Wanda Commercial impacted by parent Wanda Group’s liquidity woes – Credit Report

Useful links:

- DWCM 1H23 interim report (Chinese)

- DWCM 2022 annual report (Chinese)

- DWCM CNY 1.5bn 6.8% due-March 2026 onshore MTN OC (dated 15-Mar-23) (Chinese)

- Zhuhai Wanda IPO prospectus (dated 28-Jun-23)

- Wanda Commercial’s strong credit profile weighed down by parent – Credit Report (9 February 2023)

[Excel model for DWCM’s historical financials and list of investment properties]

Dalian Wanda Commercial Management Group’s (DWCM) 1H23 results published on 31 August shows peculiar transactions that significantly drained its liquidity at a time when other parts of the Dalian Wanda Group have been under severe liquidity pressure.

Worryingly from a corporate governance perspective, Beijing-based, unlisted, shopping-mall owner and operator DWCM reported investing CNY 17.7bn (USD 2.4bn) in undisclosed financial assets in 1H23. That left it short of cash to redeem USD 400m (CNY 2.9bn), 6.875% due-23 July bonds as well as CNY 1.1bn onshore debt allegedly already due.

To fully repay the bonds, DWCM relied partly on the CNY 2.3bn (USD 310m) that Wanda Group raised from the sale of half of its minority stake in Shenzhen-listed cinema operator and film production house Wanda Film Holding.

DWCM disclosed in the 1H23 report that it was hit with a CNY 1.11bn recovery suit on 21 April from a non-banking financial institution over principal and interest. It adds that no court hearing date had been set as of end-August but doesn’t provide any other details on the claims or litigation.

DWCM has provided – and may continue to provide – cash to Wanda Group’s 50.3%-owned, unlisted, struggling property development arm Wanda Properties Group (WPG) through prepayments on property acquisitions. The mall owner and operator reported that in 2H22, it advanced CNY 11.6bn cash to WPG entities for the planned acquisition of undisclosed shopping mall properties that has yet to be consummated as of end-June. DWCM separately disclosed in its 1H23 results that it “plans” to acquire eight shopping malls – each in a different city – from WPG but doesn’t make clear whether these are the ones for which the advance was paid.

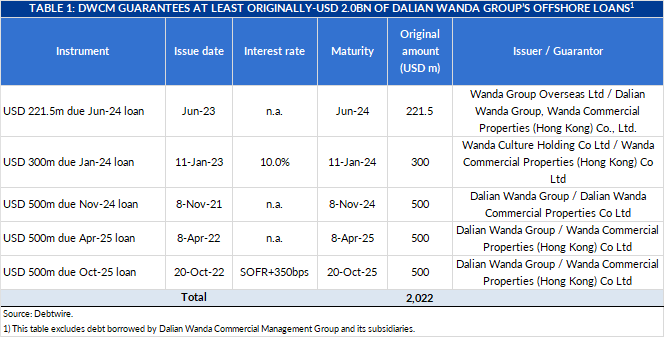

DWCM also provides guarantees on originally USD 2.0bn of Wanda Group’s offshore loans (see table 1), a significant amount compared to DWCM’s own USD 1.4bn offshore debt as of end-August, comprising three USD bond tranches.

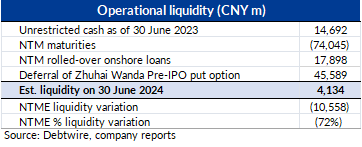

On paper, DWMC has sufficient cash and expected free cash flow generation to repay its own debt maturities through end-June 2024 if it is able to avoid needing to pay early next year as much as CNY 45.6bn to buy back shares of pre-IPO investors in 78.8%-owned unit Zhuhai Wanda Commercial Management Group. The pre-IPO investors have the right to put back to DWCM their 21.2% stake in shopping-mall manager Zhuhai Wanda if it is not listed by yearend.

Debtwire first reported in late-May that the company was in talks with the pre-IPO investors to delay by two years their put option (see section on Zhuhai Wanda IPO).

DWCM Liquidity

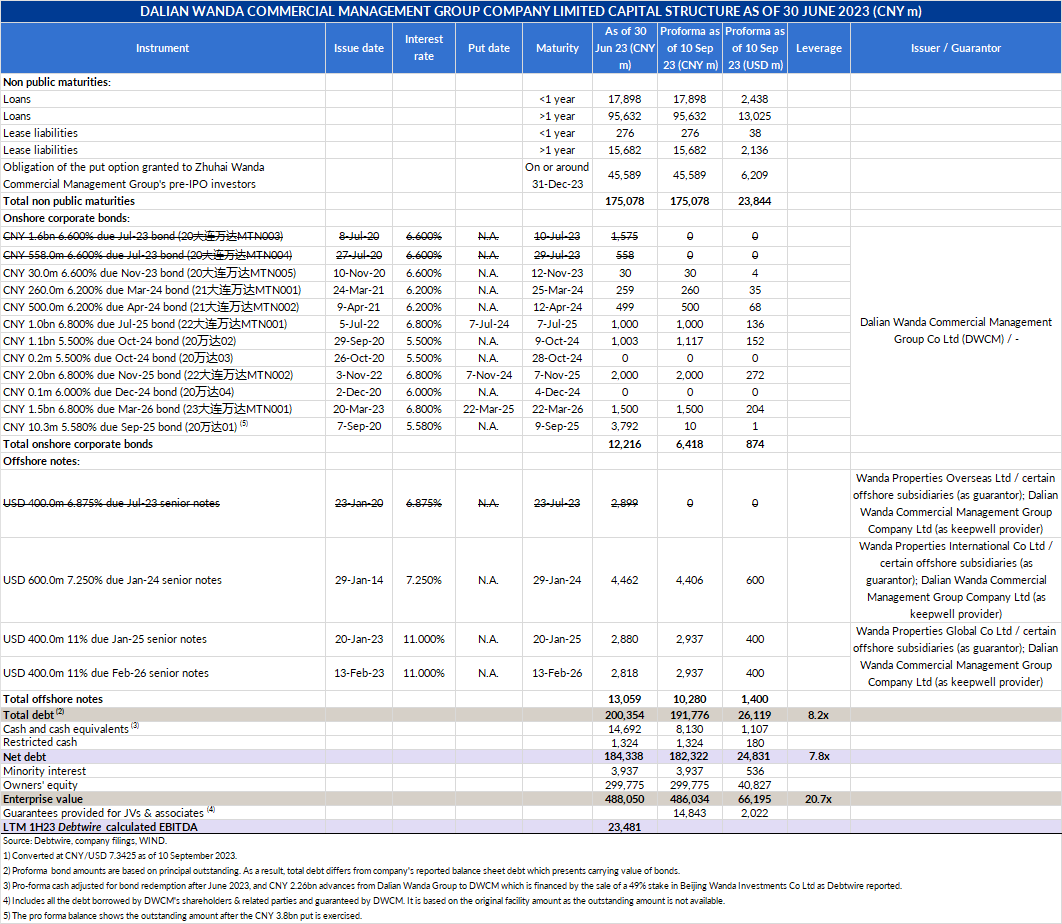

DWCM has CNY 8.1bn pro forma cash (adjusted only for financing) and is expected to generate CNY 15.7bn free cash flow in the twelve months through June 2024 from property management revenues and rental income from its mature portfolio of 473 operating Wanda Plaza shopping malls, per Debtwire estimates (see the 2nd bullet point for pro forma adjustments). That liquidity is more than enough to cover the shopping-mall owner and operator’s CNY 5.2bn hard debt maturities through June next year, comprising USD 600m, 7.25% due-29 January 2024s and CNY 790m onshore bonds across three tranches due between November 2023 and April 2024.

DWCM’s liquidity is also sufficient to cover the CNY 17.9bn in mostly secured onshore bank loans due by end-June although these should be easily refinanced or extended because of the sector-wide support measures Chinese authorities announced on 10 July. Under the measures jointly announced by the People's Bank of China and the National Financial Regulatory Administration, financial institutions are encouraged to extend by one year any domestic loans due by end-2024 owed by developers, including trust loans; lenders are given the flexibility to refrain from classifying the extended loans as problematic.

Despite sufficient liquidity to meet all its own near-term debt obligations, DWCM has been trying – albeit, with limited success – to raise funds from selling down its portfolio of Wanda Plazas. As recently as May, the company was in talks with several parties about potentially disposing 20-30 malls via a structure that would require it to buy back the malls if certain operating income targets were not met, per a 13 June Debtwire article. In June, DWCM already sold for “a bit more” than CNY 2bn three shopping malls to state-owned life insurer Dajia Life Insurance via a transaction that was in “some way actually debt disguised as equity”, per the Debtwire article.

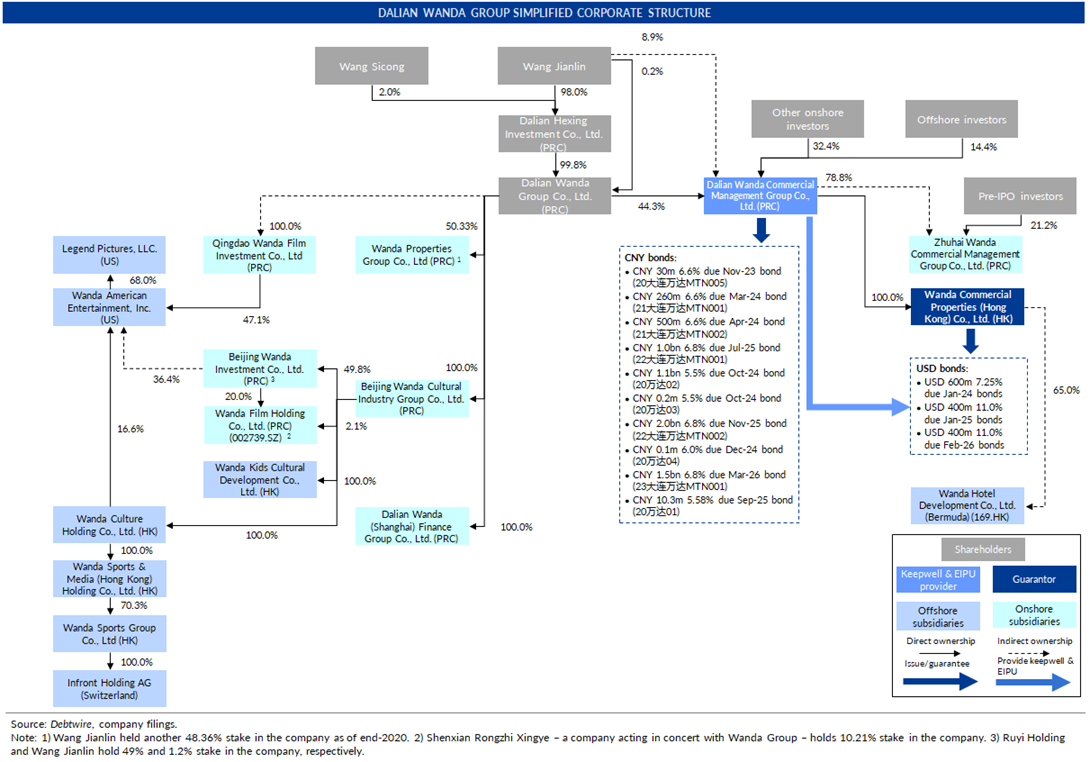

Group Chairman Wang Jianlin controls an effective 53.3% stake in DWCM, including a 44.3% held by his family’s wholly owned Wanda Group (see bottom of this report for a simplified corporate structure of Wanda Group).

Liquidity of rest of Wanda Group, including WPG

While Wanda Group hasn’t publicly released financials since 2020, there have been multiple public filings so far this year showing that the conglomerate – in particular WPG – is experiencing a liquidity crunch.

WPG, which is 50.3% owned by Wanda Group, has been on the Shanghai No.2 Intermediate People’s Court’s “dishonest-debtor list” since April, after failing to settle CNY 1.09bn across two claims related to a contract dispute for a project in Heyuan City, Guangdong Province.

A 1.2% stake in DWCM held by Wanda Group has been frozen by Shanghai and Dalian courts, per Chinese corporate information database Qichacha on 12 September. The database isn’t clear about how that freeze relates to a Shanghai court’s 5 June freeze of a 43.7% DWCM stake held by Wanda Group. The larger freeze was at behest of Changchun, Jilin province project joint venture partner China Vanke – one of the country’s largest developers – which had been seeking more than CNY 1bn from WPG. That dispute was settled in late July and the stake was to be unfrozen “soon”, Cailian Press reported on 27 July.

The root cause of WPG’s liquidity woes is likely because of slow sales of its property projects. While the unlisted WPG doesn’t publicly disclose its landbank, Chinese real estate information provider CRIC show that its landbank has sizeable exposure to tier-3 or lower cities in Gansu and Jilin provinces, which are among the worst performing regions and city tiers in terms of new homes sell-through rates. Indeed, the YoY decline for WPG’s contracted sales for the eight months to end-August was nearly twice as bad as the aggregated contracted sales of the 29 high-yield-bond-issuing developers (excluding WPG) that still provided comparative monthly data, as monitored by Debtwire’s China HY property tracker. WPG’s 8M23 contracted sales plummeted 65% YoY to CNY 12bn, per data compiled by CRIC, a significantly higher decline compared to the 37% YoY fall for the cohort of 29 developers.

Wanda Group has in recent months been working to dispose of its Australian-based cinema business Hoyts Group and European sports marketing business Infront Sports & Media AG, most likely to raise cash to cover looming debt payments.

Zhuhai Wanda IPO no panacea

The Zhuhai Wanda IPO, even if it receives the requisite regulatory approvals in the next few months, is unlikely to raise any cash for DWCM any time soon, never mind Wanda Group. The shopping-mall operator, being Zhuhai Wanda’s controlling shareholder, is not allowed to dispose of or pledge any shares until six months after the shopping-mall manager’s IPO, per Hong Kong’s Listing Rules. Even when DWCM is eventually able to sell Zhuhai Wanda shares, the amount raised from such sales will be nowhere near what it was expecting only two years ago.

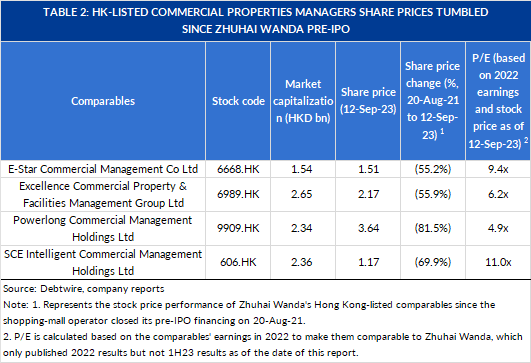

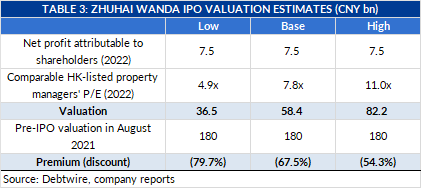

If the share price performances of peers are any guide, Zhuhai Wanda’s current market valuation should be only CNY 36.5bn-CNY 82.2bn, or 50% to 80% lower than the August 2021 CNY 180bn pre-IPO valuation cited in the listing prospectus (see table 2 for trading multiples of Hong Kong listed mainland Chinese commercial property managers and table 3 for Debtwire’s estimates for Zhuhai Wanda IPO valuation).

Key takeaways from DWCM’s 1H23 interim report released on 31 August and other recent developments:

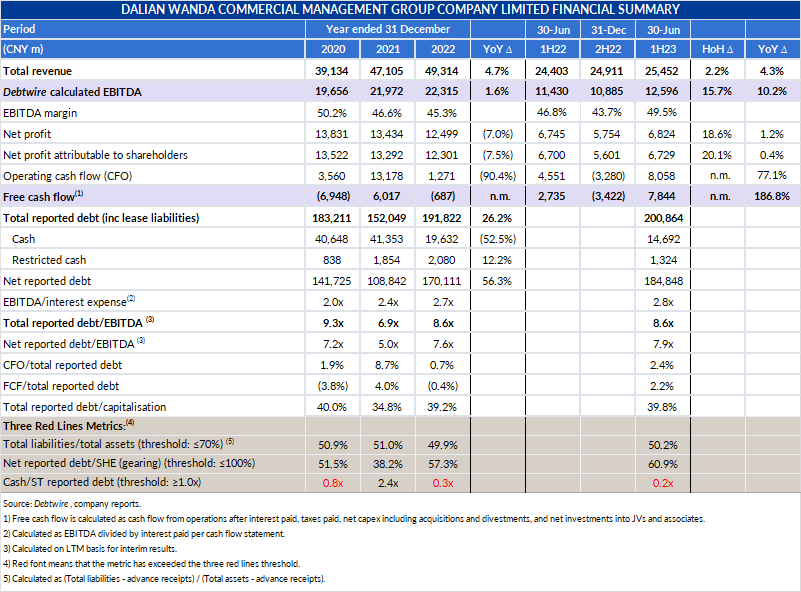

- Even while struggling with liquidity, DWCM’s financial assets oddly increased by 35.4% HoH / 15.9% YoY to CNY 66.3bn as of end-June, from CNY 49.0bn as of end-2022 and CNY 57.2bn as of end-June last year. The end-June balance comprised CNY 43.4bn “financial assets held for trading” and CNY 22.9bn “financial products”, per its interim report.

- It had pro forma unrestricted cash of CNY 8.1bn and pro forma total debt of CNY 191.8bn, per Debtwire calculations. Pro forma cash and debt were calculated by adjusting reported end-June balances for the following: 1) repaid CNY 5.9bn maturities and puts across three onshore bond tranches; 2) repaid at maturity USD 400m (CNY 2,9bn) due-23 July offshore bond, and 3) received CNY 2.3bn cash from its parentco’s sale of the 9.8% stake in Wanda Film Holding.

- Its pro forma debt stack comprises CNY 113.5bn secured loans, CNY 45.6bn Zhuhai Wanda pre-IPO investor buyback obligations, CNY 16bn lease liabilities, CNY 10.3bn offshore bonds and CNY 6.4bn onshore bonds.

- Unrestricted cash plummeted 48.2% QoQ and 25.2% HoH to CNY 14.7bn as of end-June, from CNY 28.3bn as of end-March and CNY 19.6bn as of end-2022.

- Total debt was CNY 200.9bn as of end-June, down from CNY 204.4bn as of end-March and up from CNY 191.8bn as of end-2022.

- DWCM reported CNY 459.1bn book value of investment properties as of end-June, of which CNY 343.0bn were encumbered, implying a loan-to-value (LTV) of 33%. Secured loans – most backed by its shopping malls – was CNY 113.5bn as of end-June, up 5.2% compared to CNY 107.9bn as of end-December (see the tab ‘investment properties’ in the attached spreadsheet for a full list of Wanda Commercial’s self-owned investment properties as of end-2022).

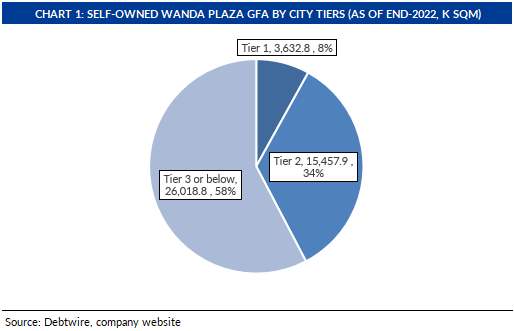

- DWCM’s corporate website shows that it owned and or operated 473 Wanda Plaza-branded shopping malls with total GFA of 65.6m sqm as of end-2022 (latest publicly available figure). Of the 473, it owned and operated 310 with total GFA of 45.1m sqm while it only operated the remaining 163 third-party owned malls. Tier-3 or lower, tier-2 and tier-1 cities accounted for 58%, 34% and 8%, respectively, of the company’s total owned and operated GFA as of end-2022 (see chart 1 below).

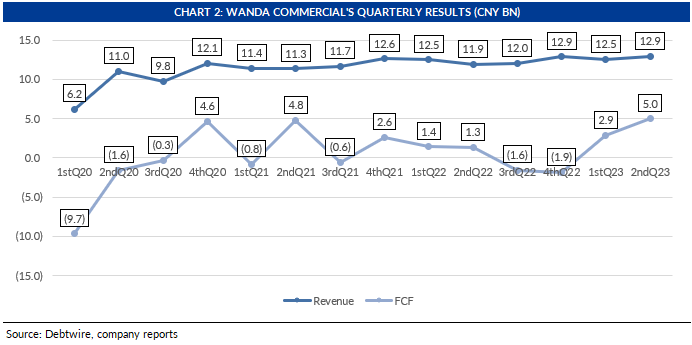

- The company generated positive CNY 7.8bn free cash flows (FCF) in 1H23 compared to negative CNY 3.4bn in 2H22 and positive CNY 2.7bn in 1H22. Revenues – comprising rental income and management fees – was CNY 25.5bn in 1H23, up 2.2% HoH / 4.3% YoY (See chart 2 for quarterly revenues).

- DWCM paid out CNY 4.5bn and CNY 4.8bn dividends in 2021 and 2020, respectively. The dividend payout ratio calculated on the previous full year earnings was 33% and 19% in 2021 and 2020, respectively. The company didn’t distribute any dividends for 2022.

A service of

Start your trial. Today

Explore unlimited content like this, available only in the platform.

Already a client? Sign in