Data center boom sees explosion in bulge bracket project finance

The emergence of digital infrastructure, and data centers in particular as the dominant sector in the infrastructure world has driven a rush to obtain capital for developers and their projects from all possible sources.

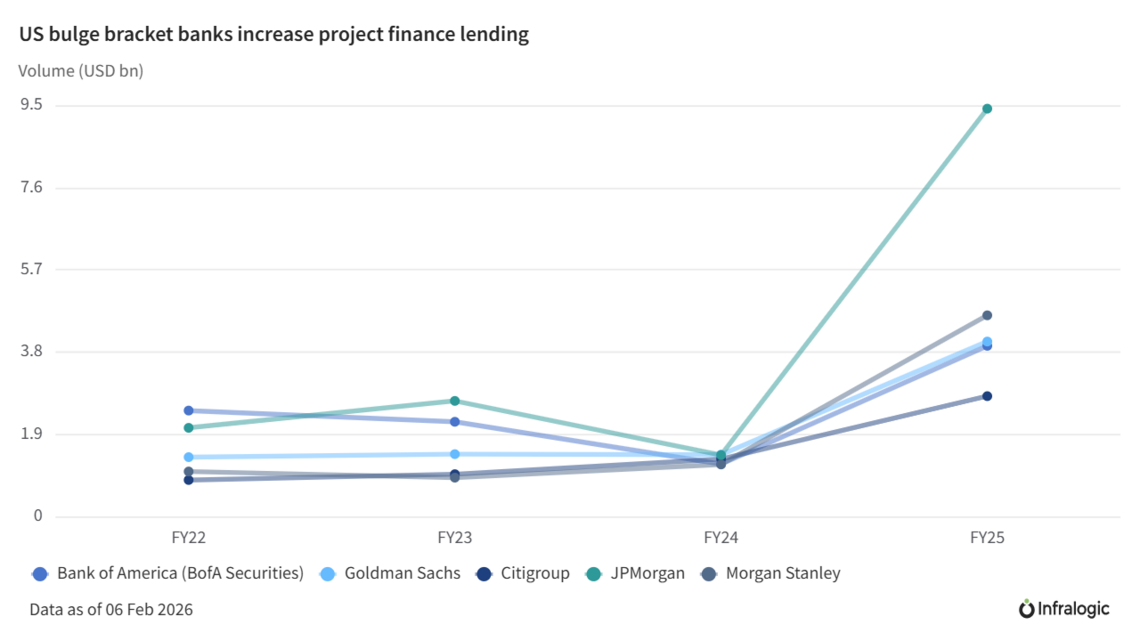

While Japanese and European commercial banks typically dominate Infralogic’s project finance rankings, over the course of the past 12-18 months the US bulge bracket banks (traditionally Bank of America, Citigroup, Goldman Sachs, JPMorgan, and Morgan Stanley) have increased their participation in project finance deals.

JPMorgan featured in the top ten in the broader North America loan providers section in Infralogic’s Project Finance Rankings 2025 report for the first time in four years.

According to Infralogic data on US project finance deals, the five American bulge bracket banks moved up significantly in the 2025 rankings versus 2024. The highest-ranking of the five, JPMorgan, rose 22 spots to sixth place via a 562% increase in the volume lent year over year. The remaining bulge bracket banks grew by 182% (Goldman Sachs), 285% (Morgan Stanley), 225% (BofA), and 109% (Citigroup) year-over-year, respectively.

The rapid rise in project finance for these banks has mirrored the data center and AI boom over the past 18 months, and the two are not mutually exclusive.

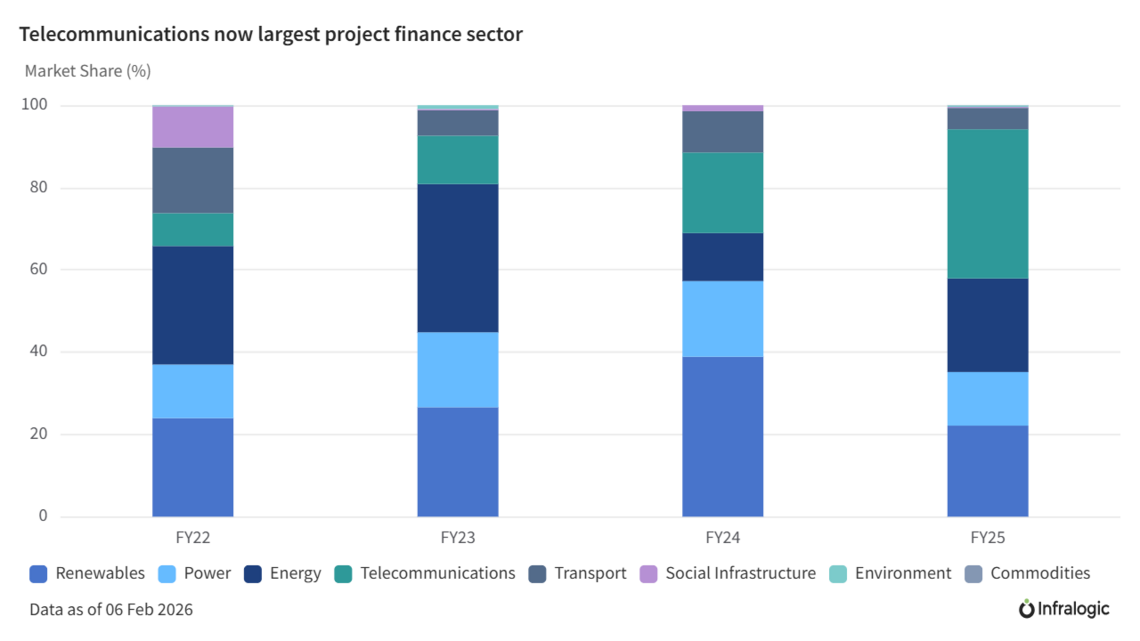

*Telecommunications = “digital infrastructure”

Deal structure preferences and definitions of project finance

As the definition of which projects are suited to utilizing project finance expands, the data center construction boom is creating new opportunities for the largest US banks and greenfield deals to adopt increasingly project financeable traits.

“To bring new capacity online quickly, hyperscalers are adopting an ‘all of the above’ approach – both to procuring compute and relating to financing products,” said Fuat Savas, co-head of infrastructure finance and advisory at JPMorgan.

“Financing methods now include use of the corporate balance sheet, leases, joint ventures and structured capital, among others. The fact pattern of ‘small company needs to build a big project’ is becoming more prevalent around the world, and that is a fact pattern that lends itself to project finance.”

As project sizes balloon, hyperscalers can no longer afford to carry these builds on balance sheet without risking a downgrade of their credit ratings. Over the past 18 months, many developers have shifted to procuring financing via project-level special purpose vehicles, creating large PF-style financings, which bulge bracket banks have flocked to.

Joint ventures with infra funds, private equity, hyperscalers, and sovereign wealth funds are another driver, as multi-sponsor platforms naturally require PF-style risk allocation and structuring. At the same time, smaller developers and new entrants, AI firms, neoclouds, power players, and real estate groups, are taking on outsized projects that can suitably utilize project finance structures.

These dynamics are widening the definition of project finance and drawing bulge bracket banks deeper into the market. With strong structuring teams and the ability to underwrite multibillion dollar tranches, they are increasingly interested in datacenter financing.

Inside the bulge bracket bank

There are several internal, structural reasons why these big US banks are becoming more involved in the data center project finance sphere, including the prevalence of active ABS desks and strong, existing real estate finance arms.

“Banks like fee income. If you can underwrite a large data center financing that you know you can syndicate, and you also have an active ABS desk, you essentially hold both ends of the business. You underwrite the construction, and you’re also positioned to handle the takeout,” said Maniesh Kharti, director of project finance at NORD/LB.

For JPMorgan, the key to the rapid growth of their project finance activity could be attributed to an alignment of strategies between project finance and real estate teams.

“Data center construction lending is evaluated and booked out of the firm’s Securitized Products Group (SPG), as part of its commercial real estate book of work,” said Savas. “This business generally has the capacity to take larger ‘hold’ positions compared to typical infrastructure project finance syndicates.”

As a result, the ultimate hold for an LNG deal would be between eight and 10%, while it can be up to 60% in commercial real estate transactions, Savas explained. For some of these mega data center deals, that can mean banks taking on multi-billion-dollar tranches per deal.

On the other hand, Japanese and European project finance lenders tend to take smaller chunks of many deals, Savas said.

This was shown in Infralogic’s data as the US banks had a lower number of deals in 2025 compared to more traditional project finance lenders. While JPMorgan provided USD 9.42bn across 29 deals, Mizuho, which ranked one spot higher, provided USD 9.68bn across 64 deals, and Natixis, although one spot below JPM, provided USD 7.9bn across a total of 52 deals.

Goldman Sachs participated in 22 deals, Bank of America in 27, Morgan Stanley in 26, and Citigroup in 18. This pales in comparison to the whopping 146 deals that lead loan provider MUFG participated in during 2025.

For data center project finance in 2025, the five US banks loaned a total of USD 13.28bn, compared to approximately USD 600m in 2024, according to Infralogic data. JPMorgan ranked first by volume, USD 6.72bn.

“Data center financings blend real estate and project finance. A lot of banks look at them from the real estate desk, but those desks can’t underwrite power generation risk, which is why you often see the assets financed separately,” said NORD/LB’s Kharti.

Bulge bracket banks are also quietly retooling internally. Goldman Sachs told the Wall Street Journal that it was expanding its AI influence by establishing an infrastructure financing division within its global banking and markets divisions. JPMorgan lost its head of North America digital infrastructure, Jon Edwards, to Switch, underscoring the talent churn as banks and investors all compete for valuable digital infrastructure expertise.

“With recent focus on data centers, we have grown our team and our capital commitment to hyperscale data center lending. We are committed to adopting a product agnostic approach to this rapidly growing sector, ensuring that we display competence and thoughtfulness across public and private debt and equity,” added Savas when discussing JPMorgan’s response to the sector boom.

The boundaries of project finance growth

Despite this growth, there has been little movement for these banks outside of the digital infrastructure space.

“I know they’re plugging for the data center deals. But in power and energy, I just haven’t seen that,” said a lead banker at an established project finance bank. “I haven’t seen an increase in their activity outside specific LNG projects.”

In other sectors, these large US banks have not seen the same increase in participation as in digital. In the 2025 Rankings, Morgan Stanley placed 19th in non-telecommunications project finance deals, providing USD 2.98bn across 18 deals, according to the data.

These banks were active participants in some of the major LNG transactions, although the banks’ rankings by volume and position have decreased since 2023.

For the US banks, it will be a continued focus on data centers, GPUs, and fiber that spurs this uptick, Savas added.

A service of

Shape your future with Infralogic. Today

Explore unlimited content like this, available only in the platform.

Already a client? Sign in