Antin’s Matawan investment pushes infra boundaries

Software fails to tick many of the boxes for typical infrastructure investments, but features such as recurring contracts and a lack of competition have attracted Antin to Matawan. Alexander MacLeod and Stefano Berra report.

Infrastructure funds have recently kept a close eye on technological disruption in the transport sector, both to fend off threats and embrace opportunities for their portfolio companies.

From electric vehicle charging to bike-sharing, and from vertiports to futuristic flying taxis, in the last few years infrastructure investors have made bets with varying degrees of success on the evolution of transport.

Antin Infrastructure Partners in September took this trend one step further with the acquisition of French mobility payment provider Matawan, effectively betting that software is becoming so ingrained in public transport systems that it will soon be considered as essential as roads, rail or buses.

The Paris-listed infrastructure fund manager announced on 4 September that it had agreed to buy an 80% stake in Mâcon-headquartered Matawan for its NextGen Fund I, whose mission is to invest in “businesses poised to become the next generation of infrastructure”.

Antin is set to invest around EUR 100m in the deal, a source familiar with the matter said, to buy shares from Matawan’s previous owners, including French investor Essling Capital, and inject new capital for growth.

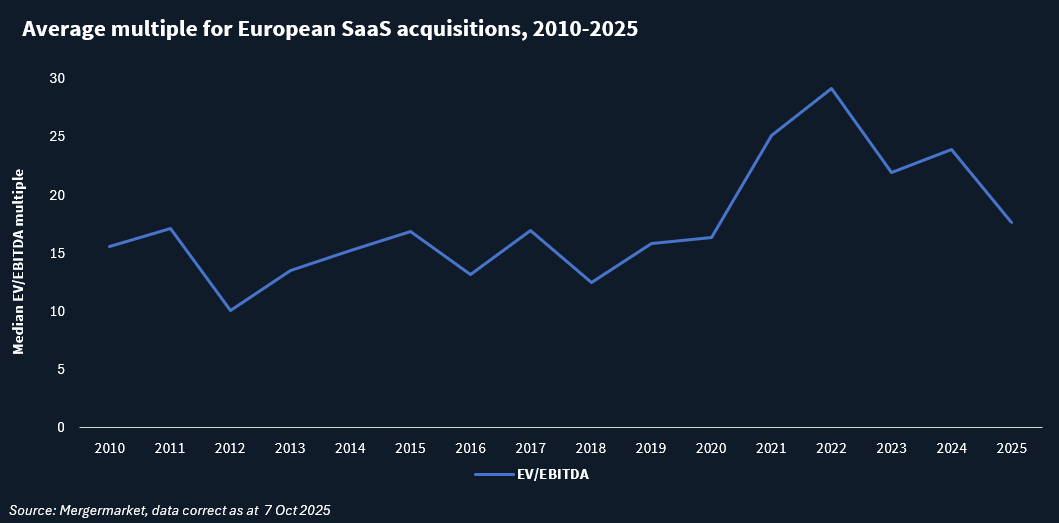

Matawan is known as a software as a service (SaaS) provider, mainly processing card payments by public transport users, including for the metro, buses, trains and even bike hire, for public municipalities and transport agencies.

Founded in 2012 and previously called Ubitransport, the firm employs around 300 staff and also offers real-time data and analytics services on transport network performance and location data for vehicles.

Software infrastructure

Antin partner Nicolas Mallet, who works on the NextGen strategy, says the firm saw infrastructure-like characteristics in Matawan because of its long-term, sticky contracts with public sector clients, which he describes as “evergreen” because customers tend to keep renewing them.

He adds that French public authorities are particularly risk averse and unlikely to want to change their transport setup for fear of upsetting the users, who are also voters.

High barriers to entry and a dearth of competitors in the same space were also important factors, according to Mallet.

The number of competitors able to offer a rival product is small, he says, and switching providers is challenging because of high software and hardware costs.

Matawan’s market penetration also provides comfort. Over a period of 10 or so years, the company has built up a broad client base including Keolis, RATP Dev and Transdev, as well as 12 French regions, including in overseas territories.

Antin’s love affair with software linked to infrastructure might just be getting started. Mallet says the fund has also considered investing in healthcare software, which he believes can in some cases be classified as infrastructure, for instance in the optimisation of critical medical systems for large hospitals and clinics.

All aboard for more growth

Antin’s peer InfraVia Capital Partners also recently invested in software companies focused on the transport sector, buying a majority stake in airport software provider Copenhagen Optimization last year. InfraVia however struck that deal through its growth fund, which targets early-stage digital companies, rather than specifically infrastructure ones.

While Antin’s NextGen fund is not taking risks on unproven technologies, high growth is a primary objective for its portfolio companies to achieve its mid-teen target returns.

Antin senior partner Nathalie Kosciusko-Morizet says transport authorities are increasingly adopting digital technology to help users switch between different modes of transport, and between different transport operators, within their networks.

This trend “will ultimately result in wide super-dominant adoption of the cloud-based system”, says Kosciusko-Morizet, who has experience of French public authorities’ thinking from her time as Minister of Ecology, Sustainable Development, Transport and Housing in the French government in the 2010s.

| Antin NextGen Infrastructure Fund I | ||

Investments to date: |

||

| Name | Location | Sector |

| SNRG | UK | Electricity Distribution |

| Raw Charging | UK | EV Infrastructure |

| Power Dot | Portugal | EV Infrastructure |

| PearlX | USA | Smart Grid |

| Uddevalla Tyre Recycling Plant | Sweden | Waste-to-value |

| GTL Leasing | USA | Hydrogen |

| Matawan | France | Transport |

More specifically, under Antin’s watch the business could seek to grow more outside France, including in the US, Canada, Spain, Italy and Switzerland, where it already has some operations.

The fund manager could also find bolt-on acquisitions, including targeting companies that provide adjacent data services.

Matawan has completed four acquisitions in as many years, which are helping to drive the company’s current “hyper-growth”, Mallet says.

The company’s revenues jumped from EUR 15m in 2020 to EUR 34m in 2022, according to public records. Sister publication Mergermarket reported that revenues from recurring contracts were around EUR 30-40m in 2024, with EBITDA standing at about EUR 10m.

“When you look at the size of the market, when you look at the different opportunities in front of Matawan, we really believe that this company has the right product at the right time, in the right market”, he says.

Not (yet) infra?

Despite Matawan’s promises, transport software is a long way from being seen firmly as an infrastructure asset, other infrastructure GPs privately say.

One fund manager with investments in transport shares Antin’s view on the “stickiness” of Matawan’s contract. “That does make sense to me to a certain extent, because if you have a public authority, they don’t want to change their system every year,” he says.

However, fast-paced innovation in the digital sector, which may give rise to cheaper or more convenient alternatives by well-funded giants such as Uber, is seen as one threat that could displace Matawan’s products. Software companies’ lack of hard assets is another, as it makes it easier to switch provider.

One infrastructure GP pointed to providers of digital services for cashless parking, which have struggled with high competition and difficult adoption, as a cautionary tale.

Infrastructure lenders might also be hard to convince. Mergermarket reported that Antin has turned to private credit fund Eurazeo to arrange financing for Matawan, structured on its annual recurring revenues (ARR) – a type of deal typical for SaaS companies rather than infrastructure assets. Antin declined to comment on this point.

Antin however may not have to prove Matawan’s infrastructure characteristics – or sell it to an infrastructure fund – to turn it into a successful investment.

Fellow value-add-focused infrastructure fund manager HIG Infrastructure last year put on the market its Spanish mobility company Eysa, which combined low-risk traditional car parking concessions with higher-growth “smart mobility” operations such as traffic monitoring and urban tolling systems.

The sale was aimed at infrastructure funds among possible buyers, but the company was ultimately bought by private equity firm Tikehau Capital.

This is because “the growth potential far outweighed the cost of capital play”, says one source familiar with that deal, meaning PE firms betting on further growth were prepared to pay a higher price than infrastructure funds looking for a more stable investment.

“The smart mobility trend that [Antin] are buying into is one I am super optimistic for,” says this source. “All the sectors are in growth mode. There are very good tailwinds.”

Antin’s Matawan investment may ultimately follow the same trajectory.

| “New infra” sectors profiled by Infralogic | |

| Vertical farming | Swiss Life AM’s “agricultural infrastructure” bet on vertical farms |

| Graphics processing units | GPUs could be infrastructure investors’ next AI frontier |

| Helicopters | The tailwinds behind infra investors’ move into helicopters |

| Aircraft leasing | Infra funds warm to aircraft leasing amid supply constraints |

A service of

Shape your future with Infralogic. Today

Explore unlimited content like this, available only in the platform.

Already a client? Sign in