Brookfield’s wide-ranging AI infrastructure strategy

- BAIIF to acquire up to USD 100bn of assets across AI infrastructure value chain

- AI infrastructure funds remove overconcentration risk from traditional funds

- Brookfield targeting GPU market with predicted sales of USD 4tn in decade

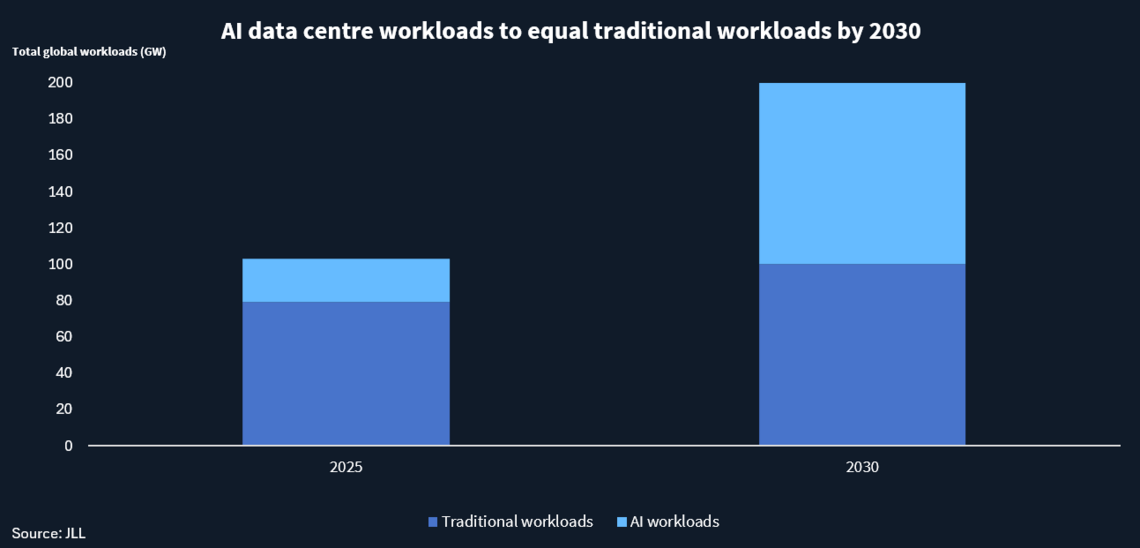

The investment opportunities that the rise of artificial intelligence presents to infrastructure funds, which have been investing in data centres for more than a decade, are well known. Nearly 100 GW of new data centres are expected to be added between 2026 and 2030 as AI demand grows, doubling global capacity and requiring up to USD 3tn of investment, according to real estate firm JLL.

Infrastructure funds are seeking to address this opportunity in various ways, one of which is simply to launch dedicated AI infrastructure funds. Brookfield was first out of the blocks last year, with its Brookfield Artificial Intelligence Infrastructure Fund (BAIIF). The fund when it launched in November had secured USD 5bn of capital towards its USD 10bn target, with backing from the tech giant and major AI player Nvidia and the Kuwait Investment Authority (KIA). “Together with additional capital from its co-investors and prudent financing,” the fund will acquire up to USD 100bn of assets, it said. “We’re seeing strong demand from institutional investors who want targeted exposure to this emerging asset class,” Brookfield’s head of Europe and Global AI Infrastructure Sikander Rashid told Infralogic.

Seeking scale

Scale was a major factor in Brookfield’s decision to launch the dedicated AI infrastructure fund, according to Rashid. “AI requires infrastructure delivered at such a great scale that it runs the risk of over-concentration in a traditional infrastructure or transition fund; AI infra in North America and Europe alone is a USD 7tn investment opportunity,” he told Infralogic. Scale is particularly relevant for Brookfield because it is according to Rashid targeting investments “across the full AI infrastructure value chain — from power and land through to data centres, cooling and chip manufacturing — where we can structure the assets around infrastructure-style contracts.”

This all-encompassing approach is important because AI infrastructure, while having much in common with more traditional data centres, includes new technologies that not all would see as meeting the usual criteria of infrastructure investors. At the centre of this difference are graphics processing units (GPUs), the sophisticated chips that perform the main AI tasks. These chips are overwhelmingly designed by Nvidia and are used to serve the big AI companies such as OpenAI and Anthropic, known as AI labs. Between Nvidia and the AI labs lie the buyers of the chips, which can include big tech companies such as Alphabet and Microsoft, but also “neoclouds” such as Coreweave and Lambda, whose main business model is to buy GPUs and then serve AI labs and other customers.

As relatively new players, both AI labs and neo-clouds do not have strong credit histories and are therefore not covered by ratings agencies or are rated as junk, like Coreweave with a B+ rating from S&P Global. This can create challenges for infrastructure funds used to either hosting such tenants in their data centres or, if they own all the equipment within the data centres, using this to serve investment grade customers.The Dutch bank NIBC, a major digital infrastructure lender, for example said in a recent report on AI infrastructure that it “will not currently finance a large AI facility that relies solely on a neocloud tenant as its anchor customer” noting that neoclouds have “very limited credit history”.

But, according to Rashid, “often a non-investment grade entity has partial or full support from a stronger investment grade counterparty”. To give some examples of non-investment grade entities supported by investment grade ones, neoclouds Coreweave and Lambda are both backed by Nvidia, while on the AI labs side Microsoft is a backer of OpenAI, and Anthropic’s shareholders include Nvidia, Amazon and Google. “The key point,” according to Rashid, “is whether the contract structure delivers long-term, take-or-pay cashflows with counterparties capable of supporting infrastructure-scale commitments.”

Radiant plans

Brookfield is addressing the AI infrastructure opportunity through Radiant, a BAIIF platform company, which is in its first few months of operation and has secured contract lengths in excess of five years. The Canadian manager took a major step in shaping its AI infrastructure when it in February announced the acquisition by Radiant of London-headquartered ORI Industries. Similarly to Coreweave and Lambda but on a smaller scale, ORI buys Nvidia GPUs and uses these to service technology companies’ AI needs. Despite their name, GPUs are used for a much wider range of functions than graphics, notably parallel processing, which involves carrying out multiple calculations and other functions simultaneously rather than sequentially. This capability is used to power chatbots, image recognition, self-driving cars and other applications.

As noted by Ori’s advisor on the deal, PwC, the transaction is “one of the first landmark deals bringing long-term infrastructure fund capital directly into the development and ownership of utility-scale AI factories.” AI factories are essentially data centres that host large clusters of GPUs, requiring vast amounts of power as well as water cooling rather than the air cooling that is sufficient for more traditional data centres. Folding ORI into Radiant, which according to its website has access to more than 45 GW of renewable generation capacity globally, helps it achieve its aim of acting across the AI infrastructure value chain, Rashid said. This power Radiant has access to is held through Brookfield’s other portfolio companies within its older funds, while BAIIF also has a USD 5bn framework agreement with onsite energy specialist Bloom Energy to install up to 1 GW of behind the meter power for data centres and AI factories. Brookfield is also pursuing its AI infrastructure strategy through Data4, a data centre company that also sits outside BAIIF.

But the manager ultimately intends to make Radiant a “fully integrated AI infrastructure platform” covering land, power, data centres and chip manufacturing. This is a step up from ORI, which prior to its agreed acquisition by Radiant did not operate its own data centres, but leased space in them. Brookfield’s acquisition of ORI means that it will rather than hosting neoclouds as tenants be performing the neocloud function itself, serving both investment grade major tech companies as well as non-investment grade AI labs. If other infrastructure investors follow Brookfield into moving into ownership of GPUs this will be an important step for the asset class. Brookfield, which sees the total investment opportunity for AI infrastructure totalling more than USD 7tn over the next decade, predicts that cumulative GPU sales will total USD 4tn over this period.

Government partnerships

While ownership of GPUs may seem like a leap in the dark for more conservative infrastructure investors, one area where NIBC in its report sees the potential for AI infrastructure to become more bankable for infrastructure lenders is through support from government. It notes that this could mirror “the evolution of offshore wind, where multi‑billion‑euro financings only became feasible once governments supported early‑stage risk.”

Working with governments is already a major part of Brookfield’s AI infrastructure strategy. Early in 2025, it pledged EUR 20bn (USD 23.2bn) of investment in AI infrastructure in France, this year increasing this to EUR 30bn, and plans SEK 95bn (USD 10.2bn) of investment in Sweden, both in partnership with the governments. Governments have yet to announce AI infrastructure subsidy programs comparable with those in offshore wind. But in an example of how Brookfield is working together with governments, its investment in France involves developing a data centre on a site in Escaudain that was earmarked by the French state for this purpose, with Brookfield being selected after a competitive process.

Viewing AI capabilities as matters of economic competitiveness and national security, governments will take an increasingly active role in supporting AI infrastructure development, according to Rashid. “We believe demand for sovereign AI platforms — where countries can keep their data, compute and critical infrastructure fully domiciled and secure — will be a major long-term driver of investment in the sector,” he told Infralogic.

Interestingly chip manufacturing – named by Rashid as one of the areas of AI infrastructure Brookfield would like to target – is also likely to be addressed through partnerships with governments. In a commentary last year, Brookfield identified semiconductor fabrication – meaning the actual production of semiconductors rather than their design – as one of the areas where private capital can combine with public money as governments look to “reshore” industrial capacity. Brookfield Infrastructure has experience in chip manufacturing, having in 2022 partnered with Intel to jointly fund the tech company’s semiconductor fabrication facility in Arizona.

Other AI strategies

Brookfield has been joined in launching an AI infrastructure fund by EQT, which announced its AI strategy in April. Like Brookfield’s this will target AI factories and involve raising a specific fund. Other big infrastructure funds, while not specifically launching AI infrastructure funds, have announced major AI infrastructure plans, notably Global Infrastructure Partners and its owner BlackRock, which in 2024 joined forces with Microsoft and UAE tech investor MGX to create an AI infrastructure investment partnership. As well as backing BAIIF, Nvidia and KIA are joining forces with KKR to fund an AI infrastructure platform company. Blackstone meanwhile is investing USD 5bn in a joint venture with Google to offer data centre capacity and services using the tech company’s Tensor Process Units (TPUs), which rival Brookfield’s GPUs.

While various funding models and partnerships are being adopted, a common theme is addressing the need for scale, which cannot simply be met by generalist infrastructure funds making lone investments in the sector. Funds devoted to AI infrastructure are an obvious way of creating this scale, and it is unlikely to be long before Brookfield and EQT are joined by others in launching them.

A service of

Shape your future with Infralogic. Today

Explore unlimited content like this, available only in the platform.

Already a client? Sign in