UK and Germany continue as main drivers of restructuring activity, retail and real estate most stressed sectors – 2023 European Restructuring Insights

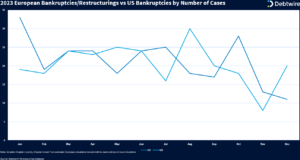

Debtwire’s Restructuring Insights report series provides a high-level overview of restructuring situations, digging deep into data available in Debtwire’s Restructuring Database (RDB) to highlight key trends and takeaways. This edition reviews newly commenced large-cap insolvencies and restructurings in Europe during 2023 with a record 254 restructurings tracked by the RDB, a 46% increase from 2022 (174), and marginally higher than the 245 US Chapter 11 bankruptcies tracked in the RDB during 2023.

The UK and Germany continue the 2022 trend of being the main drivers of EU restructuring activity, increasing their share of EU restructuring activity in the RDB to 61% from 50% (split UK with 35% (2022 – 25%) and Germany tracking the same as 2022 with 25%. France was the next busiest with 8% (2022 – 12%) and the Netherlands, Italy and Spain (‘the big six’) accounting for 5% each, respectively. In total, the big six represent 84% of large-cap restructurings commenced in 2023 verses 82% in 2022.

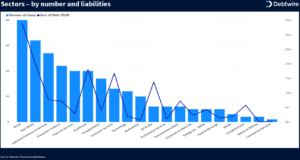

The leading sector again was retail with 40 situations, a 54% increase from 2022 which saw 26 situations, followed by real estate with 32 situations and industrial products & services with 27 situations. Retail also led pre-restructuring liabilities with EUR 33.8bn (23% of all sector pre-restructuring liabilities), with apparel & clothing accounting for 50% of that amount (EUR 17.5bn in pre-restructuring liabilities), followed by real estate (EUR 20bn in pre-restructuring liabilities), healthcare (EUR 18bn in pre-restructuring liabilities) and consumer services (EUR 16.7bn in pre-restructuring liabilities).

The number of situations where amend & extend (A&E) was one of the main restructuring financing featured was 44, a 63% increase on 2022 (27) and close to the peak of 48 A&Es in 2020. The number of debt equitisations remained the same YoY with 24 whereas the number of distressed debt exchange / reinstatements increased YoY to 25, 47% higher than 2022.

There was an 85% increase YoY in the number of scheme of arrangements and restructuring plans that came through the English courts with 24 compared to 13 in 2022. The number of Restructuring Plans nearly tripled YoY from five to 14 in 2023, whilst the number of schemes increased 25% from eight to 10.

The most active financial advisor/investment banker (FA/IB) tracked was Houlihan Lokey with 24 representations followed by PJT Partners with 19, PWC with 16, and Lazard and Rothschild with 15 each. Kirkland & Ellis was again the most active legal advisor with 25 representations followed closely by Latham & Watkins with 24, Linklaters with 20 and Freshfields with 19. In terms of creditors, HSBC was the most active lender/bondholder, followed by GLAS (as agent/security agent and/or trustee), Santander, Barclays, BNP Paribas and Credit Suisse. Carlyle was the leading investment fund, followed by Bain, Blackrock, Man /GLG and Sculptor.

Click here to explore the Restructuring Data platform (access required).

A service of

Start your trial. Today

Explore unlimited content like this, available only in the platform.

Already a client? Sign in