USS ready for next stage with mid-market, flexible plan

A combination of its willingness to do deals across a wide risk spectrum and limited competition from rival bidders could pave the way for a string of new investments by USS.

One of USS’ main strategies in recent years has been hunting opportunities to buy stakes in companies that it can then help to build and grow.

A prime example of this has been its purchase in 2020 of a small holding in Dukes Education, at the time a relatively small owner of private schools focused on the UK market.

Dukes has grown since USS’ stake purchase five years ago into a continental pan-European operator with bases in 15 countries.

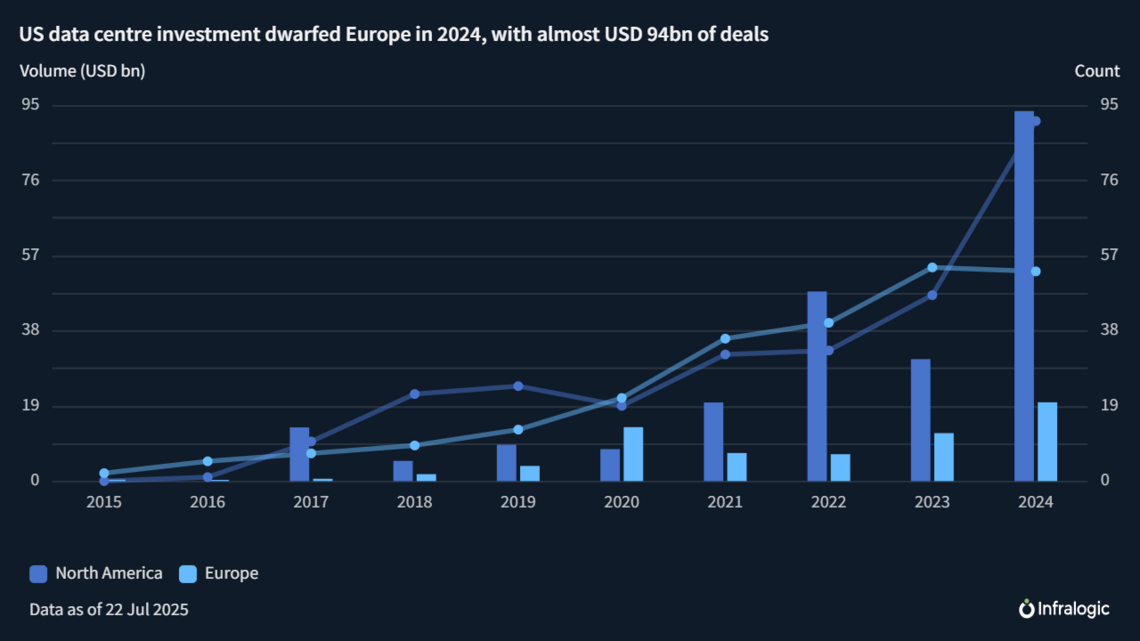

More recently, USS, which has been operating in infrastructure finance for some 15 years, has been taking its penchant for growing businesses – and for higher risk-adjusted returns – one step further by investing up to GBP 250m to be deployed over time into a pure greenfield data centre in northern England being developed by Blackstone-backed data centre operator QTS.

The scale of the deal is significant – once built the data centre will be the UK’s largest data centre and some of the largest data centres in Europe.

The rationale for the deal is clear, says Ben Levenstein, USS’ head of private markets at USS Investment Management Limited (USSIM). “Europe is years behind the US in data capacity. There’s going to be a long catch-up driven by AI and cloud computing.”

It has not always been plain sailing for USS’ digital deals – it has twice had to pump extra debt into its London-focused fibre company G.Network that it co-owns with Cube Infrastructure. Levenstein describes the UK fibre market as “difficult” and “ripe for consolidation”, with multiple alternative networks in need of scale and rationalisation.

Mid-market consolidation

Nonetheless, the Blackstone deal besides showing USS’ appetite for greenfield risk also shines a light on a key element of its current strategic thinking: of seeing itself as situated in the mid-market camp while at the same time allying with big managers.

“We focus more on mid-market than we have done previously but continue to look for opportunities to deploy capital in the large-cap space typically alongside lead investors, often where we have existing relationships across our Private Markets Group. In the mid-market our differentiator from many of our competitors is that we can support management teams to scale and grow their business, sustainably, over a longer-term horizon,” says Rob Horsnall, USSIM’s head of direct equity, which includes its infrastructure strategy.

Ultimately this means that – as exemplified by the Blackstone data centre deal – it is looking to deploy mid-market sized investments – of between GBP 100m and GBP 500m-plus – to complement investing in large cap companies or assets alongside “high quality” lead investors that can take controlling positions.

“Our strategy is to spend more of our time in the mid-market where we have a strong track record and have a differentiated approach,” says Horsnall.

This has echoes of moves by other institutional investors such as GIC, which has made a name for itself by coming in as a co-investor in large ticket deals.

Horsnall, who joined USS in 2010 and rose to his current role this year, does not just see greenfield opportunities through teaming up with large-cap investors, but also to work more closely with governments that are keen for private capital to support their growth agenda

“Government balance sheets are quite challenged so we expect they will need to crowd in private capital. It is an interesting opportunity,” says Horsnall.

USS has already run the rule over at least one mega greenfield opportunity in the government space, taking part in the initial phases of the bidding for greenfield Sizewell C nuclear project in eastern England. Although it has withdrawn from the auction process, its interest shines a light on its current focus on such higher return greenfield projects.

Opportunities elsewhere in the government space including in digital, decarbonisation, healthcare and defence sectors, says Horsnall, adding USS is also eyeing a big pivot to grids that “will be a big area of focus for us” over the next three to five years.

“We love offshore transmission assets which deliver inflation linked returns,” he says, citing USS’ interest in the planned UK onshore greenfield electricity grids dubbed competitively Appointed Transmission Owners (CATOs) and lower voltage distribution networks both in the UK and Europe. USS “would also look at interconnectors, with the right revenue model”, he adds.

The Blackstone deal – and also the Dukes deal – also show how far USS has travelled from its early days of pumping millions into so-called safe, steady utilities such as Thames Water and Heathrow Airport. “We have pivoted away from looking at large cap deals with like-minded investors with a large number of shareholders,” he says. “We still see opportunity in large utilities but focus on partnering with one high-quality lead investor.”

Risk appetite

It also shines a light on its flexibility when it comes to its choice of deals both in terms of risk and equity cheques.

“We can go from super core to opportunistic infrastructure, high single digit returns to 15%-plus returns,” says Horsnall. “This flexibility is an advantage, alongside working closely with colleagues in credit, private equity and property where we often work together on deals and asset management”.

In truth, core-plus and value-add seems to be its largely chosen terrain of late, given the Blackstone data centre partnership as well as its Dukes deal (which Horsnall describes as “historically on the cusp of private equity and infrastructure, but now firmly in infrastructure”) and also its purchase in 2020 alongside Astatine of a stake in Itasca, Illinois-headquartered PECO Pallet, which rents pallets to the foodservice, grocery and consumer products industries.

Horsnall says that “the core market in terms of pricing still has a little way to go before it becomes really attractive, but we believe that this will materialise overtime as new opportunities arise”. Having said that, USS did take early-stage interest in the 50% in PD Ports, a relatively core opportunity, being sold by Brookfield Infrastructure.

Aside from this flexibility over investments, Horsnall is optimistic on its potential pipeline. He sees less competition in the market as managers struggle to raise the same amounts of capital as they did before the interest rate hike, while USS as a pension fund can continue to deploy capital at pace.

“Over the medium term I see more supply of opportunities than there is currently dry powder in certain areas,” he remarks, adding that deals also remain challenging as the “bid-ask spread is a little bit wide”. The next “two to three years will likely be a very good time to invest capital”, he adds.

That said, USS has hardly been investing at a fast rate. While around 70% of USS’ private markets portfolio is held in direct or co-investments, the remainder is invested in a small number of large, generalist fund managers.

Ramping up investment

Horsnall’s team now plans to make a total of multiple billions of direct investments over the next three years, including over a billion a year.

But as the current market opens up opportunities to buy, it also throws up challenges – last year in what was a tough sellers’ market it failed to sell its stake in Moto, a decade after it bought into the UK motorway services area operator.

But while fund managers have to sell to comply with their fund cycles – or be forced to seek to manage the asset for another decade , or even raise further growth capital – USS is doubling down on Moto.

“Moto is a high quality business with a strong management team and a decarbonisation strategy in the UK,” says Horsnall, adding he is “super excited” by the fact that Moto will need the “equivalent power of a quarter of an average sized nuclear power station” to fuel its chargepoints over the next five years.

This is just the start, says Horsnall, as MSAs transform themselves from fuelling and food depots into providers of a swathe of new energy resources, from electricity for HGVs to solar and batteries and even biofuels.

National Air Traffic Systems is a not dissimilar story. An asset that USS bought a minority stake in 11 years ago alongside the UK government, the UK provider of air traffic control services has had its fair share of issues: two years ago its IT systems were unable to process flight plan data for a flight from Los Angeles to Paris, leading to flight delays and cancellations and a cost to consumers and airlines.

Although such risks seem inherent for owners of critical infrastructure, the incident has not put off Horsnall who, as with Moto, says USS has “no immediate plans” to sell its stake in NATS.

Indeed, he argues, the company is well placed to take advantage of the evolution of air travel and also drones over the next five to 10 years. Also, as the prospect of a third runway at Heathrow Airport looks more likely given government signals, NATS will likely play a key role in the “airspace design” for the new infrastructure, says Horsnall.

This buy and build strategy has reaped rewards in the past – its Spanish solar platform Bruc has grown from 100 MW of capacity when it bought a 50% stake in the company in 2021 years ago to over 2 GW today, and it has ambitions to reach 9 GW including batteries and flexible generation.

USS is clearly ramping up investing and pushing deeper into the value and greenfield opportunities. This is taking place against the backdrop of the current challenges faced by Thames Water, in which USS remains a shareholder. Horsnall declined to comment on this point, although the pension fund previously said it has “engaged extensively with Thames Water’s regulator [Ofwat] and management” but “that this effort has not borne fruit is a great disappointment and frustration to us all”.

Meanwhile USS’ ability to keep investing as GPs struggle to raise and deploy capital, and its inherent strategic flexibility, might stand it in good stead in the months ahead.

One area of less flexibility is geography. It hasn’t done a deal in Australia for years, and has no plans to do so now. While North America is still a key market, it’s proving a little “more challenging”. Ultimately, USS is a “long-term investor and will continue to allocate capital to the US as well as the UK and Europe”, says Horsnall.

Given the opportunity for deals like the Blackstone one, as well as fundraising challenges faced by GPs, there is clearly a gap in the market that USS is seeking to fill.

A service of

Shape your future with Infralogic. Today

Explore unlimited content like this, available only in the platform.

Already a client? Sign in