Circle’s blockbuster IPO marks a watershed moment for stablecoins — ECM Pulse North America

- Stablecoins emerge as ‘global financial building block’ for real-world use cases

- Regulatory clarity needed for broader adoption, pending legislation adds momentum

- Institutional investors take notice, leading to financial boardroom reevaluations

Circle’s soaring public debut is shaping up to be more than just another crypto headline. It’s becoming a catalyst for a structural shift in how investors, regulators, and corporations engage with digital assets.

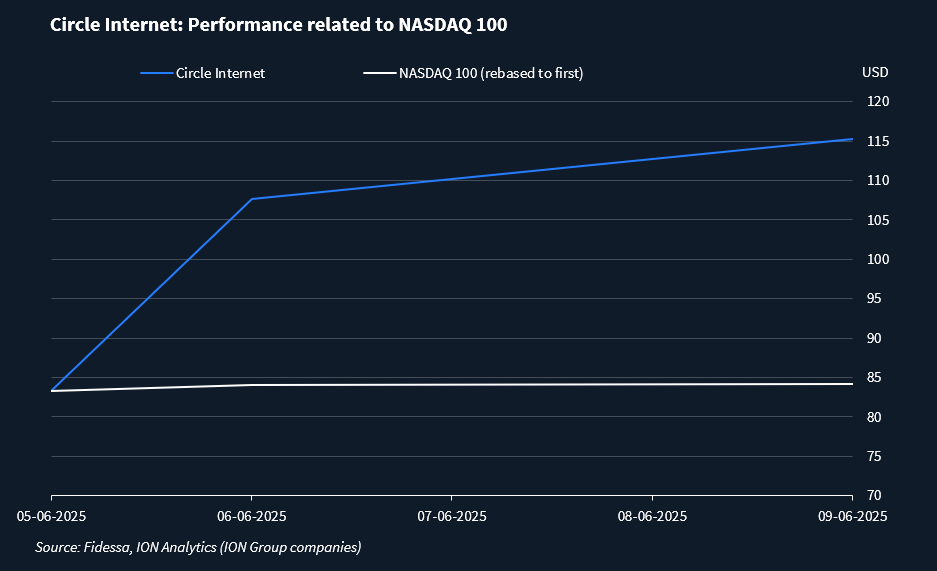

The stablecoin issuer’s stock surged in its first three trading days, opening at USD 115 on Tuesday – a 270% gain from its USD 31 IPO price. The rally, which began with a 200% intraday spike on last Thursday’s debut, has drawn attention from both institutional desks and retail momentum traders.

“This IPO came with a more reasonable starting point than Circle’s previous SPAC attempt,” said an ECM banker tracking the deal. “And that’s clearly been well-received.”

Unlike earlier crypto-linked IPOs that leaned on narrative over fundamentals, Circle’s pitch to the public markets is rooted in utility. Its dollar-pegged stablecoin, the USDC, is used in payments, remittances, and financial infrastructure.

With the Trump administration signaling support for a crypto-friendly regulatory framework and stablecoin-specific bills advancing in Congress, Circle’s role as a regulated, US-based stablecoin issuer resonates with investors looking for a de-risked bet in a sector still viewed with caution.

“Circle’s business is way less volatile than others in the space,” said one IPO investor. “It’s the most de-risked segment we’re reviewing.”

Real world use cases

For years, stablecoins were dismissed as shadow banking tools or speculative liquidity instruments. But the narrative is shifting. Several fintech incumbents – including PayPal, Visa and Stripe – are experimenting with stablecoin rails and programmable wallets. Stripe’s USD 1bn acquisition of Bridge, a stablecoin-native payments platform, underscores the sector’s growing relevance.

Bridge co-founder Zach Abrams described stablecoins as a “global financial building block” at a recent conference in San Francisco.

“Before, everything was very localized,” he said. “Now, we’re able to ship one card, one program, and serve users in dozens of countries. That’s a massive change in financial infrastructure.”

Bridge’s stablecoin-based payment rails already support real-world use cases — from SpaceX moving Starlink payments globally, to Scale AI paying data labelers in emerging markets, and US government foreign aid disbursements.

The next leap, according to Abrams, is the programmability of stablecoins, allowing businesses to send data with payments, streamlining everything from telecom roaming to insurance reconciliation. “Stablecoins aren’t just faster money,” he said. “They’re smarter money.”

While some worry about stablecoins cannibalizing existing networks, Abrams sees them as additive. “Cards stole share from what came before. Stablecoins will do the same, but the pie is growing. We’re not replacing, we’re expanding.”

That expansion is catching the eye of traditional players. “Stripe entering this space has sent a powerful signal,” one venture capitalist said. “Now everyone’s paying attention.”

Bridge’s exponential growth has outpaced Stripe’s this year, one sector advisor noted.

In a discussion about stablecoins at last week’s Money 20/20 conference in Amsterdam, Stripe CTO Rahul Patil said that in the future, “moving money will be as simple as sending text messages around the world.”

Despite early operational hurdles like securing banking partners, Bridge found support from institutions such as JPMorgan. But broader adoption still hinges on one missing ingredient: clear regulation. “We’re seeing material change,” Abrams said. “What’s holding this back from going from 5% to 50% of the market is legislative clarity.”

Crypto IPO pipeline widens

The success of eToro’s IPO, which surged 30% in its May debut, has also helped drive investor appetite. The multi-asset trading platform’s strong financials and a dual focus on retail and crypto, including stablecoins, have drawn favorable analyst coverage and sustained investor interest.

More crypto-themed IPOs may follow.

A day after Circle’s debut, Gemini, founded by Cameron and Tyler Winklevoss, confirmed it confidentially filed IPO paperwork with the SEC. The venture capitalist estimates Gemini could list in the second half of the year, pending regulatory approval and market conditions.

Kraken is also in talks with banks about a potential IPO, but hasn’t formalized mandates, co-CEO Arjun Sethi recently told this news service. He said the firm will proceed once there is clearer US regulation, with a bakeoff expected sometime after Congress recesses in August.

More potential crypto issuers are in the pipeline. “We’re working on a handful of other IPOs that are in various stages of readiness,” the sector advisor said, noting that a few are under SEC review and could list later this year “if things continue to go well.”

The IPO hopefuls include crypto exchanges, an asset manager, and a few service providers, he said. The ones that don’t go out this year will likely try in 2026, the sources agreed.

But many institutions remain cautious. “We’re largely staying on the sidelines,” said the ECM banker. “We’re still studying this space and hear the same from other banks.”

Regulatory challenges remain, especially around know your customer and anti-money laundering compliance and downstream user verification.

Lead Bank Chair and CEO Jacqueline Reses said financial institutions still lack the tools to properly manage risk, particularly for intraday money movement. Better tools for compliance, fraud detection, and liquidity management are needed, she said.

Still, proponents argue that stablecoins’ greatest strength may be their invisibility.

Many people might not even notice their future business dealings involve a stablecoin, said the sector advisor. The technology will be there, and “it’s going to suddenly be in all of these transactions and at a lower cost for everyone involved because it’s just peer-to-peer,” he said.

“Every financial service will have a wallet under the hood,” Abrams said. “Your Amazon account, your X account … you won’t even know it’s a wallet. The consumer doesn’t care.”

Rather than shouting disruption, programmable money will quietly embed itself into the plumbing of global commerce.

And thanks to Circle’s breakout, Wall Street is finally taking notice.

A service of

Your M&A Future. Today

Explore unlimited content like this, available only in the platform.

Already a client? Sign in