TalkTalk bondholders pick Milbank and PWP as advisors, company targets par refi for bonds

Milbank is advising a group of TalkTalk bondholders following pitches held last month, according to two sources familiar with the matter.

Perella Weinberg Partners has been chosen to advise the group of bondholders who heard presentations from at least two other investment banks, as reported. The selection comes as the UK telecoms provider told investors at meetings last month it is still targeting a par refinancing of its bonds, which are maturing in February 2025 and are trading at a significant discount.

The company’s management also disclosed that they had begun a bondholder identification process, according to two buysiders. The process was being run through issuer agent CMi2i, according to the first buysider.

“The key message is that [TalkTalk’s] CFO is confident on a par refinancing of the bonds,” the first buysider said. “Given where they are trading it doesn’t look like this is imminent but the par refi was the key message.”

TalkTalk’s B-/B- rated GPB 685m 3.875% senior secured 2025s have moved around five points higher from before the investor meetings to be indicated today (1 November) at 76-mid with a 27.0% yield-to-worst on Markit.

TalkTalk’s debt stack also includes a GBP 330m RCF maturing in November 2024, which ranks pari passu with the senior secured notes and has seen some trading on the secondary market. A GBP 20m piece of the loan cleared an auction in early September in the high-70% to par, as reported.

A group of RCF lenders in July chose PwC as their advisor to coordinate the financial information that lenders would be receiving ahead of a refinancing, as reported.

The RCF debt had a 3.75x net leverage test at FY22/23 fiscal year-end 28 February 2023 that stepped down to 3.5x in FY23/24, but under a covenant relaxation for the RCF TalkTalk had secured with its banks, the test for the fiscal year end-February 2024 has now been set at 4.95x to give more headroom in case of any downside scenarios. It reported 3.66x net leverage at FY22/23 for covenant purposes.

The net leverage covenant test level then reverts down to 3.5x after the relaxation period ends in February 2024. There is also a minimum liquidity covenant built in during the relaxation period.

In early September, TalkTalk managed to obtain an approximately three-year GBP 75m non-recourse financing facility from KKR, which replaced a receivables facility of the same amount that was coming due the same month.

TalkTalk of the town

TalkTalk met with investors last week with a session organised by British bank Barclays on 18 October and a fireside chat also hosted by New Street Research, a TMT-focused independent research boutique, on 19 October, as reported.

The management at the meetings included representation by recently appointed CFO James Smith who joined the business after nine years as CFO at UK oil & gas company Capricorn Energy and previously had an investment banking career at Rothschild and Merrill Lynch.

Unlike previous interactions with investors, TalkTalk’s management came across as more open and is actively engaging with bondholders this time around, according to two buysiders.

The management disclosed that TalkTalk has initiated data rooms to facilitate the process of raising equity to back the company’s Wholesale business. Thereafter, it hopes to raise debt against the Wholesale platform and Consumer Direct business.

“When a company starts a sale process they create a data room which provides a folder which buyers would require to make a proposal. They are in a process and they could raise equity based on the wholesale business,” a third buysider said.

While noting that the company has been talking to private equity funds for the Wholesale business, it is unclear if TalkTalk would be successful in the equity raise, the first buysider said. The remaining business will be smaller to raise a bond but perhaps it can go pursue the direct lending route, he added.

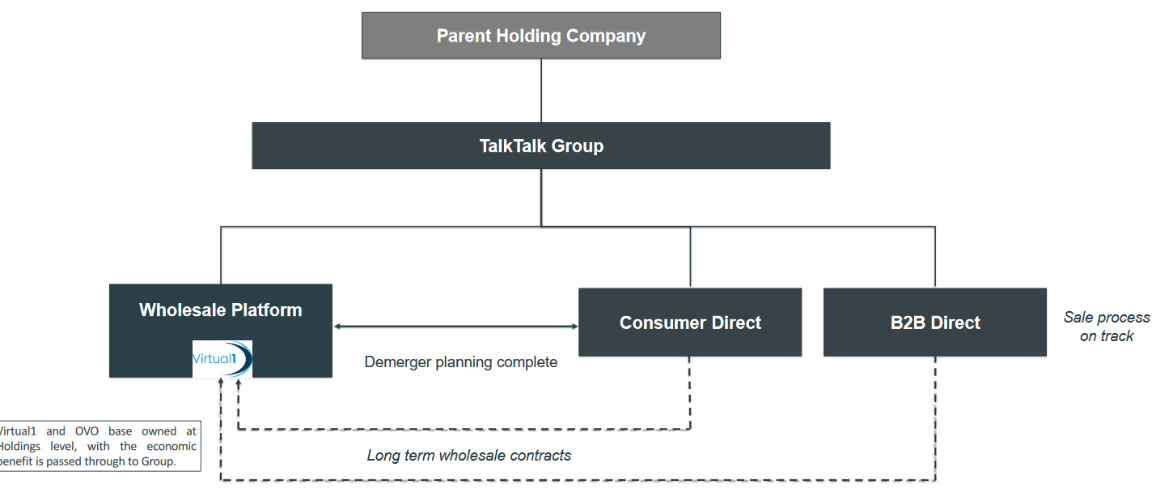

TalkTalk had previously de-merged its corporate structure with the business split into three entities including the Wholesale Platform, Consumer Direct business, and B2B Direct business which was sold to the main TalkTalk shareholders for GBP 95m, as reported. The management confirmed at last week’s meetings that the B2B Direct arm had around a GBP 17m EBITDA for FY22/23, implying a 5.5x EV/EBITDA.

Source: TalkTalk FY22/23 investor presentation

Let’s TalkTalk money

The management team has argued at the investor meetings that the company can be cashflow generative. This is despite the company already reporting GBP 33m negative net cashflow in the FY22/23 period (fiscal-year end 28 February 2023) after accounting for intra-group transactions. This was based on a GBP 297m FY22/23 headline EBITDA then adding a GBP 89m working capital release, deducting GBP 118m capex, GBP 11m investments, GBP 6m non-headline spend, GBP 44m interest on borrowings, GBP 178m cash payment on leases, GBP 3m PIK payments, GBP 36m intragroup cost allocations, and GBP 23m funding of OVO investment.

However, some investors questioned the company’s ability to generate cash. “There was not so much new granular information and there is low confidence on significant cash generation versus the high debt burden,” the third buysider said. “There was also a question on what is the leveragability of the business.”

TalkTalk’s management also stated that current trading was on track versus its budget since the reporting of FY22/23 results. The company management reiterated previous guidance that earnings can grow through an increased average revenue per user (ARPU) and reduced marketing costs.

“We forecast an EBITDA increase this fiscal year and think they can do a GBP 375m EBITDA versus GBP 297m in FY22/23,” the first buysider said. “But we forecast GBP 45m non-headline costs from running the copper network which will not go away and working capital could also become an outflow. So, while the CFO said they can generate cash, we don’t see it.”

The management team provided additional colour on the company’s Openreach infrastructure owners that enable TalkTalk customers to gain access to high-grade connectivity via the TalkTalk national network and industry-leading customer service capability. The integration of the alternative network provider into the TalkTalk platform enables a lower average cost per circuit to be achieved, according to the TalkTalk FY22/23 annual report.

The end of the Openreach 112 deal, which was replaced by the Equinox FTTP (fibre to the premise) offer, allows for more disciplined investment in new customer acquisition in the Consumer Direct business and is expected to improve cashflow. However, the management noted in the investor meetings that higher Openreach costs will be passed on to TalkTalk consumers but that many are locked into fixed-term contracts so it will take time for the pass-through of higher costs to materialise into greater selling prices.

The third buysider noted Openreach increased prices in April but then it takes time for the price increases to come through as people have different renewal periods. He was concerned they are heading into the latest results with costs going up and this could provide weakness.

“They have done price increases and Openreach prices are inflation-linked and up 11%. Gross margins could drop however as customers are growing less than 5% and their key input costs are up so this is a problem for gross margins,” the first buysider said. “Openreach costs increases are a headwind and they may struggle to pass them through as some customers are on fixed terms for 18 to 24 months. Their front-book is also lower than their back-book.”

The second buysider argued that while there are difficulties in being able to pass through costs given the fixed term contracts, that is a common challenge for every company in the sector.

He acknowledged it is a headwind, but it is not a new one, and tailwind wise the company is going to decrease marketing expenses. “The company also guided OK numbers for next quarter,” he added.

“We think there is a 30% likelihood of TalkTalk bonds going to par but the Amend-and-Extend scenario is most likely with the situation not as rosy as the management see it,” the first buysider said. “One avenue [for par refi] is that the company gets sold to Virgin Media.”

Sale talks with British telecommunications company Virgin Media O2 broke down in March 2023 after it was reported in July 2022 that Virgin Media O2 had placed an initial GBP 3bn offer for TalkTalk, according to a sector press report.

A fourth buysider countered that he does not like TalkTalk and still thinks this is a default candidate. He argued the bonds are overvalued and unless there is a shareholder injection then there is no hope for the bondholders.

“If the hope is a refi when the bonds are in the mid-70s with just over a year till maturity then it is not good,” the fourth buysider said. “It doesn’t look like the shareholders will contribute anything so far.”

Keep TalkTalking

TalkTalk previously held investor meetings through Citi on 18 July, during which it elaborated on its expected operational recovery and refinancing strategy. But some investors were apprehensive about the refinancing plan given its increasing HoldCo PIK size, downward pre-IFRS 16 earnings trajectory, and uncertainty on realising any speculated sale value on its B2B Direct business, as reported.

The outstanding amount on the HoldCo PIK had risen to around GBP 380m after an around GBP 90m debt increase via fund Ares, which lent the amount to the HoldCo via a Virtual1 asset that is outside the restricted group, as reported. Adding GBP 380m to net debt means that adjusted covenant net leverage climbs above 5x and investor-estimated pre-IFRS 16 adjusted net leverage climbs above 10x. The HoldCo PIK had previously been disclosed as GBP 291m in size as of 28 February 2022, according to public filings for company entity Tosca IOM Limited.

Maturing in 2026, the PIK is unsecured debt in the shareholder entity and it sits structurally subordinated to the bond issuer group debt, as reported.

Click HERE for the Debtwire FY22/23 TalkTalk credit report.

TalkTalk and New Street Research declined to comment.

Milbank, PWP, Barclays, and CMi2i did not respond to a request for comment.

A service of

Start your trial. Today

Explore unlimited content like this, available only in the platform.

Already a client? Sign in