Goldman Sachs, JPMorgan lead 1Q26 M&A rankings amid relentless hunt for scale

- Goldman Sachs, JPMorgan, Morgan Stanley stay on podium, but volumes slip

- Evercore storms into global top five with 56% increase in volume to USD 137.6bn

- PwC shares deal count crown with Goldman Sachs, but top 10 all see falls

Amid the peaks and troughs of rollercoaster drama, 1Q26 is perhaps best seen as a quarter of continuity. In many ways it was a microcosm of FY25, with an astonishing haul of megadeals, the flight to scale only accelerating, and geopolitical risks running alongside AI fallout in setting the stage for capital flows.

M&A volume of USD 1.38tn in 1Q26, up 20% year-on-year (YoY), incorporated some 20 megadeals of more than USD 10bn, worth a combined USD 508bn. Even the Iran conflict has not arrested momentum among larger deals. A mammoth USD 122bn capital raise from OpenAI closed on the last day of the quarter, just as McCormick & Co. unveiled its proposed USD 42.7bn takeover of Unilever’s food business.

Accompanying their multinational and large cap clients’ ambitions to scale has seen leading financial advisors accumulate astonishing deal hauls.

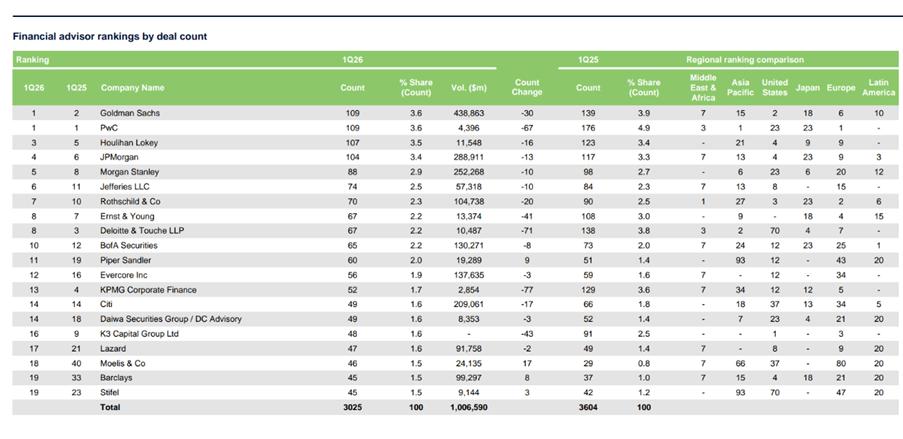

Just as in 1Q25 – and indeed FY25 – Goldman Sachs, JPMorgan, and Morgan Stanley have taken the podium positions. Only these houses achieved volume of at least USD 250bn apiece. Though it is worth noting all three saw slips in volume YoY, reflecting greater competition for mandates in an active market.

In first position, Goldman Sachs achieved USD 438.9bn in volume, down 2.4% YoY, but boasts roles on 12 of those 20 megadeals. It also achieved the double, taking the joint deal count crown with PwC at 109 apiece. Goldman’s volume market share of 43.6% was a shade lower than the 44.5% it recorded last year. Just over 60% of its deals were on the sellside, though this includes both active sale assistance and defence. Goldman Sachs will be delighted to see its sellside advice on the aforementioned Unilever foods deal come good; it will be less pleased if Andrea Orcel’s UniCredit succeeds in its USD 29.5bn pursuit of Commerzbank.

JPMorgan retained its second place with volume of USD 288.9bn despite a slide of 11.4% YoY. Working on eight megadeals, market share slipped to 28.7% from 32.3% in 1Q25. Some 64.4% of its mandates were sellside and the bank kicked off March in style as lead financial advisor to US energy utility player AES in its pending USD 38.4bn takeover by Global Infrastructure Partners.

Taking the bronze, Morgan Stanley secured roles on five megadeals and clocked up total volume of USD 252.3bn, down 2.6% YoY. Landing a sellside role alongside Goldman Sachs on that Unilever deal will have sweetened the close of the quarter no end.

Evercore – with USD 137.6bn, up 56% YoY – stormed into the top 10 by volume, taking fifth position, accumulating four megadeal mandates – including the plum role of lead financial advisor to US-based Jetro Restaurant Depot in its USD 29.1bn takeover by food products player Sysco Corp. UBS exited the top 10, (now ranked at 12, with volume of USD 71.9bn, down 28.4% YoY).

Though 1Q26 volume is the second highest start to a year on record – bested only by 1Q21 – deal count remains under scrutiny. Reconciliation of deal count data can last well beyond the reported period, but a flash reading looks a little soft.

Just as the flight to scale is easiest pursued by larger multinationals, so any chill winds tend to affect the mid-market hardest. Sponsor exits from technology assets bought in the heady 2020-2022 period have been particularly tricky amid the “SaaSpocalypse” unleashed by Anthropic’s release of Claude Cowork plugins in January 2026.

In this context, it is perhaps unsurprising to see that the top 10 financial advisors by deal count all saw their hauls fall versus 1Q25, with joint gold medallists Goldman Sachs and PwC down 21.6% and 38%, respectively, with 109 mandates apiece. Houlihan Lokey climbed into the bronze position from fifth last year, racking up 107 deals, down 13% YoY.

Instability continues to coerce the chase for scale in a market desperate to be proactive rather than waiting for conditions to limit optionality. But this sentiment could certainly be challenged if the Iran conflict extends into a major bout of stagflation. The pathways from today remain varied and outlook is obscured.

But if this quarter’s financial advisor rankings prove anything, it is that financial advisors are meeting their clients’ ambitions to execute bigger deals in the pursuit of resilience and scale.

Europe

- Goldman Sachs retained the top spot, with volume of USD 191.9bn.

- JPMorgan climbed one place to take silver, with volume of USD 140.4bn.

- PwC led by deal count, though its haul of 67 was down by 40% versus 1Q265

- In the UK, Goldman Sachs retained its top position with volume of USD 94.4bn across 19 deals.

- Likewise, Goldman Sachs retained the DACH crown with USD 61.9bn across nine deals.

Americas

- The crown stayed with Goldman Sachs, with a haul of USD 322.8bn. And Goldman Sachs also led in deal count, with 87 deals. JP Morgan retained its silver with USD 205.6bn across 79 deals.

- Houlihan Lokey lost its deal count gold and took silver with 83 deals.

- This was replicated in US rankings, with Goldman Sachs at USD 313.8bn across 83 deals and JP Morgan with USD 194.5bn across 71 deals.

- In Canada, RBC Capital Markets crossed the line first with USD 17.4bn across five deals.

APAC

- In APAC excl. Japan, Goldman Sachs retained its No.1 spot by volume, with USD 45.6bn across 12 deals.

- BofA Securities climbed 16 places to secure the silver position, with USD 34.8bn across 10 deals, while JPMorgan rose one spot to claim bronze with USD 24.8bn from 14 deals

- Rothschild vaulted from 12th place to 4th, posting USD 24.1bn, while BNP Paribas (USD 23.3bn) took fifth position.

- On the APAC excl. Japan deal count score, PwC retained its crown with 39 deals, down by 18 from 1Q25.

- In Japan, Morgan Stanley took first place by volume, with USD 19.8bn across 21 deals. Nomura took the silver in volume and gold in deal count with USD 15.6bn across 33 deals.

- In South Korea, Citi took the volume crown with a single high value deal of USD 1.6bn, on the count front PwC led the race with 19 deals.

- In India, JPMorgan took the volume top spot at USD 2.4bn across two deals, EY took the silver in volumes and led the deal count race with USD 1.8bn across 11 deals.

- In Australasia, Goldman Sachs won the day across volume (USD 22.2bn), PwC grabbed the top spot in deal count front with 11 deals.

Financial sponsors buyouts

- Goldman Sachs took the global volume crown, with USD 73.1bn across 10 deals.

- Top performer by deal count was Houlihan Lokey, with USD 1.3bn across 14 deals

Financial sponsors exits

- Evercore jumped two spots to score the highest on volume, with USD 47.2bn across 13 deals.

- Robert W Baird surged five spots to take the deal count gold, with USD 9.7bn across 22 deals.

A service of

Your M&A Future. Today

Explore unlimited content like this, available only in the platform.

Already a client? Sign in