Infrastructure’s growing appeal versus real estate

For institutional investors, real estate is the obvious alternative to equities and bonds, not least given its relative simplicity versus other parts of private markets.

“Lots of people own a house after all,” said Gravis chief investment officer Anthony Curl, while acknowledging that real estate has diversified in recent years from sectors such as residential and office property to areas such as student accommodation, data centres and healthcare real estate.

Infrastructure in contrast is complex given its broader ranges of sub sectors, and “not every institutional investor has the governance budget to assess those”, added Curl.

Infrastructure deal tickets are also typically bigger compared to real estate, so it generally attracts a narrower institutional investor base, said one private markets investor. This has changed somewhat with the proliferation of a broader range of infrastructure funds from the sub-USD 100m through to the mega funds.

Real estate also generally features more prominently than infrastructure in institutional portfolios. Average private markets allocation for institutional investors of real estate equity – including long income, which refers to leasing commercial properties for up to 250 years – is 30%, versus 13% for infrastructure equity, according to a private markets survey published this year by Aviva Investors.

But while real estate might seem fundamentally more attractive on paper, infrastructure is currently on an upward curve versus real estate.

Latest data reflects the point, with some 60% of institutional investors saying they want to be overweight in infrastructure within their real asset portfolio, according to a survey of 40 institutional investors carried out by investment consultant bfinance and shared with Infralogic.

In contrast, just 27% of those surveyed said they want to be overweight to real estate, while 13% said they want a balanced portfolio of the two real assets sectors.

“Infrastructure is increasingly viewed as the anchor real asset allocation, offering greater visibility on cash flows and downside protection,” said bfinance, which surveyed a mix of pension funds, insurers, sovereign wealth funds and endowment funds from EMEA, Asia-Pacific and North America.

Other data supports the view with 38% of institutional investors saying they intend to increase their allocation to infrastructure equity, according to the Aviva Investors private market survey, higher than all other parts of private markets.

Plight of real estate

Real estate has been particularly impacted by the rise of interest rates as well as valuation resets, two private markets sources said. Capitalisation rates, the expected annual rate of return from properties, have “gone up”, said one private markets investors, meaning valuations have come down. “This is good for investors coming in now – potentially – but less good for investors already in,” said Anthony Curl.

These factors help explain the current growing interest in infrastructure at the expense of the more traditional real estate, the private markets sources said. “Real estate remains relevant, but faces deeper cyclical and structural challenges,” said bfinance.

“Infrastructure doesn’t spike up and down as much as real estate,” said one of the investors, although added that infrastructure equity is “relatively smooth versus public markets”.

One large US institutional investor respondent to the survey said that while real estate “is not going away”, it “continues to be in a very deep down-cycle”. “I still like real estate, just not as much relative to infrastructure,” added the investor.

Ohio’s School Employees Retirement System (SERS) – a US public pension fund that provides retirement benefits and post-retirement healthcare to non-teaching public school employees – offers one of the clearest examples of the shift.

Board minutes show trustees approved a new asset allocation in April that cut the real estate target from 13% to 7% and raised infrastructure from 7% to 10%, effective July 1, 2026.

The transition for the system, whose infrastructure portfolio currently has a market value of about USD 1.7bn, is expected to take two to three years, a SERS spokesperson told Infralogic. The higher infrastructure target reflected a search for “stable income returns,” the spokesperson added. The additional allocation will be deployed through “both” existing managers and “new mandates” and “diversified across sectors”, the spokesperson said.

North Dakota’s Board of University and School Lands, a state board that manages assets for schools and other public beneficiaries, points in the same direction. Its August 2025 minutes described a strategic theme of “shift from real estate to infrastructure”, tied partly to rising power demand from artificial intelligence. The accompanying target allocation changes reduced real estate from 10% to 8% and increased private infrastructure from 7% to 10%.

One LP to infrastructure funds told Infralogic that a “slight overweight to infrastructure as opposed to real estate is warranted” so long as “you are in the preferred segments”.

The rotation is not universal. Orange County Employees Retirement System, the pension plan for public employees, approved a 2026 real estate investment plan that authorised USD 50m to100m of core commitments and USD 150m to 225m of non-core commitments.

LACERS, the Los Angeles municipal pension scheme whose real estate portfolio stood at 5.4% of plan assets against a 7% target at the end of 2024, set out up to USD 300m of real estate commitments for 2025-26 and said the portfolio was expected to move gradually towards target over the next few years.

But ultimately, infrastructure lies across multiple asset classes: private equity (given the growing number of infrastructure value add deals being transacted); commodities (given its exposure to oil and energy pricing markets) and real estate, given both invest in the likes of data centres and student accommodation.

But the survey data suggests that despite LPs’ opportunity to target similar assets in both real estate, they get better overall value from infrastructure currently.

“The shift towards infrastructure looks less like a vote against real estate and more like an evolution in classification,” said Callum Fraser, Head of Private Markets Equity Investment Specialists, Aviva Investors “Investors are becoming more agnostic about labels and more focused on outcomes: resilience, inflation protection and long-term income.

Infra’s growing popularity

As real estate continues to be buffeted by headwinds, infrastructure’s core characteristics meanwhile appear attractive in the current market.

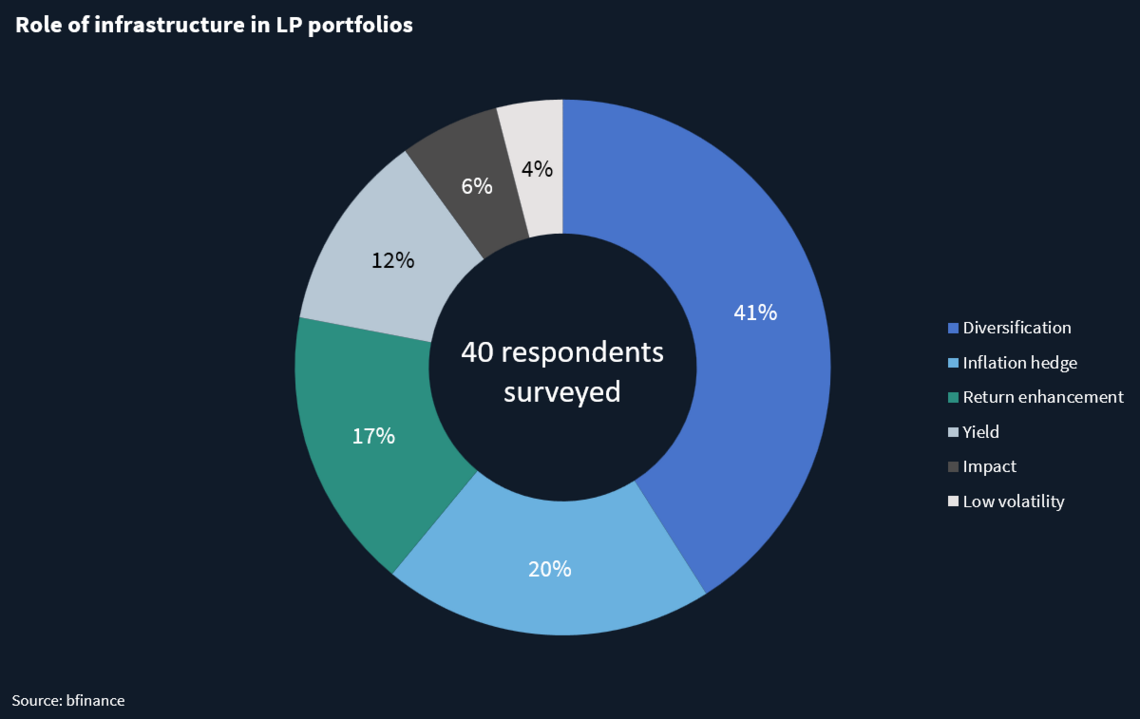

It delivers “multiple objectives”, including diversification, inflation hedge, return enhancement, yield, impact and low volatility, according to the bfinance survey, which added “infrastructure is no longer defined by a single role, but by its ability to deliver multiple objectives”.

The most popular role of infrastructure in LPs’ portfolios is diversification, with some 41% of respondents saying it offers this objective. This means its assets, such as toll roads, utilities and telecom towers, are relatively immune to economic cycles and therefore can provide returns that are largely uncorrelated to stocks and bonds.

Inflation hedging is also a popular feature of infrastructure investing for LPs, with a fifth of respondents saying this is a reason to invest in the sector.

One LP told Infralogic said the infrastructure sector provided inflation protection across its different risk strategies, not just in areas such as regulated utilities and renewables with tariffs, sectors which have obvious inflation linked revenues.

“Even in core plus sectors that inflation linkage was still strong even if contractual, which was quite a pleasant surprise,” said the LP.

One UK defined benefit LP pointed to how “core infrastructure offers contracted, long-term, inflation-linked income” while in contrast “core real estate doesn’t always give you that”.

Higher returns

As well as inflation protection, LPs also increasingly see the sector as offering high returns, with some 17% of respondents saying infrastructure provides return enhancement.

An Australian superannuation fund interviewed for the survey pointed to the “opportunity to outperform” from infrastructure, given “the quantum of capex is changing the nature of what the asset class can do”.

This combination of inflation linked returns and some risk adjusted returns is key to the sector’s current appeal.

LPs “increasingly structure portfolios around a core of contracted cash flows”, including inflation protection, but which are also “complemented by selective higher-risk sleeves”, said bfinance.

This data is reflected in the nature of the survey respondents themselves, 46% of whom target core plus and upwards investments, 34% core/core plus and just 20% on core.

Just 4% of respondents to bfinance’s survey said they invested in infrastructure as it offers low volatility, although typically they would have started investing in the sector through core funds.

But one LP told Infralogic that low volatility is the most important reason for investing in infrastructure. “Low volatility has always been important and remains important,” said the LP.

“Part of the purpose of investing in infrastructure is that it provides stable, resilient downside protected and inflation linked cashflows,” he added.

Also, just 12% said they did so because infrastructure offers yield, a typical component of a core infrastructure fund, further suggesting a desire for slightly higher risk portfolios that are balanced by inflation protection.

This is the second of a series of articles by Infralogic based on findings from an in-depth bfinance survey of limited partners’ attitudes to the infrastructure sector.

A service of

Shape your future with Infralogic. Today

Explore unlimited content like this, available only in the platform.

Already a client? Sign in