Consumer Trendspotter 1H23: Cava IPO shines in second year of record-low deals

- Strategics with cash continue to scoop up competitors

- Restaurants, luxury brands resilient in face of uncertainty

As investors confront the back half of a second year of slow deal-making, they do so with a bit more experience under their belts.

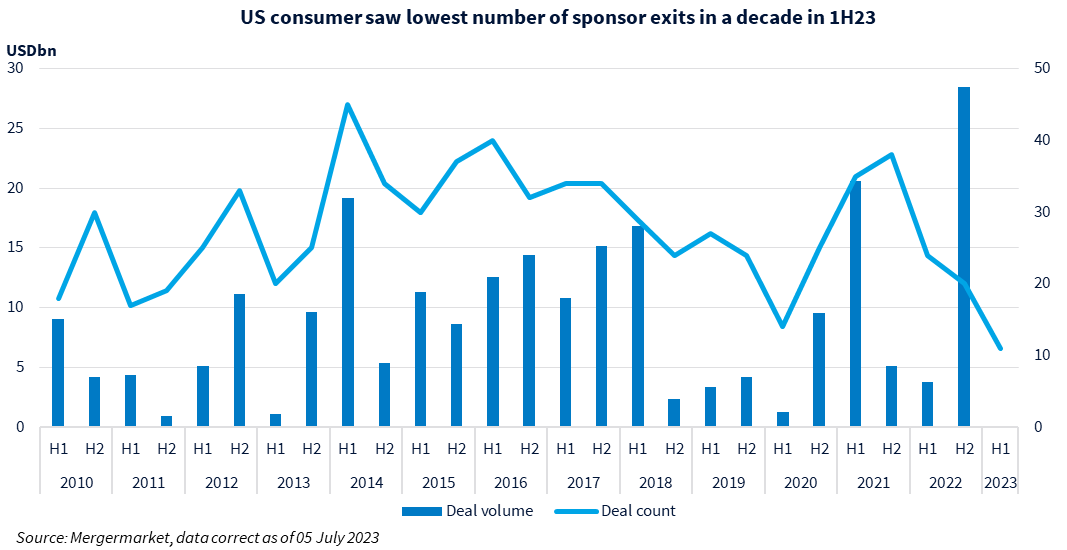

According to Mergermarket data, the consumer sector again saw the lowest number of US financial sponsor exits in a decade, with 1H23 registering just 11.

Similarly, deal value in 1H this year was down 5% compared to the first half of last year, notching USD 20.2bn. Many deals continue to fall apart due to discrepancies in valuation expectations, sources say.

However, with the 52-week highs from last year dropping off, management teams may soon ease their stubbornness on price and look for creative ways to strike deals, sources say.

“It has been a slow M&A market for two years running, but we're seeing increased activity,” said Kelly Hardy, M&A partner and global head of consumer at law firm Hogan Lovells. “We're seeing more strength in the middle market, and that makes sense thinking about PE funds with dry powder, strategics with some cash, and the economic stresses of the last several years.”

So far this year, in the consumer sector, restaurant chains have emerged as good swimmers in choppy waters, making bullish bets. Cava Group [NYSE:CAVA] pioneered 2023’s first major market test of a standalone brand going public, and it benefited from parched investors thirsty for fresh growth.

In June, Cava priced its IPO at USD 22 per share – three dollars above the top end of its initial USD 17 to USD 19 range – to raise almost USD 318m at a USD 2.45bn valuation.

Cava may have paved the way for more restaurants to test the IPO market this year or early next year, as Brazilian steakhouse owner Fogo Hospitality, Korean barbecue chain Gen Restaurant Group and Panera Bread have all signaled their desire to go public.

This year, restaurant strategics also continue to eat up competitors, as seen in Darden Restaurants’ [NYSE:DRI] May acquisition of Ruth's Chris [NASDAQ: RUTH] for USD 21.50 per share, or an equity value of USD 715m.

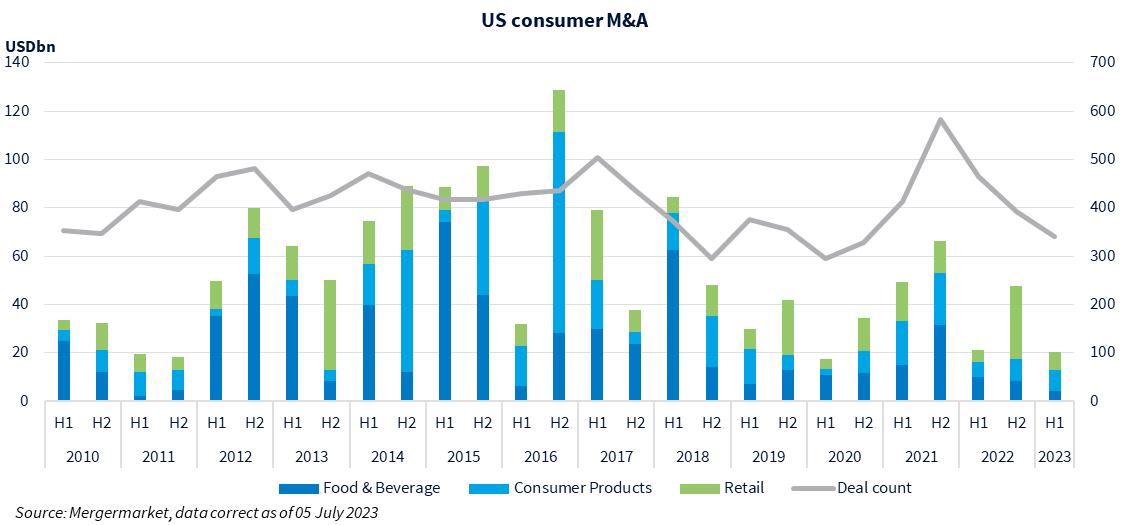

CPG (consumer packaged goods) strategics, on the other hand, are more keen to review their portfolios for divestitures, offering acquisition opportunities for smaller players.

The largest deals of the year so far point directly to those trends, as food manufacturing giant The J.M. Smucker Co. [NYSE:SJM] off-loaded its Rachael Ray Nutrish and other pet food brands for USD 1.2bn to the smaller Post Holdings [NYSE:POST] in February. In May, Tempur Sealy International [NYSE:TPX] scooped up Mattress Firm Group from Steinhoff International in a cash and stock transaction of around USD 4bn.

Also in May, Mexico-based Fomento Económico agreed to divest its minority interest in New York-based foodservice supplier JetroRestaurant Depot for USD 1.4bn in cash.

“2023 is the year of the divests,” said Eric Roth, managing director for the consumer group at PE firm MidOcean Partners. Roth also expects take-private opportunities in the public markets to be major sources of M&A activity this year.

Some activity will also be driven by distress in the retail space. The bankruptcy of Bed, Bath & Beyond and the subsequent failed sale attempt of its Buy Buy Baby stores are prime examples. Other quiet segments include fashion, beauty, and beverage.

However, signs of “cautious optimism” can be seen in recent deals, such as Mars’ agreement to acquire Kevin’s Natural Foods announced in early July; and the reported sale effort for uniform and apparel manufacturer Augusta Sportswear, owned by PE firm Kelso & Co.

More healthy deal-making is expected in 4Q this year or 1Q next year as many sale processes that were pulled or paused in 2022 due to valuation disagreements are expected to come back to market – including Bain Capital’s luxury Dutch stroller brand Bugaboo, according to a Mergermarket report.

High-quality and cash-positive assets are scarce and can afford to bide their time until frothier markets return, sources say.

Meanwhile, as luxury brands remain resilient in the face of macro market pressures, they continue to ride a wave of growth and performance. Expect more ultra-luxury assets to make a splash in an otherwise shallow pool of dealmaking.

A service of

Your M&A Future. Today

Explore unlimited content like this, available only in the platform.

Already a client? Sign in