More LPs want a piece of Asterion’s infra strategy

The Spanish manager’s third infrastructure fund is three times the size of its first one. But the GP retains the same mid-market strategy it adopted at launch seven years ago. Stefano Berra reports.

If any sign was needed that LP interest in the European infrastructure mid-market is back, look no further than Asterion Industrial Partners’ latest fundraising.

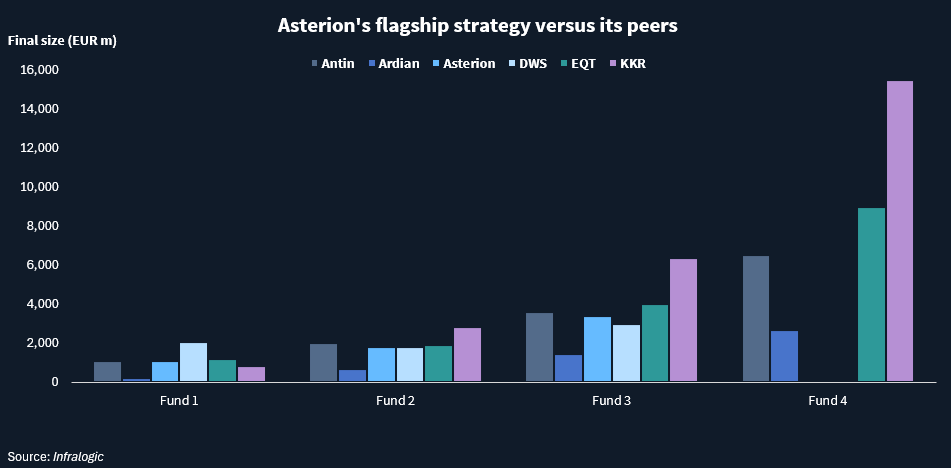

The Madrid-headquartered fund manager announced last month that it had raised EUR 3.4bn of commitments for its Asterion Industrial Infra Fund III, beating its EUR 3.2bn target. On top of that, it added an extra EUR 250m of co-investment capital.

Its quick fundraising took 18 months from the fund’s registration and concluded on 31 July. Similar timeframes were more commonly seen during the years before 2022, while more recently, funds often stay on the market for more than two years.

The biggest expansion of its LP base to date was one of the key factors that allowed Asterion to close Fund III at around twice the size of its predecessor, Winnie Wutte, founding partner at Asterion, who led fundraising, tells Infralogic.

“It was a combination of existing investors increasing their commitments and then roughly about 30 new investors joining for the first time,” she says.

Existing LPs mostly remained loyal, with a re-up rate of 86%, and a total of 68 investors committed to the fund.

Expanding LP base

North American LPs have traditionally been a dependable source of capital for Asterion and are increasingly allocating to Europe to escape volatility at home.

Sure enough, New York City Employees’ Retirement System (NYCERS) and Teachers’ Retirement System of Louisiana (TRSL) provided large tickets of USD 100m and USD 50m each to Asterion’s third fund, public records show. NYCERS is a new investor, according to data compiled by Infralogic, while TRSL doubled its commitment compared to the previous fund.

North American investors were instrumental in the latest fundraise by ICG, a peer of Asterion, with their contribution jumping tenfold compared to the previous vintage. Wutte, however, paints a more nuanced picture of Fund III’s sources of capital.

“The new investors came very evenly split between North America, Europe, and Middle East and Asia,” she says. “We had around 35-38% coming from North America and a similar amount from Europe, with the balance from Asia and Middle East.”

While many GPs are increasingly turning to private wealth investors to complement a sluggish flow of capital from institutional investors, Asterion is sticking with its traditional LP base of pension funds, insurance companies, sovereign wealth funds.

“We have very few high-net-worth and family offices,” says Wutte. “Our investor base is 95% institutional.”

This is not to say that the mix of investors has not changed since Wutte, alongside fellow founding partners Jesus Olmos and Guido Mitrani, set up Asterion in 2018 after leaving KKR.

“We have maintained some relationships from the past, but there is not a huge amount of overlap,” says Wutte. “There are a lot of new names that we have built up relationships with [at Asterion].”

Among new European investors, Italy’s Fondazione Enpam, a pension fund for medical professionals, was one of the largest LPs with an EUR 100m ticket, while Spain’s Pensions Caixa also made an investment, according to public filings. Germany’s Union Investment also disclosed in September 2024 that it was considering committing to the fund. Asterion declined to comment on individual LPs.

Wutte says pre-marketing was very important for a successful fundraising. “You have to start talking to people for years before you build up enough trust for somebody to come in,” she says. “There’s a lot of build-up behind the scenes that exceeds 18 months.”

This allowed the fund to reach a quick first EUR 1.5bn close in mid-2024, only a few months after launch, but most of the “concerted push” took place after that, according to Wutte.

“From the first close on it was really quite tough,” she says. “There were people who were expecting the market to get better, but the reality is that it didn’t.”

Sticking with European mid-market

Asterion has long argued that the European infrastructure mid-market is underserved by GPs and typically offers better returns than large-cap deals, with CEO Olmos telling Infralogic in 2020 that the firm did not want to become a “superfund”.

This is still paying off, according to Wutte. “We occupy a space in the European mid-market that is attracting a growing amount of attention,” she says. “That certainly was interesting for new investors coming in, that perhaps didn’t previously have meaningful European exposure or were looking to grow their exposure into the middle market.”

She is adamant that the firm wants to stick to its knitting, at a time when many GPs are adding more targeted equity strategies for specific sectors or regions, or expanding into infrastructure debt.

Wutte stresses that consistency has been Asterion’s secret sauce in a “very challenging” market. “We have been very consistent in delivering performance in our prior funds,” she says.

Publicly-available data seems to back up the claim. Asterion’s first infrastructure fund, which closed at EUR 1.1bn in early 2020, had delivered an 18.9% IRR by mid-2024 against a 10%-13% target, according to the latest available performance data by Santa Barbara County Employees’ Retirement System, an LP.

The fund has completed three exits at good prices – French metering firm Proxiserve, European renewables platform Asterion Energies, and Madrid-headquartered data centre operator Nabiax, with the latter delivering a money multiple of over 2x on its original investment. Another profitable exit, from Italian utility Sorgenia, has also been agreed.

Selling its UK assets has been harder. Infralogic previously reported that an attempt to divest “last mile” utility provider Energy Assets Group was halted last year, while talks over a possible separate sale of renewable heat assets of its portfolio company AMP Clean Energy were also put on hold. Other assets still held by the fund include fibre and tower operators in Spain and Italy.

Wutte is well aware of LPs’ intense scrutiny of distributions in the tough M&A market in recent years. “We’re working hard to deliver our strategy in the full knowledge that we are a closed-ended fund,” she says. “For us, it’s not just about buying, it’s also about selling and selling well to deliver returns.”

Larger fund, same-sized investments

Buying assets is the next task for Fund III. Its larger size raises the question of whether Asterion will set its sights on bigger targets.

Some of its most recent investments have indeed been larger than usual, such as the acquisition of a minority stake in Italian airport operator 2i Aeroporti for close to EUR 800m, although Asterion raised some EUR 200m of holdco debt from Ares to cover part of the cost.

Wutte insists that average ticket sizes will remain around EUR 250m, however. “Yes, the fund size has changed, but this means we will have more diversification in the fund in terms of number of deals,” she says. “Typically [the previous funds] would have done 10 deals. Now we will do maybe 12 or 14.”

Wutte prefers not to talk about any possible Fund IV yet. “What’s next for us is to continue to deliver and to perform,” she says.

For other European GPs such as Antin and EQT, the jump between their third and fourth flagship funds marked a step-change in the scope of their ambitions, with their fourth vintages raising EUR 6bn to EUR 9bn each, compared to third funds of around EUR 3bn-EUR 4bn.

When the time comes, Asterion’s next strategy will determine whether the firm’s future is to remain a mid-market veteran, or if it will be time to start thinking like a superfund.

A service of

Shape your future with Infralogic. Today

Explore unlimited content like this, available only in the platform.

Already a client? Sign in