Data centers’ thirst for power will drive M&A in US renewables despite White House pushback

- Renewables are well positioned to help satisfy AI-driven energy demand

- Market offers attractive opportunities for ‘smart money’

- Non-traditional buyers such as Alphabet’s Google entering the space

Newton’s third law of motion states that for every action, there is an equal and opposite reaction.

In the US, the reaction to President Donald Trump’s championing for supremacy in artificial intelligence (AI) has been a frantic scramble for power sources – including clean energy, which Trump has described as “the scam of the century” – to fuel the data centers that train and run AI.

While M&A deals in the US renewable sector have steadily declined since 2021, the growing realization that power resilience requires investing in all energy sources, coupled with the need for rapid power dispatch, may increase dealmaking in the renewable space this year.

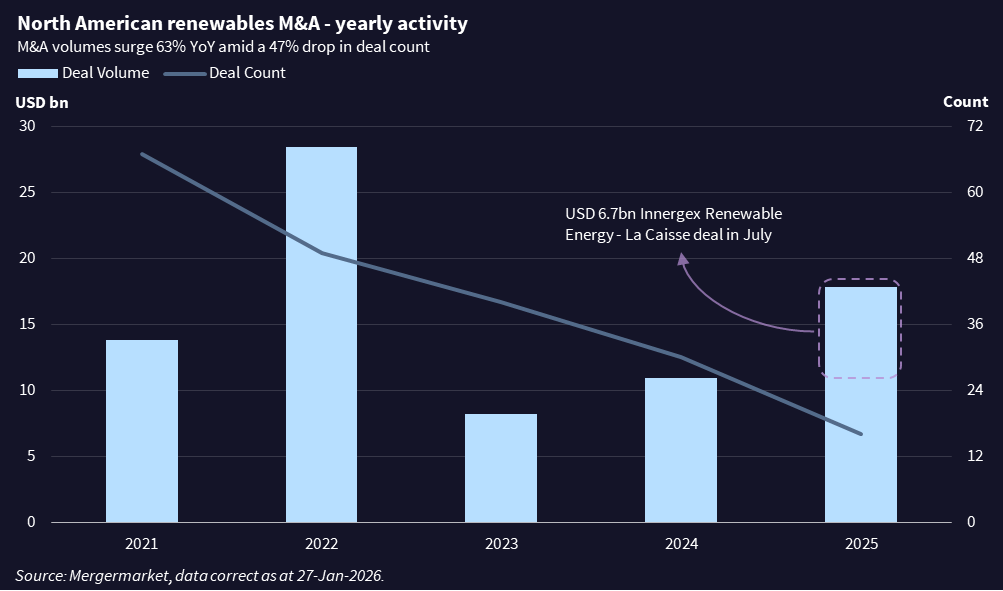

There were 16 renewable M&A deals in the US in 2025, compared with 30 in 2024, according to Mergermarket data. However, five of the 16 deals last year were valued at USD 1bn or more showing continued investors’ interest in the sector.

In fact, renewable deal volume increased 63%, from USD 10.9bn in 2024 to USD 17.7bn in 2025 driven by La Caisse’s USD 6.7bn acquisition of Innergex Renewable Energy in July. The second largest deal of the year was Alphabet’s pending acquisition of Intersect Power for USD 4.75bn – which would make it the only tech giant to own a power company.

What will power M&A in 2026?

AI-intensive data centers’ insatiable demand for electricity will provide the renewable sector the tailwind it needs, sector executives and M&A advisors said.

Securing access to reliable electricity is the primary concern for data center developers and hyperscalers, making grid infrastructure and new generation capacity the most critical bottlenecks, said Axel Thiemann, CEO of renewable energy company Sonnedix. It seems difficult to satisfy this demand for power without a significant deployment of renewable energy, notwithstanding the current regulatory and political rhetoric surrounding the industry, he added.

Trump’s One Big Beautiful Bill sunset federal tax credits for renewable projects.

Installing solar and wind farms or battery energy storage systems can take months, compared to up to three years for combined cycle natural gas-fired plants, according to Trenton Allen, CEO of Sustainable Capital Advisors, a consulting and financial advisory firm that specializes in sustainable infrastructure and climate-focused finance.

Just over 88% of the new power generation capacity put in service in the US from January to November 2025 was renewable energy, with the bulk of it being solar, according to government data. Natural gas, coal and oil represented less than 1% of the new power generation capacity.

In November, Alphabet’s Google announced it will invest USD 40bn in Texas to build new cloud and AI infrastructure, including new data center campuses. Google is also bringing new energy to the grid through a new USD 30m Energy Impact Fund that will scale and accelerate energy initiatives, along with more than 6,200 megawatts of new energy generation capacity contracted. One of the new data centers will be built alongside a new solar and battery storage plant, according to a company blog post.

Who will fuel the sector?

The renewable sector continues to offer investment opportunities but fewer than in the past, attracting sector specialists and long-term investors, the experts said.

The market is more suitable for institutional investors focused on infrastructure and interested in long term projects with 10 to 15 years investment horizons, Trenton said.

This news service reported last September that general partners are becoming more rigorous in their assessment of opportunities, prioritizing late-stage projects and niche subsectors.

Investing in renewable energy in 2026 requires a deep understanding of the dynamics at play and a willingness to be creative and take risks when the opportunities arise, said Chris Zentz, partner at Akerman’s corporate practice group. Even with some of the added difficulties the industry is currently experiencing, the “smart money” has shown that excellent opportunities still exist and that the renewable industry is not going away, he added.

“We have started to see non-traditional buyers [like data center operators] acquiring stakes in energy assets or invest in early-stage tech,” said Marcus Wolter, partner and director of the corporate practice at Caldwell. He added that he is seeing renewable energy assets in the US attracting the interest of Asian investors.

Many of the biggest players in the data center space are going to try to emulate Google’s pending acquisition of Intersect as they realize it is better to take control of the entire development cycle of their energy supply, Zentz said. Effectively, transactions like these cut out the middle-man function of utilities by giving the load customer control over a significant part of the energy supply equation – the location, speed, and size of generation development, he added.

Fault lines in the grid

Government policies could still derail the sector. The federal government could try to restrict even more the tax credits available for renewable energy projects under the Inflation Reduction Act. It could also continue to curb ESG-oriented investment. And not overhauling state and federal permitting could also be detrimental to sector, Wolter said.

The rise in private purchase agreements is a trend worth watching. As private offtakes – such as data centers – account for a growing share of demand, it becomes increasingly critical to evaluate how financially resilient and creditworthy these buyers are. Investors and developers need to be more careful if they are not selling power to a traditional utility. If too many private offtakers were to pull back, for example, if the much-discussed AI bubble were to burst, it could pose a systemic risk. That is why diversification and thorough due diligence will be crucial for investors, Wolter added.

A service of

Your M&A Future. Today

Explore unlimited content like this, available only in the platform.

Already a client? Sign in