MML Keystone takes value add infra to the next level

- Firm focuses on outsourced services, not pure finance leases, in sectors like circular economy

- MML Keystone targets essential societal needs, with investments in education and digitalisation

- EUR 935m raised by MML Keystone I fund, with significant investment progress

Asset leasing is becoming an increasingly popular sector for infrastructure investors, who have now targeted areas as diverse as airport equipment, construction machinery, and security cameras.

MML Keystone, the infrastructure strategy of MML Capital, is at the forefront of this trend, with its portfolio including refrigeration and catering equipment specialist Lowe Rental Corporation, drinks keg management platform Evaaro and crate lessor Global Packaging Services.

MML lives up to its value-add brand. Evaaro, for example, provides kegs to customers on a “pay per fill” basis, where customers just pay for the use of the keg each time it is filled, or a “pay per month” basis.

MML’s approach, which essentially provides outsourced services to clients, is in contrast to pure finance leases, which involve businesses leasing single assets over a long period and where the customer retains the assets at the end of the lease.

It is also very different to classic infrastructure investing, which is all about long and sticky contracts.

“We are focused on businesses where there is a service level that provides something beyond a financial lease,” MML Keystone co-managing partner Andrew Honan told Infralogic.

Using another of its portfolio companies as an example, he noted that GPS “is a pure asset pooler — a client uses a rented crate to ship to their end customer, GPS collects it from wherever that is and immediately delivers it to a new client.”

This results in much better efficiency, because if client owned its own crates or held them on a long-term lease, they would be coming back empty on their return journeys, resulting in utilisation rates capped at 50%, according to Honan.

Utilisation rates

Maximising utilisation is a key consideration for MML Keystone, demonstrated also by its ownership of Premier Modular, a lessor of “modular buildings” to education, healthcare, public infrastructure and commercial customers.

Honan cites education as an example of how modular buildings can help avoid the inefficiencies that can result from constructing permanent structures.

“Demographic trends move more rapidly than we might think when looking at year group sizes at individual schools — and if a school needs an extra class for a year, that may only last seven years,” he said.

While a permanent building in such a case might end up only achieving utilisation of 20% to 30% over its life, “a more flexible, shared asset can be moved to another school” if it is no longer needed by the school that originally leased it.

“We focus on what I call distributed infrastructure, which involves having as few as 5,000 assets at the low end or a million at the higher end, but the common feature is that we analyse the data associated with the assets to maximise growth and limit downside,” according to Honan.

MML Keystone’s approach differs from that of more traditional infrastructure managers which on the leasing side for example have targeted rolling stock, involving leasing trains to a single customer over a long period. The Keystone approach is undoubtedly on the core-plus or value-add end of the infrastructure risk spectrum.

Enhanced returns

While it has not publicly revealed its return targets, MML Keystone aims for “private equity returns” with downside protection.

Private equity returns obviously vary, but MML last year said it over the previous 12 months recorded an average multiple of 4.1 on invested capital across the eight transactions it announced, all of which were outside its infrastructure strategy.

Notwithstanding MML Keystone’s private equity leanings, the sectors it targets – circular economy, healthcare and education, digitalisation and energy transition – are similar to those of other infrastructure managers. MML Keystone specifically targets assets meeting “demand tied to an essential societal need” and has so far made four circular economy, one education and one digitalisation investment.

Its approach looks to have achieved strong support from LPs with its first fund, MML Keystone I raising EUR 935m by final close at the end of 2025, “among the largest on record for a new European strategy”, as MML noted at the time.

LPs to have backed the fund, which launched in 2022 under the name MML Infrastructure I, include the European Investment Fund, London-headquartered asset manager Schroders, Switzerland’s Partners Group and US-based investors StepStone and Wafra.

The fund is now “significantly invested, and (we) are approaching the second generation,” said Honan.

Having hired Honan at the time it launched its infrastructure strategy, MML hired fellow Macquarie veteran Sharand Maharaj the following year to co-lead it.

The two started working at the Australian financial group in 2009 and 2010 respectively as founding members of the principal investment business. While focused on private equity and debt, infrastructure-like deals were also in their remit, with deals including the 2014 acquisition of UK care home operator The Regard Partnership from their future employer MML. Regard was later acquired by the infrastructure arm of AMP Capital.

Infrastructure ambitions

The launch of its infrastructure strategy was a major development for MML, which was founded in 1988 as Mezzanine Management Ltd, with a focus on providing growth capital to mid-market companies.

True to these roots, MML’s current main strategy aside from MML Keystone is Partnership Capital, which for the past 20 years has been deploying its strategy of providing funding to businesses alongside management teams rather than traditional private equity style buyouts.

The strategy targets business-to-business focused companies across sectors, with examples including Waystone, a provider of compliance services to asset managers, and modular water treatment plant manufacturer RSE.

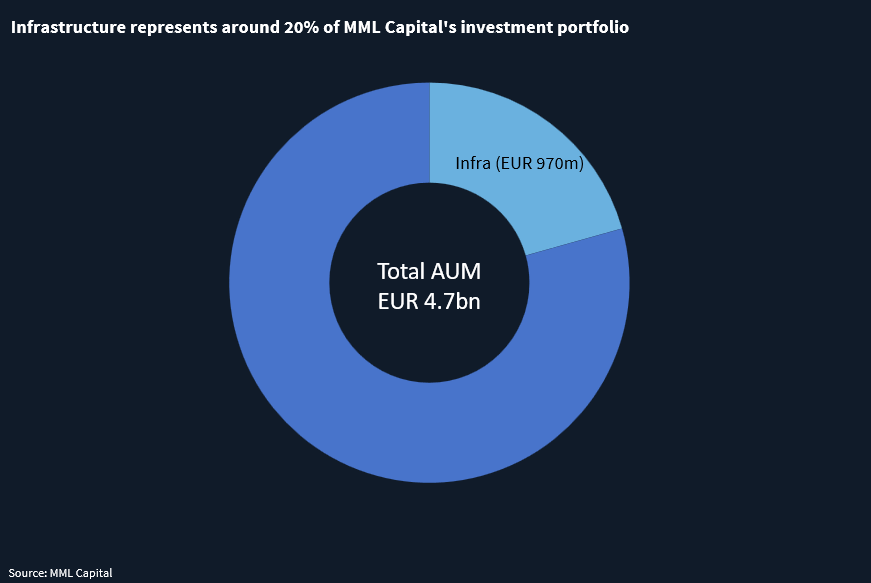

MML Capital now has offices in London, Paris, New York and Dublin and assets under management of EUR 4.7bn. Having raised nearly EUR 1bn through its fund MML Keystone is clearly already a major part of the group.

The Keystone strategy looks to be entering a major new phase of its development, with Infralogic recently reporting that advisors have been appointed for the sale of GPS.

Following its fundraising last year, MML Keystone will now be tested on whether it can match the rest of the group’s success in exiting investments.

A service of

Shape your future with Infralogic. Today

Explore unlimited content like this, available only in the platform.

Already a client? Sign in