Open-ended funds’ appeal endures despite lull

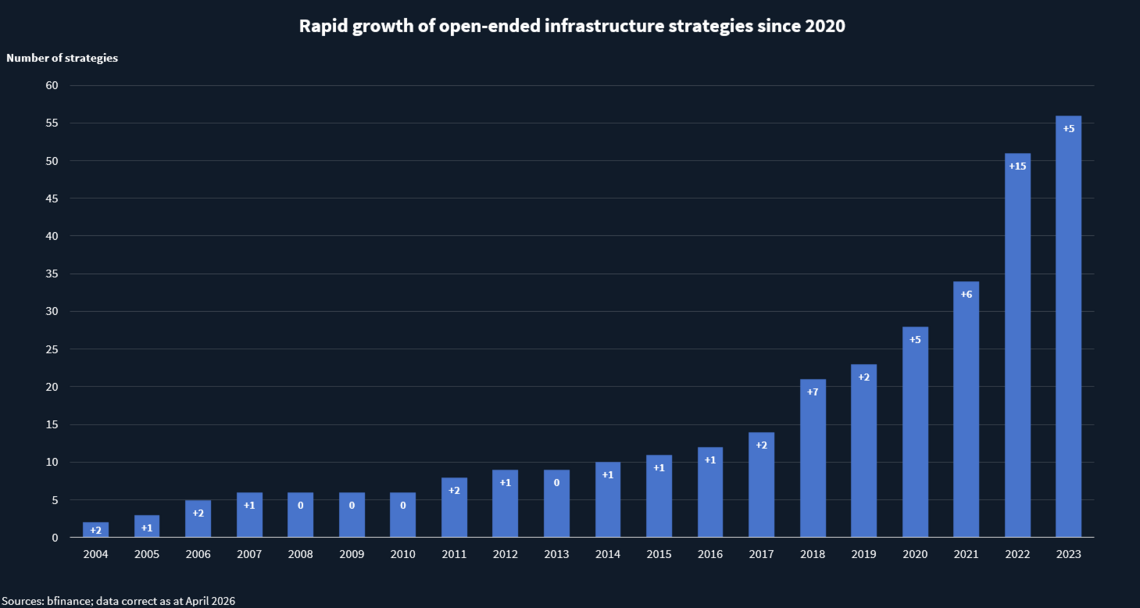

Open-ended infrastructure equity funds were all the rage in the early years of this decade, driven in part by low interest rates.

The success of the longstanding mega open-ended funds managed by the likes of IFM (which launched in 2004 and today has some USD 90bn of commitments) and JP Morgan also whetted appetites.

The need for “reinvestment, expansion and selective recycling of maturing sectors” such as digital infrastructure and the energy transition was also well suited to open ended funds, said Gordon Hay, who heads The Morrison & Co Infrastructure Partnership, an open–ended fund launched in 2021 by New Zealand-headquartered fund manager Morrison.

Octopus, KKR, Morrison, Octopus, Ardian and Macquarie were among no less than 31 infrastructure managers that launched open–ended equity infrastructure products between 2020 and 2023. Just 23 were started between 2002 and 2019.

Yet hardly any such funds have been launched since then. This is largely because many open-ended funds are focused on core investments that offer single digit returns, making them less attractive in the prevailing higher interest rate environment. EQT’s launch of its open–ended active core fund last year was one of the few to launch since 2023.

LPs see place for open ended funds

Yet an in-depth survey of limited partners’ attitudes to the infrastructure sector carried out by investment consultant bfinance and shared with Infralogic shows open ended funds have an important place in institutional investor portfolios.

They also anecdotally retain an important strategic place in infrastructure fund managers’ portfolios, and in some cases are generating healthy core-plus returns.

All this begs the question whether more open-ended strategies will come to market, particularly as interest rates start to level off. Open ended funds also particularly benefit from inflation linked protections. One challenge might be that fundraisings for some open-ended funds looks sluggish, potentially putting off fresh launches of such strategies.

Despite interest rates globally sitting well above early 2022 rates, LPs clearly regard open–ended funds as an important part of their fund investment mix.

Some 83% of limited partners said they can “consider” investing in both open–ended infrastructure equity funds as well as closed–ended ones, according to the survey of 40 global LPs carried out by bfinance.

Very few – just 6% – of the LPs surveyed said they would only target open–ended funds. But just 11% said would only have closed ended funds in their portfolios.

Serving specific roles

Open-ended funds also serve specific roles, LP respondents said. They “work well when you’re building exposure” to the sector, said one unnamed Australian superannuation fund for the survey, a reference to how open–ended funds have the benefit of giving LPs far quicker access to investments than they typically would do from a closed–end fund. “An LP will typically have its capital called within six to 12 months,” said bfinance’s Anish Butani, versus longer periods for closed end funds.

Jeppe Starup, head of Private Capital & Real Assets at PenSam, told Infralogic that open–ended funds’ “flexibility to reinvest capital as needed streamlines operational management”, adding this makes it “easier to maintain consistent exposure and efficiently allocate resources within the sector”.

From a capital planning perspective, open-ended funds can “simplify the process significantly”, Starup added.

Open ended funds can also be used for “managing cashflows”, said the Australian superannuation fund LP, a reference to open–ended funds typically offering annual yield.

Starup said that Pensam, a Danish labour market pension fund, has not yet invested into an open–ended infrastructure fund but might consider doing so, particularly in cases where “the investment horizon [of the open–ended fund] is long-term and the primary source of value is derived from ongoing yield rather than short-term capital appreciation”.

In such scenarios “the fund structure can effectively support the objectives and risk profile associated with these assets”, Starup added.

Open ended funds are also “a good vehicle because we don’t want to sell an asset which is quite good after 10 years”, said one Swiss pension fund respondent to the bfinance survey.

Core open ended and the rest

The market also seems to have more sharply bifurcated between closed-ended and open-ended strategies.

The latter typically target core assets and 10% returns, versus 8-10% in the years prior to the late 2023 interest rate hike and yield of 6% plus, according to bfinance.

Closed–ended infrastructure equity funds target core/core plus 10-12% returns – versus 10% before the interest rates hike – and yield of 4-5%; and value-add returns of 12% plus and 3-4% yield, according to bfinance.

William Barrett, cofounder of the placement agent Reach Capital, said this bifurcation between core evergreen funds and the rest of the market makes sense. “Core assets are a good strategy for evergreen as they are long-term and yielding,” he said. “In comparison, core-plus, and value-add will be more typical for close-end funds. Essentially, some strategies are a more natural fit for evergreen funds.”

Meanwhile, some 61% of respondents to bfinance’s survey prefer funds of between 10 and 15 years. This compares with 34% preferring 25 year funds and 5% five-year funds.

“There is a clear drop-off in appetite once fund lives start pushing materially beyond 15 years,” a Nordic pension fund said in the survey.

“It is becoming clearer that open ended is good for core, while core plus and value add are in 10-15 year vehicles,” said Anish Butani.

Infrastructure managers themselves report seeing value in open-ended strategies. Gordon Hay at Morrison said an “open-ended structure lets us keep backing the best assets as they grow, and exit when value is fully realised”.

It is also nuanced: Hay doesn’t see open-ended as buy and hold, rather “it’s about having control over when and why to recycle capital”, meaning they can exit when they want to and then recycle the proceeds back into the fund. “Our approach is built on active realisation and reinvestment to compound value over time,” said Hay.

Another GP said open–ended funds provide top up capital alongside the closed end funds, enabling it to do bigger deals.

Open ended funds also provide a wider suite of products for LPs. A renewables investor said open–ended funds enable more time to develop greenfield projects where grid connection and planning timelines are unclear.

Concerns around value add

Another trend in favour of open-ended funds is that some LPs are not happy with the drift up the risk curve and are returning to their core roots.

In May the Alameda County Employees’ Retirement Association said it is seeking to rebalance its portfolio by investing in “lower-risk, core-plus funds” whose investments “possess true infrastructure characteristics.” This followed its discovery that value add strategies, which made up 86% of its portfolio had “not exhibited returns commensurate with the risks taken”.

Returns anecdotally for some open–ended funds look healthy; while also fundraising for open ended strategies meanwhile continues apace for some managers.

Brookfield’s 2018-vintage open–ended super-core infrastructure fund, which had raised some USD 14bn as of December 2025 compared to USD 9.1bn in November 2023, in April received USD 100m of commitments from Oklahoma’s Tobacco Settlement Endowment Trust Fund.

Natalie Hadad, managing partner in Brookfield’s infrastructure group and co-head of its open-ended core infrastructure fund, told Infralogic recently that demand was being driven “less by the level of rates” than by investors’ focus on “stability, predictability and attractive risk-adjusted returns” in a more uncertain environment.

But open–ended funds are not for everyone.

Gabriele Todesca, head of infrastructure investments at the European Investment Fund said his fund doesn’t “invest in open-ended structures” and has no plans to do so in the “near future”, adding the reason is that it’s “linked to our mandate requirements”.

Todesca told Infralogic in a recent interview that the EIF is committing up to EUR 2bn a year to infrastructure funds and that the sector has also become “increasingly attractive, in relative terms, from a financial perspective”.

Some LPs reported concerns around valuing assets in open–ended funds. There is a requirement when “funds are pooled with multiple investors” for “frequent and precise asset valuations”, said Pensam’s Starup.

“This increased scrutiny can introduce challenges, as inflows and outflows such as new investments or redemptions may create potential conflicts of interest among participants,” he added.

William Barrett at Reach Capital said valuations of evergreen funds are “definitely under more scrutiny than valuations of closed-end funds as it is also an entry point”. Closed end funds in contrast have only one entry point.

Slow fundraising pace

The pace of fundraising for open–ended funds among smaller managers appears to be slowish, too.

Fengate’s open-ended infrastructure fund, Fengate Infrastructure Yield Fund, which was set up in 2020, has raised some USD 1.1bn of commitments.

“Fewer than 10 strategies have raised more than USD 5bn, with meaningful dispersion amongst that group, too,” bfinance said, adding it will take time for managers to scale.

Yet there are signs that some of the newer strategies have attracted meaningful capital, such as Octopus’ open ended Sky Fund which has received sizeable commitments from Wales Pension Partnership and the UK’s workplace pension scheme, the National Employment Savings Trust.

Open–ended strategies also have remained largely OECD-focused. “So far there is a limited number of region-specific offerings, particularly in Europe,” said bfinance.

The market has also shifted since 2023 with the rise of open ended semi liquid strategies targeting wealth rather than institutional capital, which may have shifted focus from some managers away from institutional open ended fundraises.

Another dynamic has been the rise of continuation vehicles, which serve a similar function to an open ended fund given they both manage assets for longer periods than closed end funds.

Overall GPs and LPs alike see benefits of open–ended structures. More might well be in the works.

This is one of a series of articles by Infralogic based on findings from an in-depth bfinance survey of limited partners’ attitudes to the infrastructure sector.

A service of

Shape your future with Infralogic. Today

Explore unlimited content like this, available only in the platform.

Already a client? Sign in