Telesat 1Q23 results meet expectations; financing for LEO remains up in the air – Credit Report

TSAT Investor Presentation December 2021

Overview: Satellite operator Telesat (TSAT) reported 1Q23 results that met expectations with lower revenue and adjusted EBITDA, but the company still generated free cash flow, and left FY23 guidance in place. With direct-to-home (DTH) renewals occurring at lower rates, TSAT is looking at declining FY23 revenue and adjusted EBITDA from its geosynchronous (GEO) satellite services business (15 geostationary satellites), thus making the transition to low earth orbit (LEO) satellites that much more important. Currently, TSAT has been unable to secure financing of its LEO program, called Telesat Lightspeed, partially due to supply chain issues at equipment contractor Thales Alenia Space, and inflation that have raised the cost of the program leading to an expected downsized constellation from the original 298 satellites planned. This delay has placed TSAT behind companies like SpaceX, with its Starlink network of satellites, and OneWeb which already have operating LEO satellites. Even if financing is secured soon, the company would not realize any revenues or cash flows from the program until after the earlier launch date in 2026. With minimal capex spending for the LEO program, during 2Q23 TSAT used cash to repurchase debt in the open market at a substantial discount to par. Due to completing the relocation of customers to free up spectrum, the company is expected to receive USD 260m in clearing payments by October 2023. Thus, we expect the company to make additional debt repurchases during FY23.

The company reports in three segments:

Broadcast (46% of LTM revenue) – Direct-to-home television, video distribution and contribution, and occasional use services. This segment has experienced declining revenues as customers are experiencing lower demand as users switch over to streaming services. Typical customers in North America include Bell TV, Shaw Direct, DISH Network, Bell Media, and NBC Universal.

Enterprise (53% of LTM revenue) – Telecommunication carrier and integrator, government, consumer broadband, resource, maritime and aeronautical, retail, and satellite operator services. Typical customers include Bell Canada, Hughes Network Systems, iForte, Marlink, Viasat, Vodafone, and Xplore.

Consulting (1.5% of LTM revenue) – services related to space and earth segments, government studies, satellite control services, and research and development. Typical customers have included Airbus, EchoStar, Lockheed Martin, Mitsubishi Electric, The Defense Advanced Research Projects Agency (DARPA), and Viasat.

The competitive landscape remains challenging with top rivals being SES SA, Intelsat, Viasat (Inmarsat), SpaceX (Starlink), Eutelsat, OneWeb, and Amazon’s Project Kuiper (planned LEO). Some announced combinations have not occurred, but Viasat and Inmarsat completed their USD 7.3bn merger in May. The combined entity has 19 satellites in orbit including 12 operating in Ka-band.

The satellite business can be quite risky as highlighted recently when a new geostationary Viasat communications satellite (VisSat-3 Americas) launched in April was unable to unfurl its antenna jeopardizing the viability of the satellite. According to a story in Ars Technica, if the satellite is written off as a total loss, it was reported that the USD 420m insurance claim still would not cover the USD 700m cost of the mission. In addition, such a claim could lead some insurers to exit the market. Covenants in TSAT’s debt agreements require the company to maintain insurance on its GEO satellites.

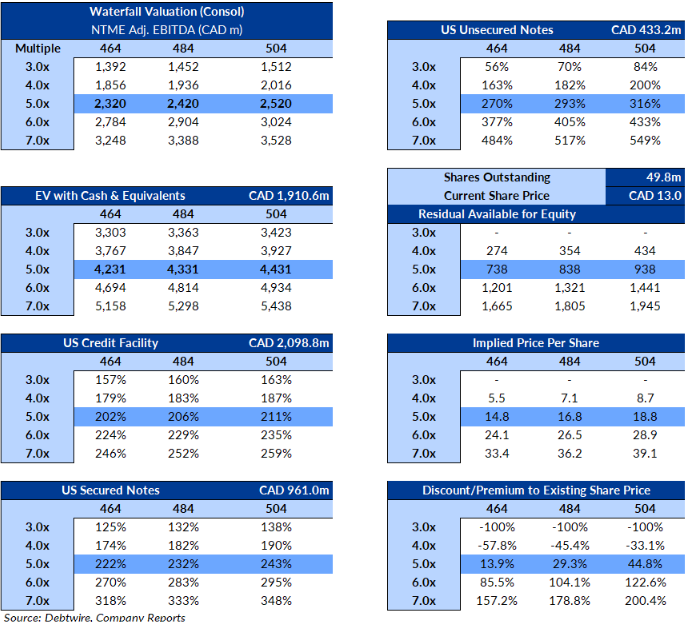

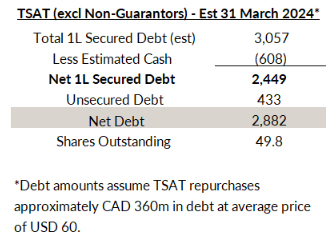

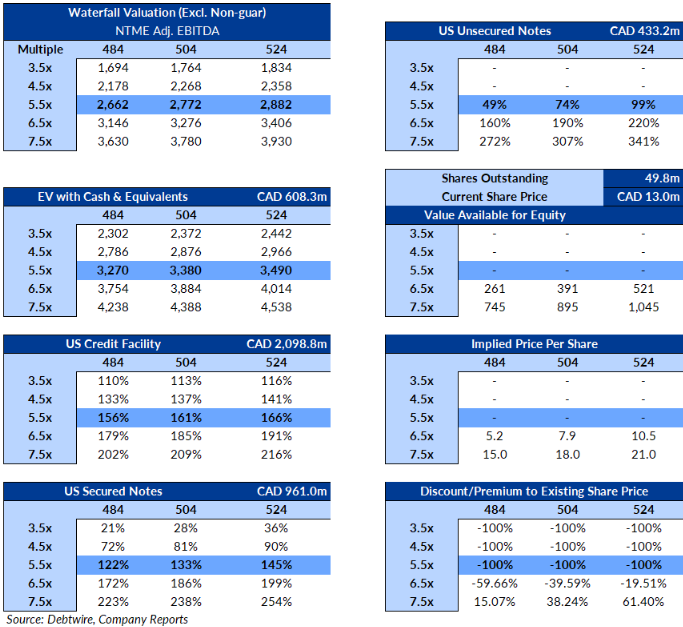

On a valuation basis, we looked at TSAT on a consolidated basis, and excluding its non-guarantor subsidiaries. On a consolidated basis, at our midpoint multiple and adjusted EBITDA estimate, we find that all debt is fully covered with an equity price of CAD 16.81 compared to the current price of CAD 13. When we exclude the non-guarantor subsidiaries, at the mid-point we find all secured debt is fully-covered with the unsecured notes valued at 45%.

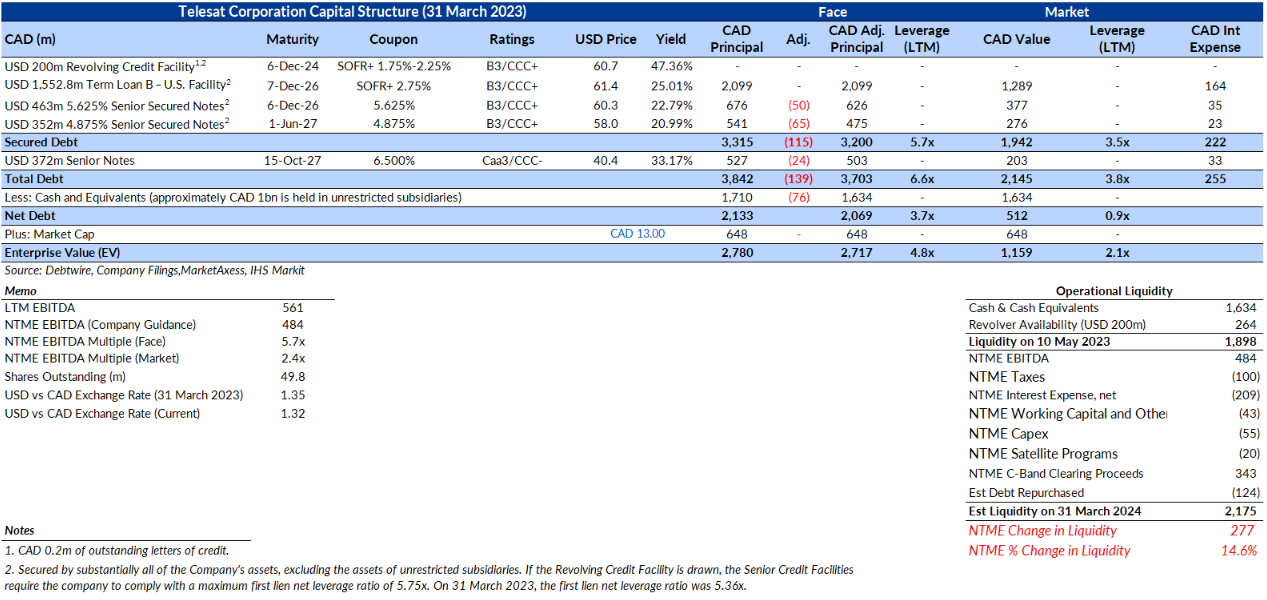

Liquidity, Debt and Cash Flow

On 31 March 2023, TSAT had CAD 2bn of liquidity, basically flat with 31 December 2022 liquidity of CAD 1.95bn. Of the CAD 1.7bn in cash, approximately CAD 1bn is held in unrestricted subsidiaries. The company had CAD 3.3bn of secured debt (USD 2.5bn) and CAD 527m of unsecured notes (USD 390m), all denominated in US dollars. At the end of 2022, if the value of the Canadian dollar increased CAD 0.01 against the USD, indebtedness would decrease by CAD 28.4m.

TSAT’s revolver, term loan B, and senior secured notes are secured by substantially all of Telesat Canada’s assets, excluding those in the unrestricted subsidiaries, and are guaranteed by the company and certain of its existing subsidiaries. The obligations are secured by first-priority liens and securities interests in the assets of Telesat and its guarantors. On 31 March 2023, for covenant purposes, Telesat’s total consolidated debt was CAD 3.7bn, and its total secured debt was CAD 3.2bn, both include up to USD 100m of net cash (CAD 135m). There is no amortization of the term loan because TSAT already made repayments through maturity.

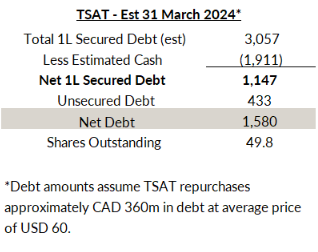

TSAT’s board authorized up to CAD 200m in cash for debt repurchases, if and when managemnt determines that repurchases are in the best interest of the company. From 1 April 2023 through 10 May 2023, Telesat repurchased in the open market USD 103.1m of notes for a cost of USD 56m (average price of USD 54). Due to estimated FCF generation, we project that the company will complete CAD 200m in debt repurchases over the NTM period.

On 31 March, TSAT reported LTM adjusted EBITDA of CAD 561m resulting in net secured leverage, net leverage, and total leverage of 2.9x, 3.8x, and 6.8x, respectively. For covenant purposes, Telesat’s LTM consolidated EBITDA was CAD 600m. The revolver was undrawn, but if more than 35% of the revolving credit facility is drawn, Telesat must comply with a first lien net leverage ratio of 5.75x. On 31 March, the first lien leverage ratio for covenant purposes was 5.36x and the total leverage ratio was 6.24x, which was more than the maximum test ratio of 4.5x, which limits any additional debt to the balance sheet.

For 1Q23, cash flow from operations (OCF) was CAD 62.6m compared to CAD 43.4m for 1Q22 and CAD 67.8m for 4Q22. Free cash flow (FCF) was CAD 37.7m, after CAD 25m of spending on property and equipment plus payments to satellite programs, compared to CAD 25.4m for 1Q22 and CAD 49.5m for 4Q22.

For NTME, we project that on a consolidated basis TSAT will generate CAD 277m of free cash flow that includes the company receiving CAD 343m (USD 260m) in C-Band clearing proceeds and allocating CAD 125m of debt repurchases, in addition to the CAD 76m spent from 1 April-10 May.

We further estimate for the NTM period, Telesat, excluding its non-restricted subsidiaries that carry no debt and over CAD 1bn of cash, will burn CAD 15m of cash (including the debt repurchases).

On the FY22 earning call, Daniel S Goldberg, President, and CEO of Telesat, stated that the company could bring back cash from its unrestricted subsidiaries, which would be important when valuing the company. “So – but, yeah, to your point, could we bring cash back? Yeah, we could. There’s nothing – I’m staring at our General Counsel. There’s certainly nothing that prevents us from doing that. We’ll cross that bridge if and when we get there.”

LEO and C-band Spectrum

TSAT secured a license from the Government of Canada (GoC) to launch and operate a low-earth orbit (LEO) satellite constellation using 4 GHz of Ka-bank spectrum for which TSAT has international spectrum rights. Telesat Lightspeed, a proposed constellation of LEO satellites and integrated terrestrial infrastructure to serve the enterprise and government market, has strong support from the GoC that includes an anchor contract that is believed to approximate CAD 1.2bn in revenue over 10 years, that includes CAD 600m from the GoC. The Government of Ontario (GoO) purchased a dedicated Telesat Lightspeed pool to be made available at substantially reduced rates to Canadian Internet services providers, and mobile network operators, which is believed to result in over CAD 200m in revenue over a five-year term, which includes CAD 109m from the GoO.

In 2021, TSAT reached an agreement in principle with the GoC for CAD 1.44bn of long-term funding and entered into a memorandum of understanding (MOU) with the Government of Quebec for an investment of CAD 400m. TSAT has been waiting for export credit agency (ECA) financing of approximately CAD 3bn. The original capex investment cost of TSAT Lightspeed was CAD 6.5bn (USD 5bn) to launch 298 satellites. The company, which thought that it would have more clarity on Lightspeed’s financing by year end 2022, is still in discussions with funding sources to cover the increased cost of the program, with the possibility of equity funding. If TSAT were to secure financing soon, the earliest it could start launching is in 2026.

TSAT has contracted for a LEO 3 satellite as a follow on to the LEO 1 satellite to provide additional capability for in orbit demonstrations in Ka-band and in non-geostationary orbit (NGSO) V-band.

The company also has rights to use C-band spectrum, critical for 5G. This spectrum is subject to regulatory proceedings in the US, where TSAT was awarded USD 344m in accelerated clearing payments, USD 84.8m (CAD 108.5m) of which has already been received. The company completed the requirement for relocating customers six months in advance of the the December 2023 deadline and is expected to receive its second accelerated relocation payment of nearly USD 260m by October 2023.

FY23 Guidance

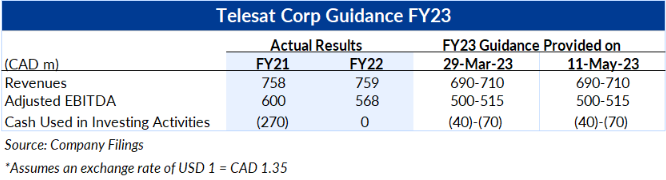

TSAT provided FY23 guidance for three metrics, as shown below. Approximately 50% of the anticipated decline in revenue and adjusted EBITDA is expected to come from (1) DISH’s Anik F3 renewal affecting the first four months of the year, and (2) the renewal for Bell Canada’s DTH capacity on Nimiq 4, but at a materially lower rate than the current one. The contact expires in October 2023 and was renewed for a two-year term. Of the remaining decline, the DARPA contract (CAD 20m) accounts for another 25% or so.

The company stated that expected FY23 cash flows for investing will be updated once it has greater visibility around the construction and financing of the Telesat Lightspeed program, but the range of CAD 40m-CAD 70m will increase substantially once the program gets fully underway.

Foreign exchange rates will effect TSAT’s reported results. In 2022, 54% or revenue, 37% of operating expenses, 100% of interest expense, and a majority of capex were denominated in US dollars.

Backlog

On 31 March 2023, TSAT’s contracted revenue backlog was CAD 1.7bn for its GEO business representing 2.2x LTM revenue. This is down from CAD 1.8bn on 31 December 2022 and CAD 2.1bn on 31 December 2021. All of the company’s backlog is non-cancellable or cancellable on economically prohibitive terms, except in the event of a continued period of service interruption. The company expects backlog to be recognized as follows:

Remainder of 2023: CAD 439m 2026: CAD 197m

2024: CAD 388m 2027: CAD 129m

2025: CAD 262m Thereafter: CAD 282m

On the company’s year-end earnings call in March, TSAT said that it had approximately CAD 750m worth of backlog for its Lightspeed (LEO) program.

Valuation for Consolidated Entity

For our valuation scenario, we estimate NTME consolidated adjusted EBITDA of CAD 484m, and a range of EV/adj EBITDA multiples from 3x-7x. At the midpoint, we find that all of the company’s debt is fully covered with an equity price of CAD 16.8 compared to the current stock price of CAD 13. We note that we have assumed that TSAT repurchases approximately CAD 350m of notes at an average price of USD 60.

Valuation for Telesat excluding Non-Guarantor Subsidiaries

Since a significant amount of cash is held in unrestricted subsidiaries, the latter of which generate slightly negative adjusted EBITDA, we have also provided a valuation of TSAT excluding its non-restricted subs. In this valuation, we used a slightly higher EV/EBITDA multiple range, 3.5x-7.5x, and at the midpoint, we find that all secured debt is fully covered, but that the company’s unsecured notes have a 74% recovery. If we include a 5% reorganization fee, the recovery for the unsecured notes drops to 42%.

The Details

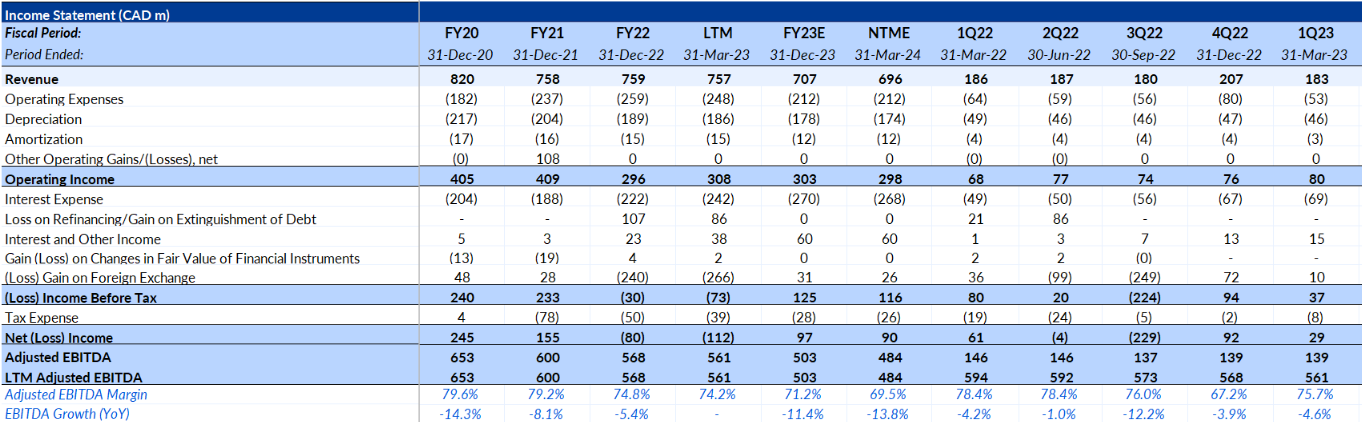

For 1Q23, TSAT reported revenue of CAD 183m, down 1.3% YoY, but when adjusting for changes in exchange rates, revenue dropped 5% (CAD 9m). For the quarter, Broadcast revenues fell 11.8% YoY to CAD 85.6m, Enterprise revenue jumped 11.3% YoY to CAD 95.1m, and Consulting revenues dropped 18.5% YoY to CAD 2.8m. Sequentially, total revenue dropped 11.3%, although 4Q22 results benefited from the completion of an equipment sale to DARPA of CAD 20m. Excluding this sale, revenue would have fallen about 1.8% sequentially.

The decline in Broadcast revenue was primarily due to a reduction from DISH due to the renewal on the company’s Anik F3 satellite at a lower rate and less capacity than the previous deal. This renewal will remain a headwind for 1H23. The increase in Enterprise came from higher equipment sales to Canadian government customers combined with increased services provided to aero and maritime customers.

At 31 March 2023, TSAT’s fleet utilization was 88%, down slightly from 89% on 31 December 2022. Utilization included the removal of Anik F2, due to a shortened life, and the inclusion of Anik F4.

On an LTM basis, 80.8% of revenues were from North America with Canada and the US accounting for 44.6% and 36.2%, respectively. EMEA, Latin America, and Asia Pacific accounted for 4.9%, 7.9%, and 6.4%, respectively.

For 2022, TSAT’s top five customers accounted for 60% of revenues, and on 31 December 2022, its top five backlog customers accounted for 81% of backlog. For 2022, approximately 82% of revenues were from North America customers, with 45% of revenue derived from North American DTH television service customers under long-term contracts (15 years).

Reported operating income was CAD 80.2m, a 17.3% YoY increase, which was primarily due to higher non-cash share-based compensation recognized during 1Q22. Excluding this non-cash expense, reported operating income would have fallen 13%. For the quarter, reported operating expenses fell CAD 11m from 1Q22. The reported operating margin increased to 43.7% from 36.8%. Excluding the non-cash shared-based compensation expense during 1Q22, the operating margin would have been 49.8%.

Adjusted EBITDA for 1Q23 was CAD 139m (75.7% margin), which was flat with 4Q22 of CAD 139m (67.2% margin) but lower than CAD 146m (78.4%) for 1Q22.

It is worth noting that as of 31 March 2023, intangibles and goodwill represent 49.2% of consolidated total assets which are supported by the planned Lightspeed constellation. If this program is delayed further or discontinued, TSAT would take a large impairment charge. Furthermore, of the CAD 2bn of assets held in non-guarantor subsidiaries, CAD 1bn is cash and cash equivalents, CAD 469m are satellites, property and equipment, and CAD 526m are intangible assets.

Business Description: Telesat is a leading global satellite operator providing its customers with mission-critical communications services through advanced satellites and ground facilities that provide voice, data, and broadcast communications in the Americas. The company operates a geosynchronous (GEO) satellite services business and has begun the development of advanced constellations of low earth orbit (LEO) satellites that travel around the earth at high velocities with the ability to serve areas at higher latitudes than GEO satellites can service. TSAT’s GEO fleet has a remaining commercial life of about six years and a utilization rate of 88%. The company’s equity ownership on 2 May 2023, according to the company’s proxy and assuming all Class A Units, Class B Units and Class C Units had been exchanged on a one-for-one basis, showed that PSP Investments, MHR/Dr. Mark Rachesky and GAMCO Investors held 36.6%, 36.4%, and 5.6%, respectively.

A service of

Start your trial. Today

Explore unlimited content like this, available only in the platform.

Already a client? Sign in