EIF looks to build niche infrastructure fund portfolio

- EIF grows infrastructure programme to EUR 1.5bn-EUR 2bn annual commitments

- (EIF targets biogas, defence infrastructure specialists for new capacity creation

- EIF prioritizes greenfield investments, avoids pure income from existing assets

For most of the past five years the European Investment Fund (EIF), the European Union-backed investment arm of the European Investment Bank (EIB) Group, has built its infrastructure programme around one thing, rapid growth.

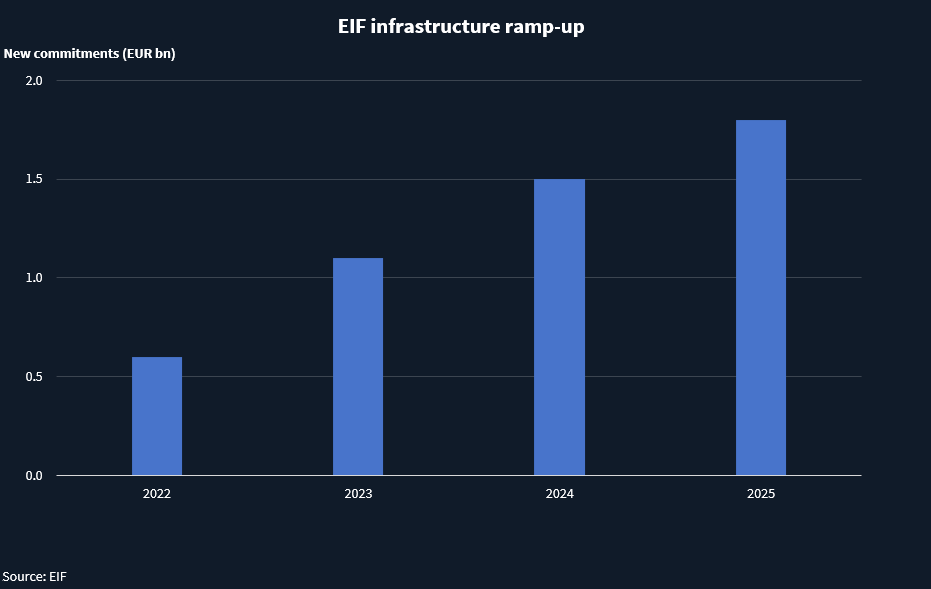

When responsibility for infrastructure investing moved from the EIB, the EU’s long-term lending institution, to EIF around five years ago, annual volumes were “in the low hundreds” of millions, says Gabriele Todesca, EIF’s head of infrastructure investments.

Since then, it has scaled quickly and today is running roughly EUR 1.5bn to EUR 2bn of new infrastructure commitments a year.

Todesca said Infrastructure is “crucial for many of the policy thematics in EIF’s focus”, particularly the green transition, social inclusion and EU strategic autonomy, and has also become “increasingly attractive, in relative terms, from a financial perspective”.

That combination has “led to a rapid increase in allocations from EIF-managed programmes over the past few years,” he added.

EIF invests in infrastructure mainly through primary commitments to third-party funds, with selective co-investments alongside the managers it backs.

But as the platform has grown, its priorities have sharpened. For instance, EIF is now actively pursuing specialist managers in biogas, and it wants to make an early move into a dedicated defence infrastructure fund, a category it says is still thin in Europe.

Todesca said the EIF has been looking closely in recent months at biogas generation, an area it expects to back through “a couple” of specialist fund commitments for the first time. The attraction is not only decarbonisation, he said, but also energy security.

“It’s also a way to have locally produced gas that we can strategically use for the consumption of the European Union, instead of having to import gas from outside of the European Union,” he said.

The biogas push comes within an energy-heavy programme. Todesca estimates energy accounts for around 50% to 60% of EIF’s infrastructure activity, spanning generation, storage, networks and energy efficiency, including EV charging.

The intention is not to abandon generalist infrastructure funds, he said, but to complement them with more specialised strategies as the market matures.

“We like the concept of specialist and dedicated strategies,” he said, arguing dedicated teams tend to have stronger networks and deeper technical capability.

Recent examples of that specialist tilt include an investment in Gore Street EU Fund, an energy infrastructure fund managed by UK-based Gore Street Capital, focused on the development of utility-scale energy storage (BESS) solutions in the EU.

If biogas is already translating into near-term commitments, defence infrastructure is earlier stage.

Todesca said the market for specialist defence infrastructure funds is “currently non-existent, basically, in Europe”, which is why EIF is pushing to back its first one into early 2026.

EIF has occasional defence-linked exposure through generalist infrastructure funds, but it has no dedicated defence infrastructure specialist in the portfolio yet and is now in discussions with managers exploring the space.

The opportunity set, Todesca said, is less about weapons and more about enabling assets tied to defence readiness and resilience.

“There needs to be a core component which is directly related to defence and military,” he said, pointing to areas such as accommodation and other facilities for military personnel and military logistics sites.

Todesca said the category is only now being formalised. Managers have long made occasional defence-related investments inside broader strategies, but “they were not labelled as such” and few have built dedicated funds around the theme. As a result, he said EIF is unlikely to back more than one specialist strategy next year, even if “the appetite will be there” over time.

EIF in numbers

| Commitment activity | Key figures |

| Annual commitments | EUR 1.5bn to EUR 2bn |

| Funds backed per year | 15 to 20 |

| Typical ticket size | EUR 70m to EUR 90m, sometimes above EUR 100m |

The move toward specialist themes sits within constraints that shape which managers EIF can back. Todesca said EIF’s capital is mainly EU public money, so funds need a clear EU focus.

Strategies can allow some exposure to non-EU countries, but EIF is often approached by managers running global mandates that fall outside those parameters. Even where EIF uses formal thresholds, he said the goal is to push capital into the EU as far as possible.

EIF also draws a hard line on fund structure. It does not invest in evergreen or open-ended vehicles. “We want to have certainty of exit,” Todesca said.

Even when a fund fits EIF’s mandate, Todesca said the most common reason it falls away is alignment. “We see a lot of funds that we’re rejecting because of lack of alignment,” he said.

He also cited proposals where the infrastructure team is housed inside a larger group and does not have full autonomy, with key decisions effectively shaped by the parent company rather than the partners running the fund. “We want to be fully aligned with the people who are making the decisions,” he said.

EIF leans toward funds that look to build new infrastructure rather than trading existing assets. Todesca said it expects most investments to be greenfield, including capex-heavy expansions that create new capacity. “We want to invest in the creation of new assets, and not simply in the transfer of existing assets,” he said.

That definition is broader than backing entirely new sites. A wind farm acquired with the objective of repowering can still qualify, he said, because the capital is creating “new assets”.

What EIF wants to avoid is paying for pure income from existing infrastructure with no expansion plan. “If it’s existing and there’s no plan to do anything with it other than running it for an income, that’s pure brownfield for us,” he said.

Recent EIF fund commitments

| Fund Name |

| Alba Infrastructure European Operational Projects Fund II |

| Equita Green Impact Fund (EGIF) |

| Qualitas Energy Credit Fund |

| Rotonda Transformation D |

| Serena Infra II |

EIF requires co-investment rights alongside its fund commitments, but Todesca said they are an add-on rather than the main reason EIF backs a manager. They are used selectively, he said, where an asset can combine a sound financial case with a clear policy angle.

He cited a co-investment alongside an EIF-backed fund in the “deep remediation and redevelopment” of a port area in the Netherlands, bringing land that was “basically not usable” back into productive use.

EIF is also using its infrastructure programme to back newer teams. Todesca said EIF is active in emerging managers, particularly spin-outs, but it prefers teams that can point to a track record. One recent example is EIF’s commitment at first close to Alba Infrastructure European Operational Projects Fund II, a 2025-vintage fund led by former 3i Infrastructure executive Stephane Grandguillaume.

Todesca said EIF wants to do more to help Europe use energy “more smartly”, through energy efficiency and storage. He pointed to investment themes such as improving energy efficiency in buildings and companies, and to batteries and other storage solutions. EIF’s view, he said, is that Europe cannot simply keep adding supply, and that at times “the marginal value” of investing in flexibility and smarter use of the grid can be higher than building more generation.

EIF’s appetite for biogas, defence and flexibility all sits within the same filter, it wants its money to help create new capacity. “We want to invest in the creation of new assets, and not simply in the transfer of existing assets,” Todesca said.

A service of

Shape your future with Infralogic. Today

Explore unlimited content like this, available only in the platform.

Already a client? Sign in