Royal London deal set to transform Dalmore Capital

- Dalmore targets GBP 12bn assets under management by 2030, focusing on UK infrastructure

- Partnership with Royal London to tap UK defined contributions sector, GBP 500m investment committed

- Dalmore to increase deal sizes, expand team, and target larger investments

For a person who has devoted much of his professional life to rejuvenating UK infrastructure, Alistair Ray’s rail journey this week to Heathrow was something of a depressing trip. “What should have taken 40 minutes took two hours,” says Ray, CIO of Dalmore Capital, speaking on Monday (3 November) from a waiting room at London’s largest airport. But in the race to improve UK infrastructure there is room for optimism.

Several hours later, Royal London, the UK’s largest mutual life and pension firm, completed its takeover of Dalmore Capital for a sum rumoured to be around GBP 130m. Dalmore declined to comment on the price.

The acquisition effectively marks the beginning of a new start for Dalmore, which just over two years ago was languishing in the face of Covid and Brexit uncertainty as well as rising interest rates. The latter particularly impacted core to core-plus investors like Dalmore that targeted high single digit returns.

Matters reached a head in early 2023 when Dalmore halted fundraising for its fourth fund at some GBP 430m versus a GBP 1bn target and focused its efforts on asset management rather than investment.

Today, with the Royal London deal signed and delivered, Dalmore hopes in fairly short order to become the number one investor in UK infrastructure as well as ramp up its senior management, grow its deal sizes and double its assets under management to some GBP 12bn by 2030.

“We are now back replicating what we were doing pre-Covid time,” says Ray.

It hopes to achieve this by taking full advantage of its partnership with Royal London, while remaining razor-focused on investing in UK infrastructure – and, possibly, helping improving those rail links to Heathrow.

Dalmore, despite recent turbulence, starts from a position of strength, having built up an arsenal of some GBP 6bn of assets under management. It also has some 135 portfolio companies mostly in the UK, including stakes in the likes of London’s EfW giant Cory Riverside, the sprawling Thames Tideway Tunnel and rolling stock lessor Porterbrook. Its performance has been solid, too, with its four funds providing returns of 550bps-600bps over the 10-year gilt on the date the funds launched, says Ray. This is equivalent to a high single-digit return, in line with targets of core to core-plus investors prior to the recent interest rate hike, he adds.

| Fund name | Vintage | Length | Size |

| Dalmore Capital 4 | 2021 | 15 years | GBP 138m (430m including co-investments) |

| Dalmore Capital 3 | 2018 | 15 years | GBP 950m |

| Dalmore Infrastructure Investments | 2015 | 25 years | GBP 445m |

| PPP Equity PIP | 2015 | 25 years | GBP 534m |

| Dalmore Capital Fund | 2013 | 25 years | GBP 248m |

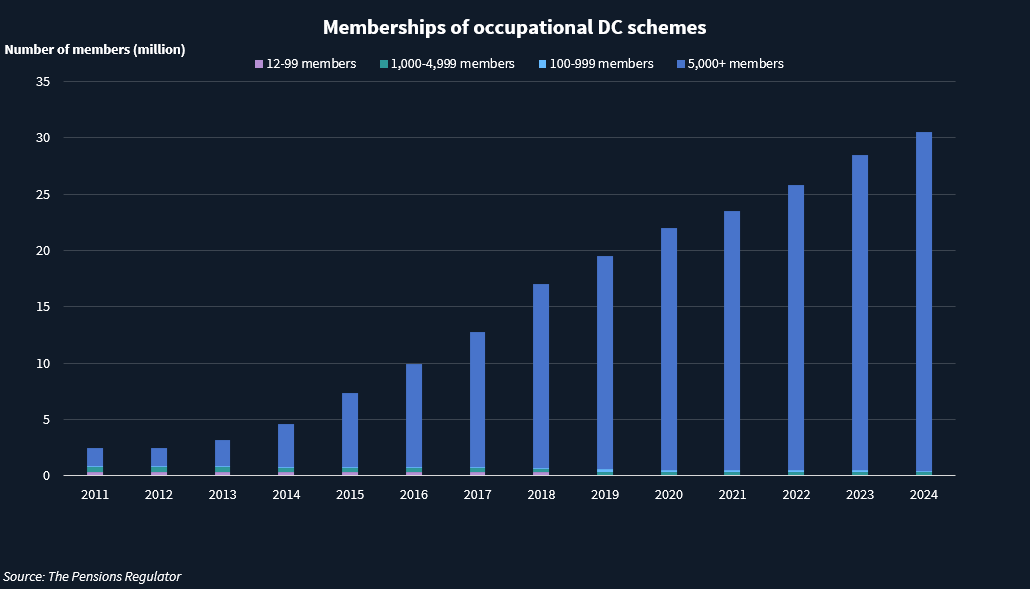

Tapping DC’s billions

But one major difference to before is its expected future sources of capital – and this is where its new partnership with Royal London comes into play.

When UK manager Dalmore Capital launched 13 years ago it sought to raise much of its capital from local authority and corporate defined benefit (DB) schemes in Britain. Today it hopes to turbocharge fundraising by tapping the UK’s defined contributions sector rather than Britain’s flagging DB market.

DC schemes involve employers guaranteeing pension contributions based on employees’ salary and years of scheme membership; while DB ones provide a guaranteed income for life based on salary and years of service.

The former are expected to flood the private infrastructure sector with capital in the wake of the government’s Mansion House Accord in May, when 17 of the UK’s largest DC workplace pension providers pledged to invest at least 5% of their assets in UK private markets, including infrastructure, by 2030.

Dalmore is on paper well placed to tap this DC market given its takeover by Royal London, which is both a major player in the UK’s DC sector and also one of the 17 pension providers to sign the Mansion House Accord.

“One of the real attractions for us in doing the deal with RLAM is getting access to one of the big players in the DC market,” says Michael Ryan, Dalmore’s CEO.

Royal London has already promised as part of its takeover of Dalmore to invest some GBP 500m into vehicles managed by the UK investor. Dalmore hopes that Royal London in reality will actually invest “multiples of the GBP 500m into Dalmore-managed vehicles,” says Ray.

This could in theory be just the start given Royal London is keen for Dalmore not to be a captive investment house but to continue to raise capital from third parties. This means Dalmore has almost free rein to tap other DC schemes, which crucially will potentially also be attracted to Dalmore given its pedigree as a UK-focused investor.

“We are spending a lot of time with DC schemes, not just Royal London,” says Ray, adding that “GBP 5bn from DC schemes into our funds would work well”.

Ryan points to “numerous DC schemes with ambitions to deploy upwards of GBP 2bn into infrastructure over the next three to four years”, although he adds that it is unlikely to engage with some competitors of Royal London, such as Aviva.

Dalmore’s deal with Royal London is reminiscent of Nest – another UK pension provider that also signed the Mansion House Accord – buying a 10% stake in IFM and agreeing to invest some GBP 5bn by the end of the decade in vehicles managed by the Australian investor.

Fundraising drive

Royal London has also made it clear that it wants Dalmore to go all guns-blazing to raise as much third party capital as it possibly can – and said it is committed to Dalmore operating as an stand-alone subsidiary under the umbrella of Royal London Asset Management (RLAM), Royal London’s investment subsidiary. The only exceptions are that RLAM’s CEO, Hans Georgeson, has a Dalmore board seat, while Royal London will have an observer on Dalmore’s investment committee.This means that as well as working with RLAM’s fundraising machine (both RLAM and Dalmore share some clients), Dalmore is also gearing up to tap LPs from across the globe as well as DCs ones at home.

It is also beefing up its own investor relations team, re-hiring its former executive Rob Styles, who has spent the last seven years at the placement agent Pareto Capital Advisors, as its head of fundraising. He works alongside Jamie Pritchard, who oversees Dalmore’s existing assets under management, say Ryan.

It is also looking to add additional senior hires to its investment team as part of a broader push to increase its number of staff by some 15 to around 40. This is around the number it had back in 2017 during its heyday while fundraising for its third fund, DCF 3, “when there was a big growth in the firm’s AuM”, says Ryan.

How to deploy the billions

All this begs the question where this potential splurge of new commitments will be directed to. Dalmore is currently pre-marketing its fifth fund, Dalmore Capital 5, which has a GBP 1bn target, of which some GBP 200m is expected to come from Royal London, sources said. Dalmore declined to comment on the fund.

Unlike Dalmore’s previous four funds, all of which had 25 or 15-year lives, DCF V will mature in 10 years. This is largely driven by the expectations of largely international limited partners that Dalmore is looking to raised capital from, says Ray.

In addition to seeking re-ups from LPs in South Korea, Japan, Canada, Europe and the UK, Dalmore is also looking to tap additional capital form the US and also for the first time from the Middle East.

Dalmore has hired Ashurst to advise on fundraising for DCF 5 and might hire a placement agent for fundraising markets it is less familiar with.

Much of the expected new capital is likely to be funnelled into coinvestment and managed accounts, for at least two good reasons. Roughly two-thirds of Dalmore’s GBP 6bn of assets under management has been in the form of coinvestment and managed accounts, with the rest fed into its four funds.

Also, managers of DC schemes tend to prefer to invest into long term vehicles. Therefore at least some of the expected commitments from Royal London and other DC schemes are likely to be rolled into coinvestments and managed accounts rather than into its shorter life funds.

Going for growth

Armed with such capital, Dalmore hopes to do larger deals of between GBP 100m and GBP 500m. It also wants to buy mainly controlling or co-controlling stakes, rather than minority stake deals in big assets, like its purchase of an 8% stake in UK gas utility Cadent.

It might also do a small number of deals in continental Europe, although typically via managed accounts and as part of a consortium, as it did in 2019 when it bought a stake in Barcelona metro’s system alongside Equitix, Brookfield and Iridium.

The extra firepower might mean it also has capacity to do more Thames Tideway style deals. It is currently preparing to vie for some large greenfield opportunities including, says Ray, for future Direct Procurement for Customers projects, mega water schemes around Britain; as well as OFTOs and the GBP 9bn Lower Thames Crossing, involving the construction of a new bored tunnel under the River Thames and new link roads.

Dalmore remains uncommitted on whether to launch further blind pool funds beyond DCF 5. “In reality we don’t know,” says Ray. “In two years things might come up around particular sub sectors around renewables or greenfield. But for now we focused on DCF V and looking at manged accounts in Europe.”

But what is clear is that by committing to still invest in the UK it is differentiating itself from much of the rest of the market. Other managers that have been bought by large financial institutions, which have used it as an opportunity to spread their wings and target new sectors and geographies. UK-headquartered InfraRed redirected part of its efforts on the United States when it was bought by SunLife in 2018, for example.

But keeping focused on one market gives it an edge over rivals, says Ray: “If people want to invest in the UK then they’re better off with us than a pan- European fund as we know the market, have better access and are not spread thin,” he says.

Focusing on the UK might also mean Ray’s next trip to Heathrow won’t take quite so long.

A service of

Shape your future with Infralogic. Today

Explore unlimited content like this, available only in the platform.

Already a client? Sign in