Data center buildout booms, but M&A activity lags – Dealspeak North America

- Skyrocketing valuations keep owners from selling prized assets

- Greenfield investments surge, tripling last year’s capital flows

- Debt financing dwarfs M&A amid hyperscaler expansion plans

The boom in artificial intelligence (AI) has triggered a wave of data center investments. Yet transformative M&A activity remains largely on hold, as owners keep their assets longer amid skyrocketing valuations, advisors say.

Rather than buyouts, more capital is pouring into new, ground-up construction as the great AI-fueled data center buildout gathers pace.

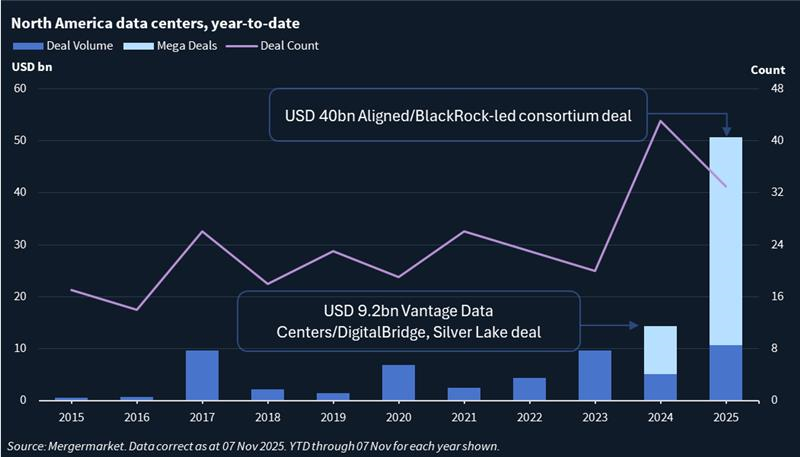

So far this year, 33 M&A deals for North American data center companies worth USD 50.7bn have taken place. That compares with 43 deals worth USD 14.3bn for the same period last year, Mergermarket data shows.

Exclude the USD 40bn buyout of Aligned Data Centers by BlackRock’s Global Infrastructure Partners, MGX, Microsoft and NVIDIA – announced 15 October – then M&A in North America’s data center space in 2025 is down from last year, even if levels remain elevated historically.

Greenfield capital floods in

Much of the datacenter buildout is driven by private capital – with private equity or infrastructure funds investing into the sector, said Fritz Lark, an infrastructure lawyer at Baker Botts.

Meta last month struck a joint venture deal with private credit firm Blue Owl to raise USD 27bn to develop a data center in Louisiana, highlighting the need to access all forms of capital.

Deals like that mean financing for various data center projects dwarfs M&A spend substantially.

Total debt issued for North American data center transactions – which includes new construction projects as well as M&A – reached USD 115bn across 66 deals for the year-to-date, the highest level on record, Infralogic data shows. That compares with USD 73.6bn of debt across 63 deals for the whole of 2024.

For new construction projects alone – also known as greenfield investments – the upswing is even more dramatic: the year-to-date total of USD 89.6bn is more than triple the whole of last year, according to Infralogic.

Why M&A is hard

Why the relative lack of data center M&A?

Financial sponsors, the main buyers of data center assets, have a thesis on AI and its importance. Right now, they want to increase their exposure to the sector, not sell, advisors say.

Sky-high valuations are another sticking point, noted Sean McDevitt, a partner at management consulting firm Arthur D. Little, which provided commercial due diligence advice to Meta on the Blue Owl deal. Data centers are projected to need trillions in capital to keep pace with the demand for computing power in the next five years, driving up valuations.

For buyers, the challenge is twofold: First, they must pay a lot of dollars to buy control, and then they must fund further growth to justify the lofty valuation, one digital infrastructure banker said.

Few buyers have the balance sheet or data center exposure to justify such large transactions.

The sheer volume of capital flooding the sector is creating suddenly large platforms, this banker said. Blackstone-owned QTS, EQT Infrastructure-owned EdgeConneX, KKR’s CyrusOne, and DigitalBridge’s Switch dominate the landscape, leaving limited room for new entrants.

“Once valuations temper down, you might see more combinations,” the banker said. “It’s kind of weird – the sector is hot, but there’s not much M&A”.

Exit options are another concern. Because many PE firms are already in one or two large data center platforms, one of the biggest questions is what their exit looks like, said an investor in infrastructure projects. Continuation vehicles may become more common as sponsors seek liquidity, the investor said.

Hyperscalers as buyers?

Sponsors like MGX, which is backed by Abu Dhabi and is an investor in OpenAI, Databricks and X.AI, could continue to acquire more data center companies, a second digital infrastructure banker said.

The bigger question revolves around the hyperscalers. Microsoft plans to double its total data center footprint over the next two years, CEO Satya Nadella told investors last month.

While such tech giants have historically built their own data center facilities, Microsoft’s participation in the Aligned deal suggests hyperscalers could emerge as buyers too. They’re also the ones with the cash, the investor added.

Energy and the long view

Data center demand is also propping up dealmaking in the energy sector.

Data centers are projected to require 22% more grid power by year-end and nearly triple in 2030, according to S&P Global’s 451 Research.

With utilities slow to respond, data center operators are striking partnerships to secure their own generation capacity, Lark said.

Microsoft’s deal with Crane Clean Energy Center and Amazon’s deal with Talen Energy illustrate this trend. In other examples, Brookfield announced a USD 5bn partnership with Bloom Energy in October, and Oracle teamed with Volta Grid to power its AI workloads.

“It’s a race to get access to power and lock it up,” the second banker noted.

Questions remain about how long the AI arms race will last and how hyperscalers will demonstrate returns to satisfy investors.

Some voice caution against overbuilding, too. If there’s a glut of data centers and AI adoption falls short, no one would know for five or six years because that is how long it takes for data center capacity to come online, Baker Botts’ Lark said.

For now, the sector remains a magnet for capital, even if transformative M&A is on hold. “It’s going to be one-off deals here and there,” the investor said. “We won’t see a constant M&A environment given how big some of these platforms have become.”

A service of

Your M&A Future. Today

Explore unlimited content like this, available only in the platform.

Already a client? Sign in