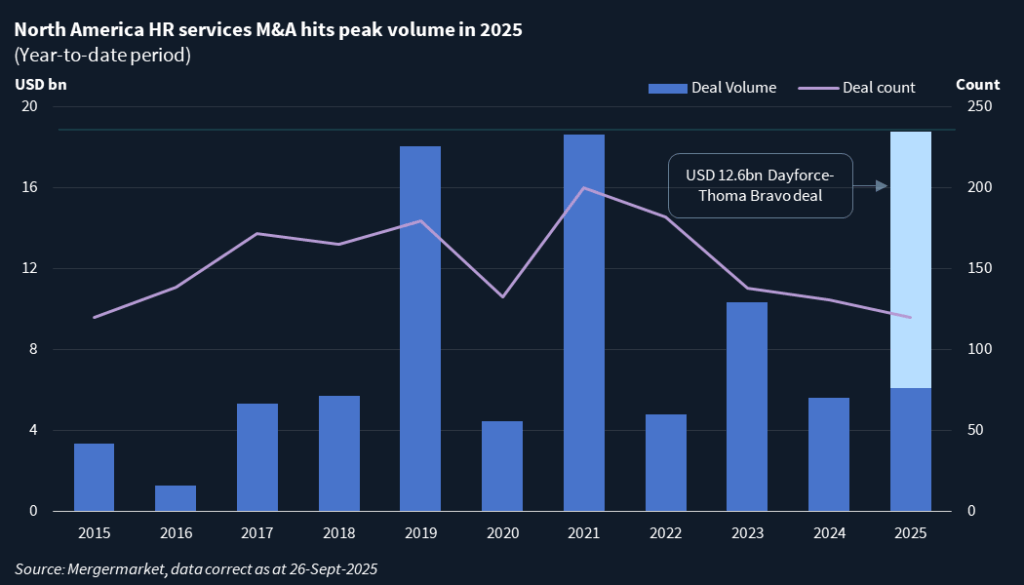

Thoma Bravo’s USD 12.7bn take-private of Dayforce, announced in late August, is now the largest HR tech deal on Mergermarket record, surpassing the USD 12.4bn merger that created UKG in 2019. Workday followed with two large acquisitions:Paradox, a recruitment software company, for USD 1bn, and Sana Labs, a Sweden-based learning and development platform, for USD 1.1bn.

“There’s something in the water,” said Sina Chehrazi, CEO of employee benefits platform Nayya, noting the elevated levels of HR tech M&A in recent months.

The recent activity comes after a three-year lull in HR tech M&A. During the first nine months of 2025, 120 deals totaling USD 18.8bn for North America-based targets were announced, according to Mergermarket data. While it is the lowest number of deals in 10 years, it is the highest by volume on record, driven by Dayforce’s take-private.

Consolidation over innovation

HR tech spans four core categories. The two largest are human capital management (HCM), which includes payroll, onboarding, performance management, and employee engagement, and talent management, which encompasses recruiting, hiring and career development. The other two are learning and development, which focuses on training and upskilling, and employee health and wellness, which covers physical, mental and emotional wellbeing.

Ron Heller, senior managing director at Woodside Capital Partners, said investment in innovation has slowed – aside from advances in artificial intelligence – while a consolidation wave is cresting as market fragmentation and vendor fatigue accelerate a shift toward integrated platforms.

“Some enterprises had up to 11 HR vendors – that was becoming cumbersome,” said Heller. Companies have started dropping some of these, putting pressure on standalone vendors to join a more comprehensive platform. “Many are realizing they’re better off as part of a broader solution, rather than a standalone point solution.” Workday, whose broader suite of products gives it pricing power, is one such home.

This consolidation trend is prompting point-solution providers to seek early exits. “You want first-mover advantage,” said Fatima Alam, executive director at Woodside. “Multiples typically go down for those selling second or third.”

Another driver of M&A is hiring activity, which has broadly struggled amid a softening labor market, said Heller. Many recruiting technology companies, which have per-employee-per-month revenue models, are facing headwinds, and will be forced to consolidate.

PE eyes sticky revenue

Although the size of Dayforce’s take-private is seen as an outlier, the deal is potentially a sign of more PE investments. “HR tech is sticky and lucrative,” said Alam. “Once you’re in it’s very difficult to switch.”

Thoma Bravo is expected to help Dayforce refocus on innovating in areas where it lagged UKG and Workday – AI, talent acquisition, internal talent mobility, and workforce management.

Paycom could be next. Its margins lag peers like SAP, Workday, Paychex, and Paylocity. While its differentiation remains unclear, one AI feature called “I want” – which allows employees to ask payroll-related questions – could offer it an edge.

Paychex’s USD 4bn acquisition in January of Paycor – one of Paycom’s biggest competitors in payroll processing – was driven by Paycor’s top-rated user experience and ability to move Paychex up market, said Alam.

Deskless workers, payroll in focus

Workday’s acquisition of Paradox reflects a pivot from desk-bound, knowledge workers – many of which have faced layoffs – to deskless or frontline workers. “Deskless workers have been the tagline for HR tech,” said Alam. “They are not going away.”

Workforce management for deskless workers is one of the hottest areas in HR, with UKG and Dayforce among the leaders, while ADP and Workday have been deepening their functionality there.

The industry is fragmented, with much room for consolidation, and tends to be incredibly sticky with customers. “I expect to see a lot of movement there,” said Alam.

Smaller companies like TCP Software, Quinyx, and Indeavor – which all focus on frontline workers – could see consolidation among them, noted Heller.

Payroll is another hotbed of M&A activity, he added.

One payroll company to watch is Vensure, which has made 14 acquisitions since Stone Point Capital acquired it in April 2021, displacing some of Paychex’s and ADP’s activity in the process. Its last acquisition came last October, signaling a potential exit may be in sight. In March, Mergermarket reported its owners were exploring a partial sale.

Other active payroll players are Accel-KKR backed iSolved HCM and Asure Software, both of which license their solutions to service providers and are now acquiring those licensees. “Almost all companies need payroll. It’s mission critical,” said Heller.

A service of

Your M&A Future. Today

Explore unlimited content like this, available only in the platform.

Already a client? Sign in