Decade-old Wren House charts new course

The Kuwait Investment Authority’s direct infrastructure investment arm responds to major changes in the investment landscape with new strategies on asset rotation, partnerships and Europe.

For much of its life since its launch a decade ago Wren House has focused on buying stakes in core assets and holding on to them for the longer term.

The investor on behalf of the Kuwait Investment Authority (KIA) has over this period acquired stakes in household name infrastructure assets such as Associated British Ports and London City Airport – a strategy that has helped it establish its current portfolio of 14 companies and assets under management of some USD 9bn.

But now, according to its CEO Phillippe Busslinger, instead of focusing mainly on acquiring assets, it plans to sell some of them within five to 10 years or so of buying them, akin to the way general partners of blind pool fund operate.

The move takes place at an important juncture for the investor, with a renewed focus on Europe and quest for partnerships with other managers. It also takes place as Wren has been awarded a new multi-billion capital allocation from the KIA to invest into European and North American infrastructure assets over the next five years. This mirrors its first investment window from 2015 (when Wren was established) to 2020, and second one from 2021 to 2024, for each of which it invested USD 5bn.

“The first two KIA allocations [in 2015 and 2021] were about building out a diversified portfolio,” says Busslinger. “Now we are investing with the aim of acquiring companies, adding value to them, and then crystallising that value by selling those companies,” he adds.

| Wren House’s top five deals by size | ||||

| Asset | Description | Date of acquisition | Stake (%) | Est cost (USDm) |

| Almaviva | Private hospital group | Dec-21 | c.70% | 1000 |

| DCLI | Inter-modal chassis leasing | Dec-22 | 33% | 850 |

| NSMP | Midstream | Sep-18 | 51% | 800 |

| ABP | Ports | Jul-15 | 10% | 650 |

| PTI | Towers | Feb-23 | 10% | 750 |

| Most recent five deals | ||||

| Electrip | EV charging | Jan-23 | 50% | 150 |

| PTI | Towers | Feb-23 | 10% | 750 |

| SeaCube | Container leasing | Nov-23 | 50% | 500 |

| Petit Forestier | Refrigerated vehicle leasing | Aug-24 | 34% | 600 |

| QTS Strategic Partnership | Data Centers | Nov-24 | 40% | 200 |

Wren in 2023 bought a 50.01% stake in European-Turkish electric vehicle charging company, Electrip, and since then has set it on a course of expansion across Italy, Greece, Bulgaria, Poland and Croatia as well as its home market of Turkey.

In line with its new buy and sell strategy, Busslinger says “Electrip is an example of where we might bring it to market after enhancing it”.

Older assets in Busslinger’s portfolio might also be available for sale. “Some of the 14 assets we plan to monetise, the rest we will hold for the long term,” says Busslinger.

In February Infralogic reported that Wren House at the time was exploring a sale of its stake it has held since 2018 in gas pipeline firm North Sea Midstream Partners.

NSMP is “one of the assets if we were to get an offer we would consider it”, says Busslinger, although in truth he is in two minds whether now is the best time to sell.

“In the US, gas assets go for very high price, but in Europe it is more of a question mark,” he says. However, he adds that given “energy security and some US energy investors looking for opportunities it may became more fashionable than it has been over the past years”.

Assets that he expects will remain in Wren’s portfolio include its stake in London City Airport. Although OTPP has sold its stake in the airport to Macquarie, and OMERS and AimCo are in the process of selling theirs, Busslinger believes “there is significant work to be done on the asset and we remain committed to it. We will work with the new partner [Macquarie] to create value”.

The reason for the strategy shift towards buying and selling assets is partly to do with economics: “It comes at a time when people have stopped believing that returns in infrastructure are just going up,” says Busslinger, meaning that buying with a view to enhancing and fairly quickly selling assets is a way of maximising returns.

He is not alone in adopting this new strategy of buy and sell – it’s “part of a broader trend of direct institutional investors rotating capital”, Busslinger says.

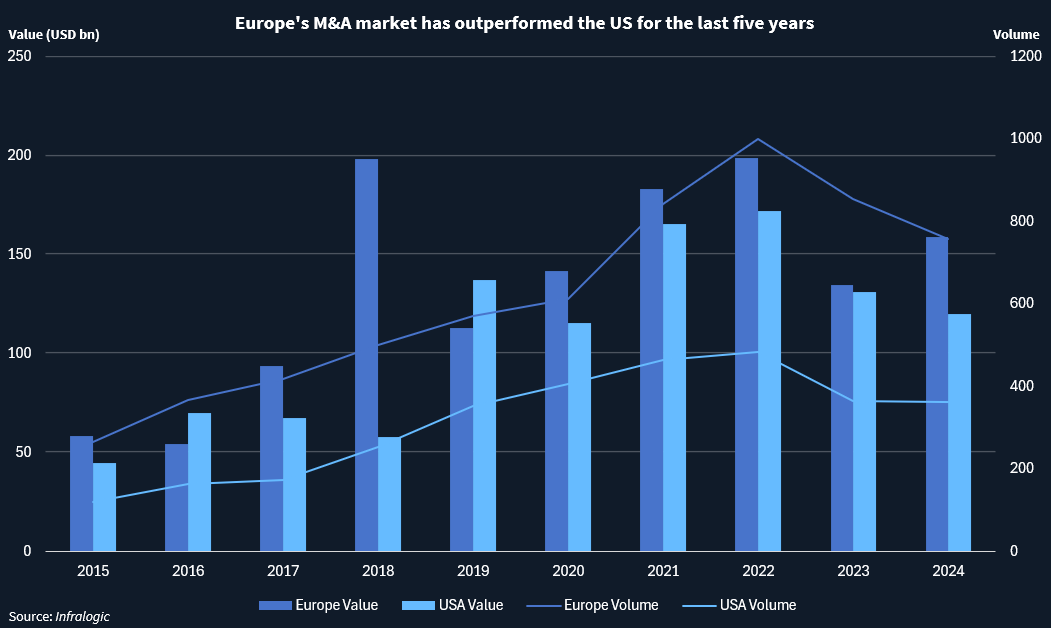

Fresh refocus on Europe

Amidst this strategy shift, one question is where Wren will choose to invest – and this also throws up a potential shift of direction, including rebalancing its portfolio back to Europe.

London-headquartered Wren spent its first five years solely investing in Europe, only doing its first deal in the US, buying Illinois-based fiber internet provider i3 Broadband, in 2020. Busslinger joined in 2022 with a mandate to “refresh its strategy”, including “rebalancing its portfolio” globally, which meant setting up an office in New York in 2023 and doing more deals in the US.

Busslinger – who points out that the last four of Wren’s last five deals were US ones – is a big fan of the US’ M&A machine, particularly its can-do attitude when it comes to dealmaking.

“Culturally the US is more transaction-minded and creative, finding ways to get a deal done in terms of earnouts, structuring senior and junior equity,” he remarks, adding that “in Europe they have a harder time bridging the bid-ask price gap”.

Europe also has a number of large institutional investors, such as PGGM, Axa and Allianz, which have a lower return target than general partners with blind pool funds; which means “you have more competition from investors with lower target returns than GPs in the US”, says Busslinger.

This brings up the price of deals and makes it harder for the likes of Wren, which targets core plus returns, to win deals, he says.

However, today he sees “significantly higher need for capital in Europe versus what we thought we had in Europe a year ago”, pointing to Germany’s EUR 500bn infrastructure sending plan as an example of this.

“This will require meaningful third party capital, and other European countries are trying to do the same. There is a lot of demand for infrastructure private capital,” says Busslinger.

Investment is also needed to fill Europe’s technical gap: “In comparison to the US, we lack technological innovation in Europe that will support the digital infrastructure and energy transition deals,” says Emmanuel Gionakis, Wren’s global digital head.

Gionakis points to how the US administration has incentivised “every single US AI company to do AI training in the US” – a reference to the process of feeding an AI model large amounts of data to teach it how to perform specific tasks. Trump did this earlier this year by seeking to impose controls on unrestricted exports of advanced computer chips and other AI technology to a number of countries, not just the ones it has identified as America’s adversaries.

“Who will do all this AI training in Europe?” asks Gionakis, adding there are no “AI companies in Europe that can do this at the scale it is happening in the US”.

Steps are being taken by European government to improve the continent’s technology: Gionakis points to French state plans to invest in French satellite operator Eutelsat to create a “European equivalent of Starlink”, SpaceX’s satellite internet giant. In August last year, EQT Infrastructure bought a stake in Eutelsat’s passive ground infrastructure assets.

Overall, Busslinger expects that Wren’s pipeline of deals will become “more balanced going forwards” – suggesting its next four deals might be more of a mix of US and European ones than its recent deals.

Indeed, the flow of deals in recent months linked to Wren on the pages of Infralogic have in the main been European ones, including energy-from-waste business Urbaser, a stake in a large EfW plant in Dublin being sold by EQT’s Encyclis, and Swiss data centre operator Green.

Yet Busslinger retains some scepticism towards Europe opportunities: it “remains to be seen” whether there will be an “oversupply of projects” and if there “is enough demand out there to go and invest capital in an unrestrictive way”.

Rise of GP partnerships

In addition to where Wren will invest, there is also the question of how it will do so, and this also throws up interesting strategic drift involving more “partnerships with GPs”, says Busslinger, adding this is a “great opportunity” and one that shines a light on the evolution of institutional investors and managers alike.

Institutional investors were in the early 2010s the biggest investors in infrastructure, while GPs raised funds of GBP 1bn or so that in today’s terms look tiny, says Busslinger, who before joining Wren held several roles at OMERS Infrastructure.

Today is a totally different world – not only have GPs’ funds exploded in size and ambition, but many “direct” institutional investors have exhausted their ability to write big cheques”, either because they have reached their target allocation for infrastructure or because their balance sheet haven’t grown sufficiently to allow them to do so.

Against this backdrop, Busslinger questions whether the “small handful of institutional investors” – including the likes of ADIA, GIC as well as Wren – want to “compete with GPs” or make partnerships with them, whether this be in the form of co-investments or “co-underwrites” (where Wren might take a small stake in a direct deal outside of a consortium).

Such a “partnership” strategy – already played out by Wren on deals such as its purchase of a 10% stake in Phoenix Towers from Blackstone in an equity syndication – has benefits for both GPs looking for extra returns and direct institutional investors seeking access to hard-to-get deals.

Wren is also well placed to forge such partnerships, given its parent, the KIA, is also a major limited partner in funds managed by GPs.

Ultimately it is also all part of parcel of Wren seeking to be a “bit more creative”, Busslinger says – a strategy which is also echoed in its choice of assets to target, having already strayed into areas some investors have steered away from for their value-add qualities, including healthcare and asset leasing. In addition to the waste sector, Wren is also mulling the utilities sector to determine if double digit returns can be achieved.

Wren this year celebrates its tenth birthday. Much has changed in the interim years, and Wren like all direct institutional investors is having to evolve with the times.

A service of

Shape your future with Infralogic. Today

Explore unlimited content like this, available only in the platform.

Already a client? Sign in