TalkTalk’s B2B arm sale keeps liquidity afloat; refi concerns continue to hover – FY23 Credit Report

TalkTalk Telecom Group (TalkTalk), a UK-based telecommunications enterprise, on 29 September 2023, announced the sale of its B2B Business arm for GBP 95m to its shareholders. Although this has aided its cash position, the agreed sale price is lower than previous expectations. As a result, on 10 October, the yields on the GBP 685m senior unsecured notes (SUNs) reached an all-time high of 32%, trading at 70, down from 75 (yield: 25.6%) post the announcement of lower sale price on 29 September. However, following an investor meeting held on 18 October, with the management showcasing confidence in refinancing its SUNs at par, the trading levels improved. As of 2 November, the SUNs were trading at 76 (yield: 27%), having fallen from 80 (yield: 14%) a year ago.

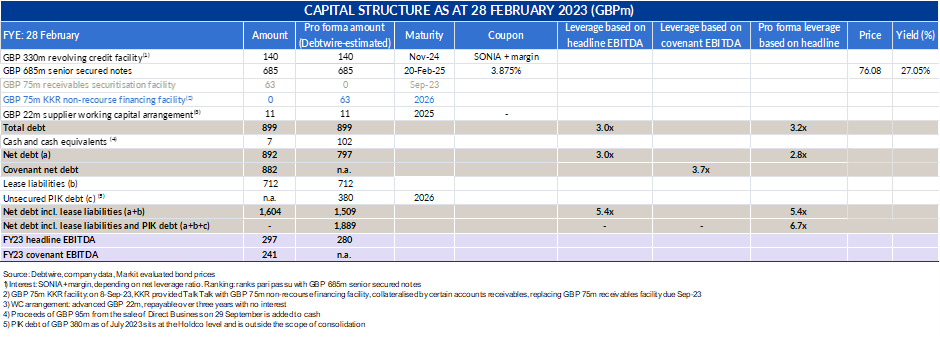

The company is also seeking fresh investment, in equity and debt, as borrowings of GBP 825m (92% of total debt) are set to mature by February 2025. Cash upstreaming to the parent entity (holdco) has strained liquidity over the past two years, although lenders of TalkTalk’s GBP 330m revolving credit facility (RCF) granted a relaxation on the net leverage covenant for FY24 (ending 28 February 2024). A group of bondholders chose Perella Weinberg Partners as their financial advisers while another group tapped Milbank. The RCF lenders are working with PwC.

Ratings update: On 18 October, S&P placed Talktalk’s B- ratings on CreditWatch negative given the high execution risk on raising debt and equity to refinance its upcoming debt. Similarly, on 7 August, Fitch downgraded TalkTalk to B- from B, while placing it on ratings watch negative, citing operational risks leading to concerns over refinancing.

Sale of B2B wing: In September 2023, TalkTalk agreed to sell “TalkTalk Business Direct”, its B2B arm to an SPV “TFP Telecoms Limited (TFP)” controlled by the main shareholders of TalkTalk Telecom Group for GBP 95m (previously valued at GBP 150m), while signing a long-term wholesale service agreement of GBP 25m for three years with the SPV. If the B2B Direct is sold off to a third party in the next 12 months, net proceeds in excess of GBP 95m would be passed on to TalkTalk. In FY23 (ending 28 February 2023), the B2B arm accounted for GBP 17m or 5% of EBITDA.

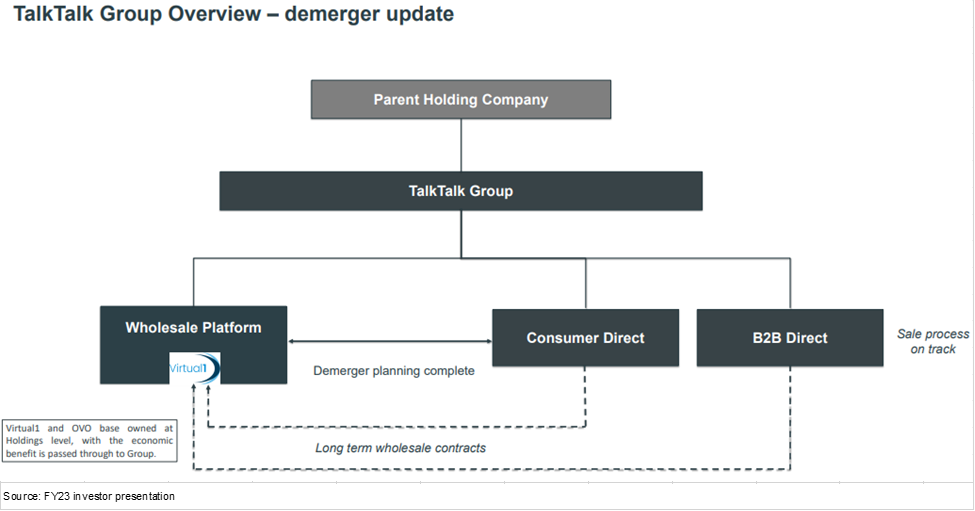

Potential equity injection for the wholesale business: For the wholesale business, the company has kickstarted the process for raising equity and is in talks with certain private equity firms. On the consumer side, the company is looking out for options to raise debt. Note that, in July, TalkTalk announced the completion of the demerger of its consumer business from the wholesale platform (see business description below) allowing it to cut central costs and expanding options for strategic mergers and acquisitions (details undisclosed).

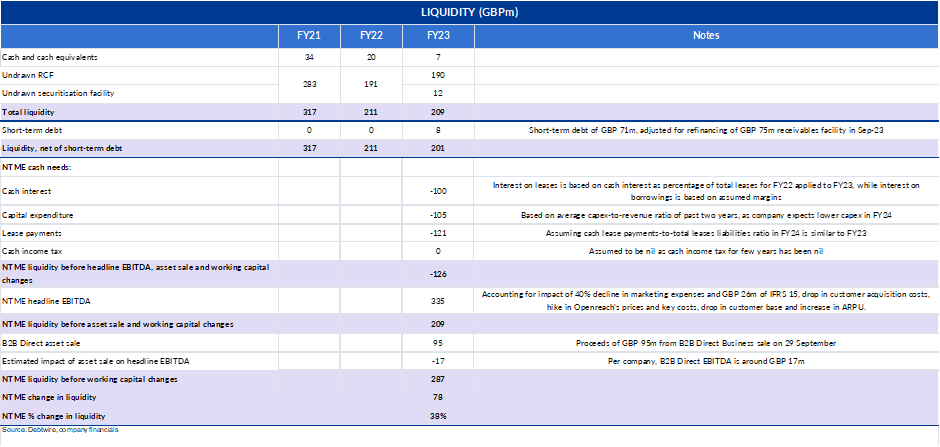

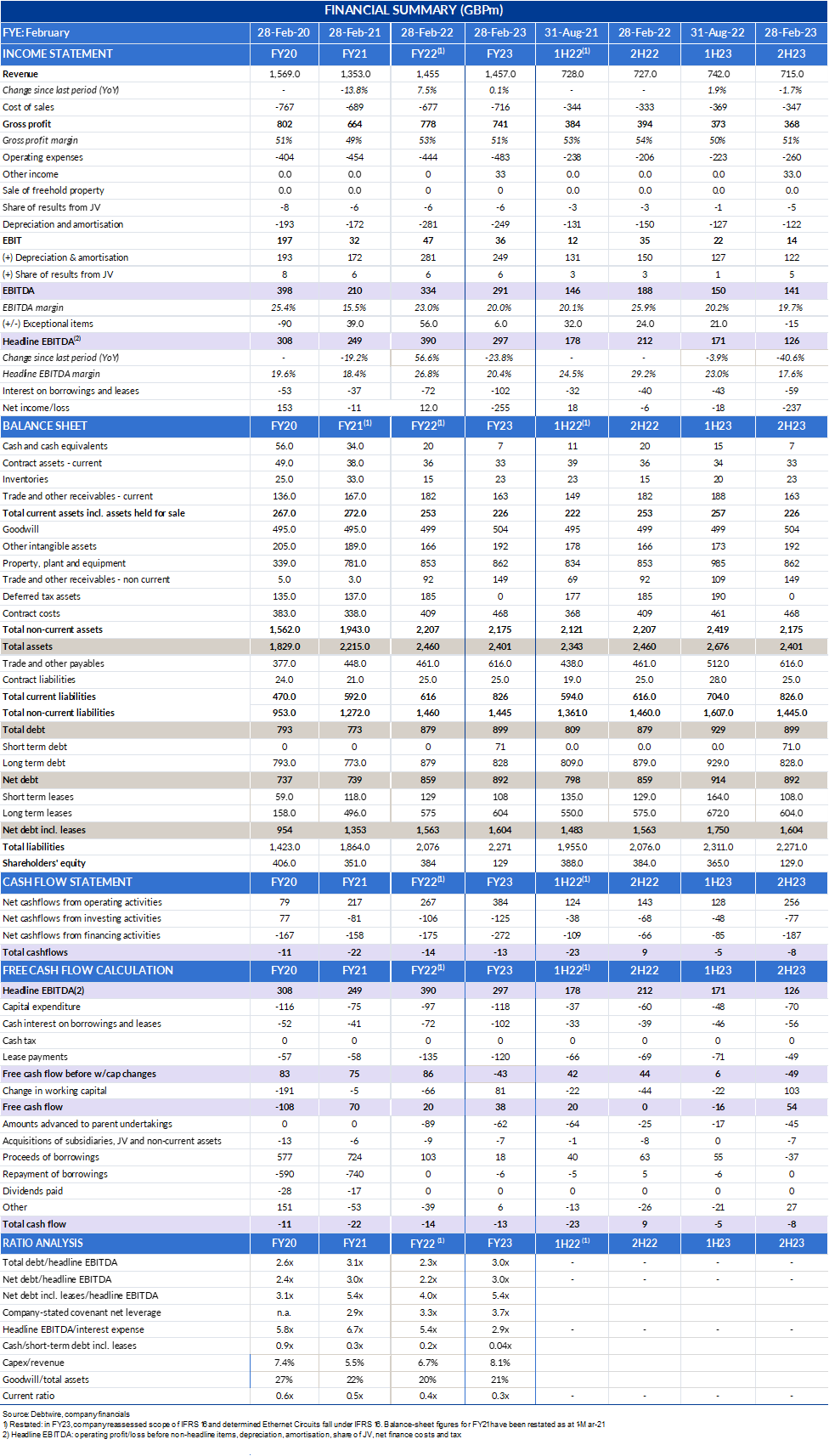

Price hikes to support EBITDA: Management expects the impact of inflation-linked price hikes to be evident in 1Q24, with a significant rise in average revenue per user (ARPU) in each segment. However, the company is unable to pass on the price hikes to all its customers immediately since a portion of the total Consumer Direct’s customers of 2.5 million are on fixed rate terms for 18-24 months. Moreover, the total customers of the group contracted by 2.6% quarter on quarter in 1Q24 to 3.8 million. In addition, gross profit margin could fall below 50% (FY23: 51%) given the hike in Openreach’s (supplier to TalkTalk’s wholesale arm) prices by approximately 11%, as per a Debtwire article dated 27 October. That being said, the company has replaced Openreach’s “112 deal”, which provided pricing discounts to customers on meeting certain volume targets, with Openreach’s new Equinox deal. The new deal focuses on incentivizing full fibre sales, thereby supporting the company’s transition from copper to full fibre. As a result, management expects customer acquisition costs to decrease in FY24, while marketing expenses are guided at GBP 135m versus GBP 180m in FY23. Hence, we expect the company’s headline EBITDA to grow to GBP 335m in FY24 (FY23: GBP 297m). Excluding the impact of the B2B Direct, the FY24E headline EBITDA is estimated to be approximately GBP 318m ( see Excel for EBITDA calculation and refer to liquidity table for details).

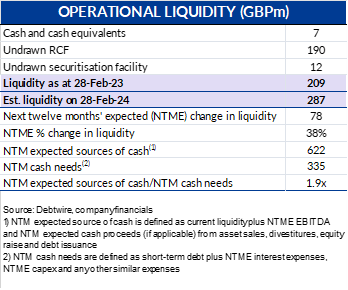

Surge in Liquidity: We expect a cash outflow of approximately GBP 335m from capex, cash interest and lease payments for FY24, versus the inflow from the asset sale proceeds of GBP 95m and NTME headline EBITDA of GBP 318m (excl. B2B Direct). We believe liquidity (before working capital changes) could increase to GBP 287m as of February 2024 (February 2023: GBP 209m), which also includes the impact of sale of the B2B arm. Note that its GBP 330m Revolver comes due in November 2024, followed by the GBP 685m SUNs in February 2025, which could exert pressure on liquidity.

Drop in pro forma leverage, PIK debt hovers: As of FY23, net debt stood at GBP 892m, with net leverage of 3x, while cash balance was at GBP 7m. Considering the asset sale proceeds added to cash, the pro forma cash balance increases to GBP 102m, with net debt dropping to GBP 797m, corresponding leverage decreasing to 2.8x.

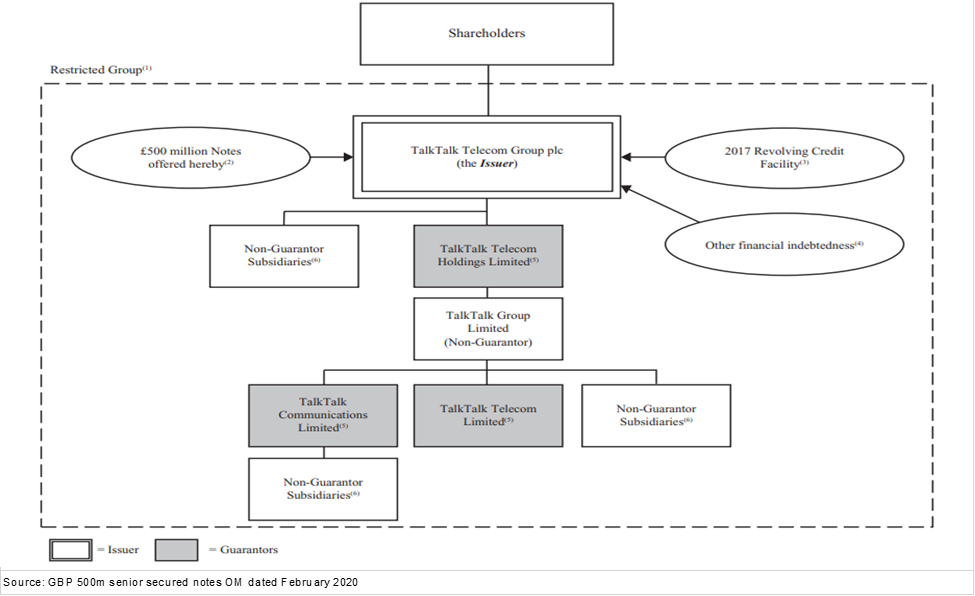

Apart from total debt of GBP 899m as of FY23, there is also GBP 380m unsecured PIK notes as of July 2023 (up from GBP 291m reported at FY22), which is held at Holdo level and outside the restricted group (see organization structure below). However, in FY23, TalkTalk made a GBP 3m payment related to PIK debt at Holdco level, significantly down from a payment of GBP 84m in FY22. If the PIK notes are included in TalkTalk’s borrowings/capital structure, pro forma net debt incl. leases balloons to GBP 1.9bn, while the corresponding leverage rises to 6.7x.

Covenant relaxation: The revolver agreement has covenants capping net leverage at 3.75x for FY23, which would have then stepped down to 3.5x for FY24 but has been relaxed to 4.95x for FY24. As of FY23, covenant net leverage stood at 3.66x, based on covenant net debt of GBP 882m and covenant EBITDA of GBP 241m. TalkTalk is also required to maintain minimum liquidity (amount undisclosed) under the revolver agreement. On 5 September, a GBP 20m portion of the GBP 330m RCF was sold at auction, with the piece trading in the high 70% to par, as lenders opted to offload the debt during the company’s refinancing efforts.

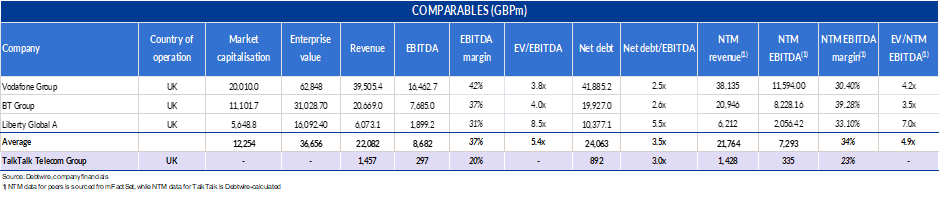

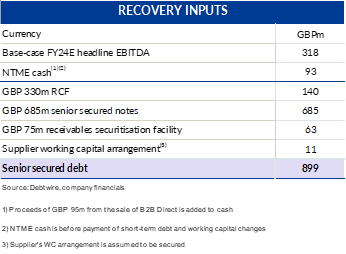

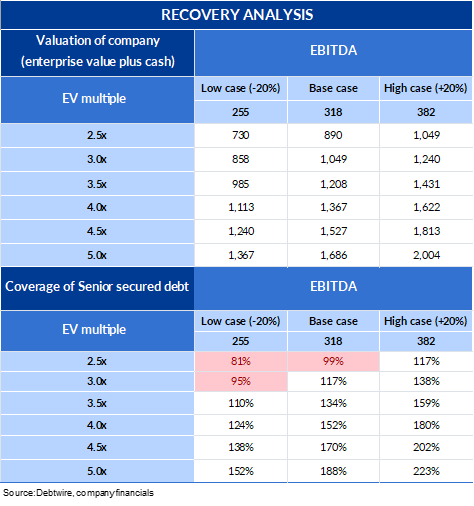

Recovery analysis: Recovery analysis: TalkTalk underperforms its peers with an EBITDA margin of 20%, significantly below the peer average of 37%, while its net leverage is 3x compared with a peer average of 3.5x. Including leases and holdco PIK debt, the company’s net leverage surges to 6.7x. As per our recovery analysis, TalkTalk’s senior secured debt receives full coverage at an assumed enterprise value/NTME EBITDA multiple range of 3x-5x (peer average: 4.9x) with a base case NTME headline EBITDA (excl. B2B Direct) of GBP 318m and NTME cash of GBP 93m (includes proceeds from the sale of B2B Direct of GBP 95m but excludes working capital changes). As reference, the TalkTalk’s B2B arm was sold at an EBITDA multiple of 5.5x. As of 2 November, the SUNs were trading at 76 (yield: 27%) due to the risk related to its refinancing and the possibility of incurring additional indebtedness related to the PIK Holdco debt. However, the growth prospects in EBITDA could provide an upside.

Financial performance recap: despite implementing price hikes and acquiring Virtual1 in May 2022 and OVO in October 2022, TalkTalk’s revenue remained steady at GBP 1.45bn in FY23, affected by weakness in voice services and a 2% contraction in the customer base. Inflation bloated the cost of sales and operating expenses (largely power costs and wages) by 7% YoY to GBP 1.2bn (FY22: GBP 1.1bn). Consequently, headline EBITDA plunged 24% YoY to GBP 297m from GBP 390m in FY22, while the corresponding margin declined to 20% (FY22: 27%). During the period, capex jumped 22% YoY to GBP 118m on account of a transition to full-fibre broadband from copper infrastructure. In addition, interest costs soared 42% YoY to GBP 102m, with the average interest rate rising 300 basis points (bps) to 7.2% in FY23. However, positive negotiations with suppliers led to a working capital release of GBP 88m (FY22: cash outflow of GBP 66m), producing higher FCF of GBP 38m versus GBP 20m in FY22.

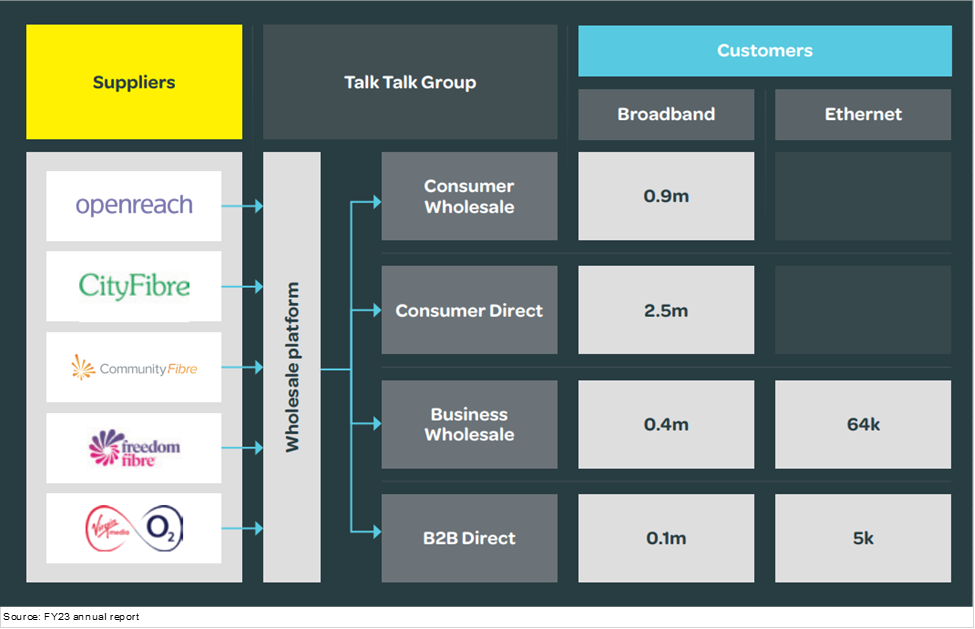

Business description: TalkTalk Telecom Group is a UK-based telecommunications company providing competitively priced fibre, broadband, landline, television and mobile services. Its fixed-line network covers 96% of UK homes, while broadband services cater for approximately 4 million users. TalkTalk largely operates across three inter-connected business lines: wholesale platform; consumer direct business (internet access); and B2B direct business. The wholesale business aggregates the incumbent and alternative networks (AltNet) full fibre network. The customer direct business provides affordable fixed-line connectivity to residential customers, while B2B Direct caters for business enterprises. Consumer Direct and B2B Direct are anchor customers of the wholesale platform. The wholesale platform represents 75% of group EBITDA and GBP 1.2bn of revenue (following the de‑merger of Consumer Direct). According to its FY23 annual report, TalkTalk is a subsidiary of TalkTalk Finco Limited (previously Tosca IOM Finco Limited), while the ultimate parent is TalkTalk Holding Company (formerly Tosca IOM Limited).

Organisational structure:

A service of

Start your trial. Today

Explore unlimited content like this, available only in the platform.

Already a client? Sign in