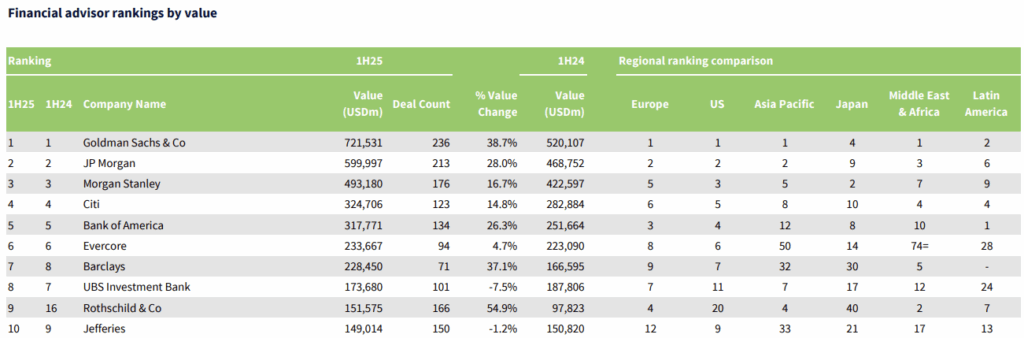

Goldman Sachs, PwC sustain top spots across 1H25 M&A value, deal count rankings

- JPMorgan, Morgan Stanley take silver, bronze in deal value stakes

- Evercore, Barclays enter European top 10

- Local advisors take seven China deal top spots

With a 25% year-on-year (YoY) boost in aggregate M&A deal values to USD 2tn balanced against the lowest deal count in 20 years, 1H25 can only be described as a period of mixed fortunes.

US President Donald Trump’s “Liberation Day” tariffs intervention yielded significant market volatility and delayed a slew of processes. Yet AI-related equity stake deals in the US, Chinese banking tie-ups, a Toyota-driven Japan M&A boom, and an uptick in sponsor exit deal values marked the half-year just as concretely as macro risk.

In such a whirlwind six months, one constant has been the top three financial advisors by deal value, according to Mergermarket’s 1H25 global and regional M&A rankings.

Goldman Sachs sustained its number one spot with a 38.7% YoY hike in deal values to USD 721bn, additionally grabbing pole position in the US, Europe, Middle East & Africa, and APAC. With sponsor LPs crying out for realisations, Goldman should be satisfied with topping the global private equity exit deal value ranking, advising the sellside on 31 deals for an aggregate USD 133.4bn, up 82.3% YoY.

In second place across the headline global rankings, JPMorgan also managed to best the global 25% hike in deal values, delivering 28% growth YoY to just shy of USD 600bn. Taking the bronze, Morgan Stanley clocked up growth of just 16.7% YoY to USD 493bn – though its sponsor exit haul of USD 119bn (up 592.9% YoY) showed remarkable progress in what has remained a challenging environment, particularly in 2Q25.

Rothschild & Co’s entry into the top 10 – climbing seven places to 9 from 16 YoY – comes off the back of a storming 54.9% YoY hike in 1H25 deal values to USD 151.6bn. Around 29 of its deals were above USD 1bn, demonstrating Rothschild’s strong position in the upper mid-market. Nomura also saw a stunning rise – to 13 from 39 YoY – clocking up an almost five-fold rise in values to USD 134.7bn, buoyed notably by the unwinding of several Japanese cross-shareholdings in Toyota.

In the 1H25 global deal count stakes, PwC also retained its No.1 position, clocking up 247 transactions, though this was down on the 1H24 haul of 344. The global advisory player’s undoubted strength in APAC – where it also topped the charts – was a major advantage in a six-month period marked by strong regional deal flow and its significant presence in South Korea.

But Goldman Sachs also stole a march on this metric, climbing into second position from fifth last year, adding 28 deals to its haul and claiming 236 across 1H25. Also jumping the charts, JPMorgan took third place with 213 deals, up from sixth in 1H24. Beating the market on both value and deal count in a volatile first half took some doing.

Europe winners

Goldman ruled the deal value roost across Europe, clocking up USD 237.4bn in deals, up by 9.2% YoY. Morgan Stanley hung on to its second place, albeit with a 3.5% YoY decline in values to USD 173.2bn. Bank of America stormed up the top 10 into third position from sixth last year, with a 71.5% YoY hike in deal values to USD 136.7bn.

Evercore and Barclays climbed into the 1H25 top 10 at eight and nine, respectively – knocking out Deutsche Bank (down to 11 from 10) and BNP Paribas (15 from eight) in the process. Evercore clocked up some impressive wins, including a sellside role acting for EQT on its partial exit of (and investors’ cash injection into) Swedish software player Industrial & Financial Systems – in total, a USD 3.3bn deal. Meanwhile, Barclays’ progress will be especially satisfying for Head of EMEA M&A Stephen Pick, who joined the bank in August 2024.

Across the region, the UK’s grim progress, with 1H25 aggregate deal values down by 27% to USD 87.2bn, was reflected in widespread drops in advisory hauls. Here again, Goldman Sachs came top with USD 58bn in deals, down by 43.3% YoY. It also took the No.1 position in DACH, Ireland, Benelux, and the Nordics.

Within DACH, UBS won the Switzerland deal value crown back from JPMorgan, which slipped to third. Elsewhere, winners include Rothschild & Co. in France; Mediobanca in Italy; and JPMorgan in Iberia and Central & Eastern Europe.

By deal count across Europe, K3 Capital Group stormed to the No.1 spot from 39 last year – proof of its reach in the SME market.

Americas winners

Across deal values, global winner Goldman Sachs (USD 549.6bn, up by 29.7% YoY) sits at the head of an unchanged Americas top six, followed by JPMorgan (USD 459.7bn, up by 21.9% YoY); Morgan Stanley (USD 365.2bn, up by 12.3% YoY); Citi (USD 258.7bn, up by 1.8% YoY); Bank of America (USD 254.7bn, up by 16.5% YoY) and Evercore (USD 213.8bn, up by 1.3% YoY).

Goldman’s mandate from Softbank in its USD 40bn capital injection into LLM giant OpenAI was a significant component of its aggregate deal value – and a further symbol of how much capital is still being put to work despite the DeepSeek wobble in January.

These banks were also the only advisors to clock more than USD 200bn in deals each. Just outside that haul was Barclays, in seventh position with USD 195.8bn – though its 48% YoY growth reflected a prominent sellside role on Wiz’s pending USD 32bn sale to tech giant Alphabet.

The top six is mirrored for the US rankings, albeit with Bank of America in fourth and Citi in fifth – a switch from the Americas read.

Goldman was top dog in the US across deal value and count for the Northeast and Midwest and by value in the West; JPMorgan benefited from Southern hospitality, taking the top spot with a USD 187.7bn haul in the region.

In Canada, Goldman was once again at the summit, but there were five new entrants to the top 10: Barclays in at No.2 (USD 41.4bn, up by 158%); BMO Capital Markets at No.3 (USD 41bn, up by 442.4% YoY); Scotiabank at No.6 (USD 33.6bn, up by 148.3% YoY); CIBC World Markets at No.9 (USD 21.7bn, up by 161.1% YoY); and Jefferies at No. 10 (USD 19.18bn, up by 79.4% YoY).

Slipping to 15 from the top spot in the Canadian deal value ranking was JPMorgan; other fallers from the top 10 included Bank of America (to 12 from three) and Wells Fargo (to 20 from six).

Across Americas deal count, Goldman Sachs (173) pipped JPMorgan (157) to the post, though the latter had the consolation of climbing from third last year. Houlihan Lokey slipped to the bronze medal position with 141 deals, 13 lower than 1H24. Citi and Lincoln International joined the top 10.

Citi has acted buyside on Charter Communications’ USD 36bn recommended offer for cable and broadband player Cox Communications as well as Johnson & Johnson’s USD 15.4bn takeover of novel drug developer Intra-Cellular Therapies.

Asia Pacific winners

Although US bulge brackets Goldman Sachs (USD 102.4bn, up by 241.9% YoY) and JPMorgan (USD 80.5bn, up by 231.5% YoY) topped the Asia Pacific (excluding Japan) deal value rankings, China’s CITIC Securities took the No.3 position with a haul of USD 40.2bn, up by 156.9% YoY.

It’s tough to overlook Rothschild & Co.’s astonishing climb to fourth from 53 last year, with its USD 37.5bn aggregated deal values having risen nearly 24-fold.

Rothschild is well-positioned as a sellside advisor – alongside the ubiquitous Goldman Sachs – on Carlyle, Abu Dhabi National Oil Company, Abu Dhabi Development Holding, and XRG’s USD 24bn proposed takeover of Australian oil and gas E&P player Santos.

The deal also fully accounts for JB North’s eye-popping entry into the top 10, in at No.9 from 144 last year – the Santos deal is the advisor’s sole entry. XRG’s buyside advisor on the deal, which also dominates the Australasia rankings, is JPMorgan.

Nomura’s stunning rise in the global rankings is capped by its unsurprising No.1 spot in the Japanese deal value standings, with an aggregate USD 128.9bn, up nearly nine times versus 1H24. Morgan Stanley slipped to second position despite more than tripling its deal values to USD 92.4bn.

In China, regional players CITIC Securities (No.3), CICC (No.4), Huatai Securities (No.6), Gram Capital (No.7), China Securities (No.8), Hongta Securities (No.9) and Postal Savings Bank of China (No.10) gave a strong showing in the top 10.

Moving to India, ICICI Securities stormed to the top spot from 61 in 1H24, boosted by its sellside role in Torrent Pharma’s pursuit of JB Chemicals & Pharmaceuticals.

PwC retained its No.1 position across both deal value and count in South Korea – a major contributor to its summit position across the APAC deal count. Landmark deals for the firm include advising the buyside on the Temasek-led, USD 1.5bn buyout of Haldiram Snack Food.

Buyout barons

With sponsor buyouts surging by 35% YoY to USD 359bn in 1H25 alongside a 7% YoY decline in deal count, it is notable how performance outstripped the wider deals market.

Consequently, the top three buyout advisors globally scored impressive deal value growth, with JPMorgan (USD 119.8bn, up by 102.3% YoY) leading the pack and topping the deal count chart. Goldman Sachs (USD 110.4bn, up by 44.2% YoY) and Citi (USD 50.8bn, up by 45.6% YoY) took silver and bronze in the global deal value category.

PwC and Goldman came second and third in the deal count stakes.

Exit emperors

Notwithstanding the number of paused situations after April’s volatility spike, 1H25’s overall private equity exit haul will have brought cheer to sore LPs, with deal values climbing by 45% YoY to USD 279bn – albeit from a deal count haul some 7% lower.

As mentioned earlier, Goldman Sachs topped the global exits ranking, with Morgan Stanley in second place. Among the exits by deal count, Houlihan Lokey ruled the roost – maintaining its top spot versus 1H24 – with a haul of 45 deals. Even on this score, Goldman Sachs remained hungry, climbing to third (31 deals) and nipping at the heels of second-placed Jefferies (33 deals).

A service of

Your M&A Future. Today

Explore unlimited content like this, available only in the platform.

Already a client? Sign in