Sixth Street bets on Italy’s power sector with F2i JV

F2i has pulled off a long-awaited deal to add a renewables growth engine to its power utility Sorgenia. Sixth Street is investing in the enlarged business to tap opportunities in the Italian energy market – with downside protections in case of surprises. By Stefano Berra.

In 2022 a new idea started to take shape at F2i’s Milan headquarters. Italy’s largest infrastructure fund manager controlled a vast portfolio of energy assets worth an estimated EUR 10bn, ranging from gas distribution and storage to renewables, through separate funds. What if all those assets were pooled together to create an energy champion?

F2i hired investment banks to study this option, but Europe’s energy crisis following Russia’s invasion of Ukraine soon threw a spanner in the works. Gas and power prices shot up and European behemoths like Uniper went under. The market’s volatility made the merger seem less feasible, not least because it made it much harder to value the assets.

F2i tweaked its plans to adjust. The biggest asset, gas distributor 2i Rete Gas, was sold separately to its peer Italgas after a brief attempt to IPO. Gas storage operator Ital Gas Storage – unrelated to Milan-listed Italgas despite the similar name – was excluded from merger plans.

But the core of the idea survived. Three years later it led to a major deal to combine two key assets of F2i – utility Sorgenia and EF Solare, Italy’s largest solar power producer – into a single group worth EUR 4bn. Renovalia Tramontana, a smaller Spanish wind power unit of F2i, was also transferred to Sorgenia in the same transaction, signed at the beginning of August.

US investment firm Sixth Street agreed to buy a 38% stake in the combined business to set the valuation – investing an equity ticket of around EUR 800m, according to sources familiar with the deal.

This allowed F2i’s second infrastructure fund and Asterion Industrial Partners to exit Sorgenia, five years after taking over the business. F2i’s Fund V invested fresh capital to help buy them out, while Fund III rolled over its previous investment in EF Solare into the merged business, allowing F2i to continue to control the company with a combined 62% stake.

The price paid by Sixth Street was slightly below the initial EUR 1bn expectation for a stake of up to 40% in the business, when the deal was launched in its current form in May 2024, but this does not tell the whole story.

Complex multiples

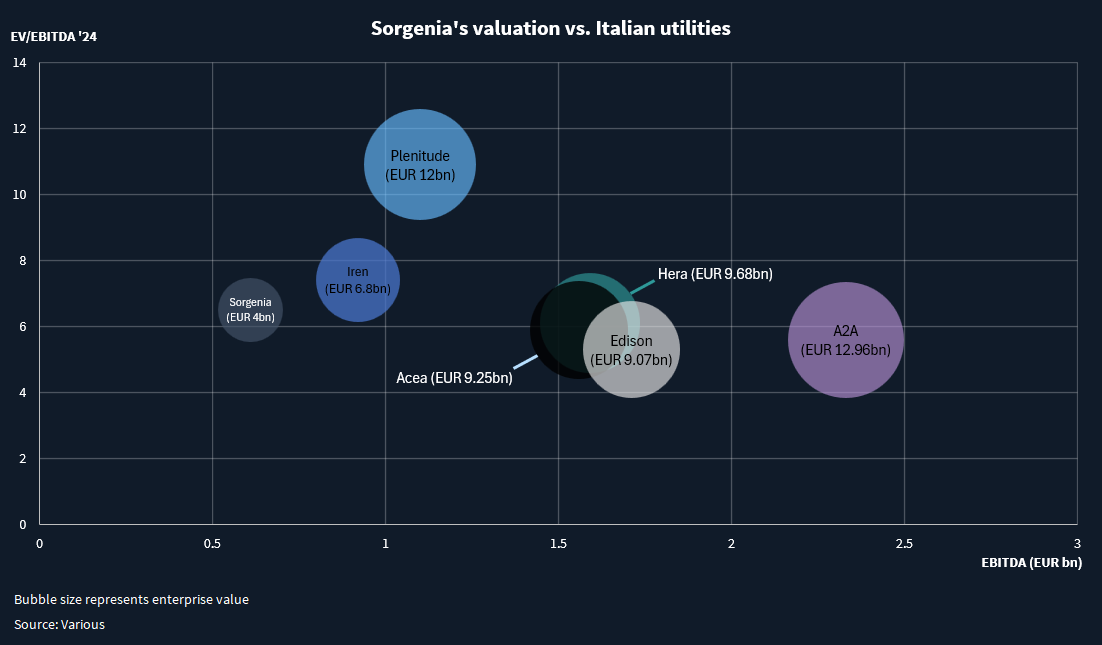

The deal values the combined business at a multiple of about 6.5x the EBITDA generated in 2024, according to sources familiar with the transaction. This is in fact a slight premium to many other Italian utilities, such as A2A, Edison, Hera and Acea, or even Enel, which all trade below 6x. (see Sorgenia’s valuation vs. Italian utilities chart)

The multiple based on 2025 EBITDA is actually higher, as the core earnings of old Sorgenia, excluding EF Solare and Renovalia, are expected to fall from EUR 302m last year to the mid-EUR 200m range this year, on the back of lower power prices, according to one source.

“Part of what’s in the valuation is [Sixth Street’s] belief in the growth of the business,” says another source.

From Sixth Street’s perspective it still looked like a bargain compared to Ares Management’s recent acquisition of a 20% stake in Eni’s renewables and retail arm, Plenitude, for a nearly 11x multiple, this source points out.

The transaction gave the pre-merger Sorgenia an enterprise value close to EUR 1.6bn, according to one source, not much above the EUR 1.4bn-1.5bn EV at the time of F2i’s and Asterion’s investment.

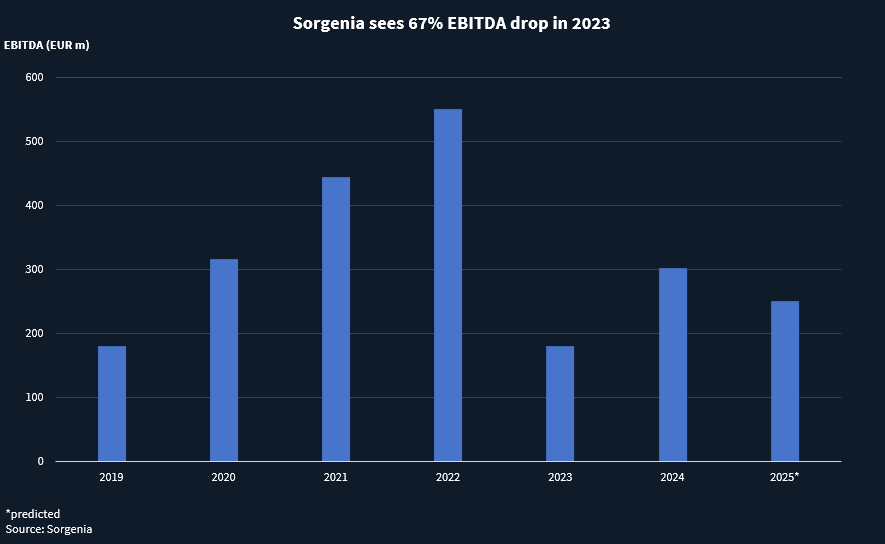

The unregulated business’ volatile earnings are partly to blame, with EBITDA tripling from EUR 180m in 2019 to EUR 550m in 2022, when energy prices shot up, only to plummet back to EUR 180m in 2023 when they fell back again. (see Sorgenia sees 67% EBITDA drop in 2023 chart)

Despite this, F2i’s Fund II and Asterion appear to have made a solid return on their investment thanks to other “value creation levers”, says one of the sources.

These levers include paying themselves nearly EUR 150m of dividends over the past years and taking advantage of the power price boom to cut down net debt by half to around EUR 350m, Sorgenia’s accounts show, which will allow them pocket a larger share of the sale price. Two debt refinancings totalling EUR 2.3bn agreed just before the sale to Sixth Street also improved the financial structure.

F2i, Sixth Street and Asterion declined to comment on valuations.

For F2i, the deal was complicated by the need to balance the interests of LPs across its different funds – with Fund II exiting, Fund III keeping a close eye on the valuation of EF Solare, which together with Renovalia represented around 60% of the overall enterprise value, and Fund V making a new investment.

A small army of advisors oversaw the deal, which “was negotiated down to the last comma”, according to one of them.

F2i’s main advisors were Lazard, Intesa Sanpaolo and Mediobanca, while Bank of America worked for Fund II, Nomura for Fund III and Societe Generale for Fund V. Rothschild worked with Sixth Street and JP Morgan with Asterion.

Growth path ahead

After the merger, Sorgenia will become “a key player in the energy transition and a potential platform for industrial aggregation”, said Renato Ravanelli, CEO of F2i, in the 4 August statement on the deal’s signing.

Following the deal the company will own one of the largest operating renewables portfolios in Europe with 1.7 GW of solar, wind, biomass, and hydroelectric plants, plus 5 GW of renewables under development.

It will also keep its 4.4 GW fleet of combined cycle gas turbine (CCGT) plants, which F2i described as “strategic assets that ensure system stability during the energy transition”, and an electricity and gas retail business with more than one million customers.

Combining the businesses will let Sorgenia generate more stable, contracted cash flows from the renewables assets, while managing intermittency with its flexible gas-fired plants. It will also allow the company to benefit from economies of scale, more than doubling its EBITDA, and potentially expand its retail offering with more green power supply contracts.

F2i was keen to hold on to the business after Fund II’s maturity because of its prospects to grow further.

“If [F2i] had exited the whole investment, they would have been giving up a lot of upside because there’s a lot of growth that is about to happen in the energy sector,” says a source familiar with F2i’s plans. “The valuations of these businesses and the underlying EBITDA are only going to continue to grow.”

While Asterion is exiting, Credit Agricole Assurances remains as a minority shareholder in the EF Solare and Renovalia portfolios, but not in Sorgenia itself.

Sixth Street has indicated it shares F2i’s growth ambitions over the long term, with partner Richard Sberlati saying in the same 4 August statement that the firm is deploying “patient institutional capital” to facilitate this.

The San Francisco-headquartered manager is investing through its USD 30bn-plus evergreen TAO fund, as well as its closed-end Sixth Street Opportunities funds, according to a source familiar with the deal.

Sixth Street is also keeping an eye on downside protection, however, and according to multiple sources it is investing through preferred equity to shield itself from possible power market shocks.

This has become a regular fixture for US investors targeting the Italian energy market – with KKR recently investing in Eni’s petrol station business Enilive through preferred equity, and Ares investing in Plenitude with a similar instrument.

Nevertheless, Sixth Street is “not going to be excited” if they “hit just the pref returns” and are banking on Sorgenia’s growth, says one source familiar with the investor’s thinking.

Sixth Street’s love affair with the Italian energy market is not new after all, as the firm already invested in 2022 in Enipower, the captive power generation unit of oil group Eni, and the new deal signals it is still bullish.

Bet on power prices

As Sorgenia is an unregulated utility, the deal represents a bet on increasing power demand and power prices in Italy.

The investors believe “electricity demand in Italy and Spain is already starting to tick up and it’ll tick up a lot over the next number of years”, driven by increased electrification and new demand from the likes of EV charging and data centres, according to one of the sources familiar with their plans.

After years of ups and downs “we’re dealing with a much more stabilized market going forward, one in which we’re not going to see a big downtick in power prices going forward,” says the source.

Combining EF Solare’s renewables and Sorgenia’s conventional power fleet is also key to avoid being exposed to periods of low power prices at times of high renewable generation, “In today’s environment there is a lot of industrial logic to combine the businesses,” adds the source. Sorgenia’s own electricity retail business on the other hand offers a “natural hedge” to pass on higher generation costs.

Adding battery energy storage systems (BESS) will also help – the company has started developing battery projects at its CCGT sites and secured capacity market tariffs. BESS represents “a decent part” of Sorgenia’s 5 GW project pipeline, and the company is considering bidding in the upcoming MACSE auctions for more incentives, according to the source.

Growth paths in Spain, where the renewables market is more in the doldrums, are less certain. However, Sorgenia’s investors see the same macro trends that are playing out in Italy – rising power demand and prices in the mid-term that should be supportive, the source says.

What’s more, opportunities could emerge to buy on the cheap more individual solar plants that are struggling to cope with price volatility, adds the source.

“There’s going to be lot of unnatural holders of assets that have built merchant projects with ill-suited capital structures,” says the source. “So there’s probably a consolidation story that’s going to happen in Spain for the next couple of years.”

Either way, Italy is likely to remain the main engine for Sorgenia’s growth. Sixth Street is not the only international investor to have spotted opportunities in the Italian energy market, as KKR’s Enilive deal and Ares’ Plenitude investment show.

And with France’s EDF now considering selling its Italian power arm Edison – a business potentially twice the size of Sorgenia – an even larger opportunity for investors could soon present itself.

A service of

Shape your future with Infralogic. Today

Explore unlimited content like this, available only in the platform.

Already a client? Sign in