Solenis revenue and margins improve, while synergies post-Diversey merger are yet to manifest – 3Q23 Credit Report

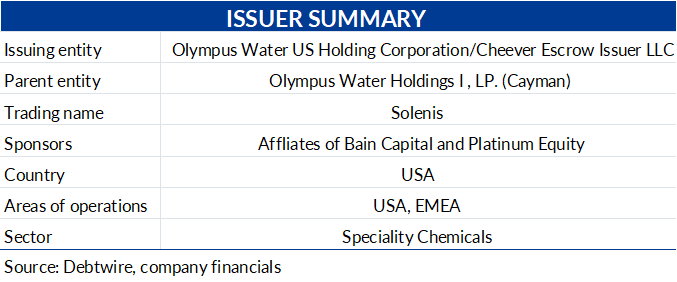

Olympus Water US Holding Corporation (Solenis), a US-headquartered leading supplier of specialty chemicals to consumer solutions (CS), industrial solutions (IS) and pool solutions (PS) segments, reported 3Q23 results (for the quarter ending June 2023) on 10 August. The company completed a merger with Diversey (a US-based cleaning solutions group catering to the institutional and food/beverage segments) on 5 July.

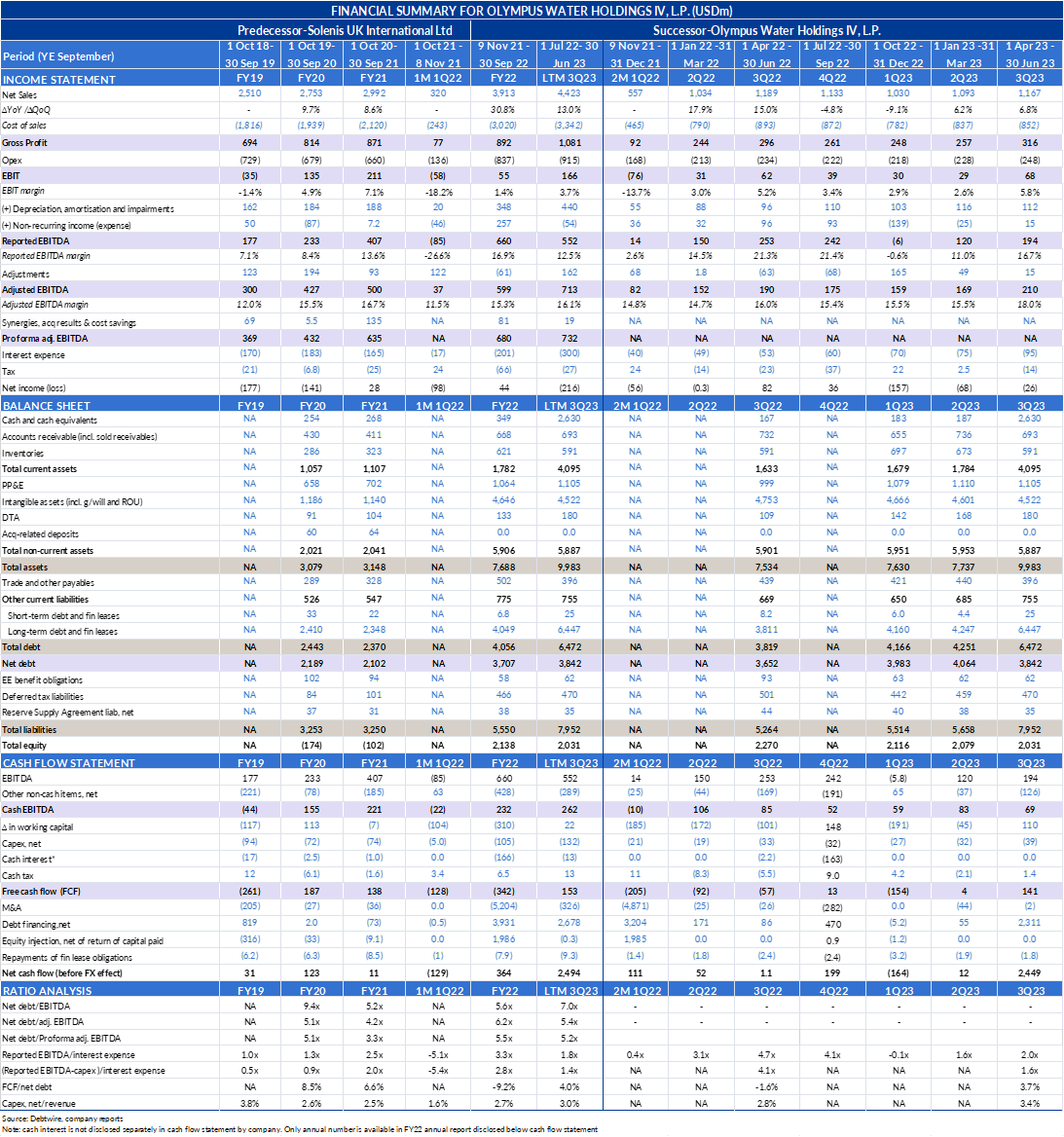

Total revenue for the quarter came in at USD 1,167m, down 1.9% year-on-year (YoY), on the back of a 10.2% volume decline across all three segments owing to customer slowdown and curtailments, and despite price increases of 5.7%. A repositioning of the business in Russia and industry-wide lower packaging volumes also contributed to the overall volume decrease. Solenis reports segmental revenue on a pro forma (PF) basis to reflect the results of Sigura business (acquired in November 2021) for all the periods presented, eliminating the non-cash purchase accounting adjustments. Accordingly, PF revenue dropped 6.0% YoY. Management clarified that volume decline is an industry-wide issue, and curtailments started in the Europe region have now been extended to the Americas as well.

However, adj. EBITDA increased 10% YoY (on a reported basis; on a PF basis, it maintained at the same level). Stable prices and a start of raw materials deflation, supported by the realisation of cost synergies from headcount actions, led to margin improvement. Both the CS and IS segments recorded a YoY increase in adj. EBITDA, while adj. EBITDA dipped in the PS segment. Management says that PS volumes suffered, as customers negotiated for volume at the start of the year when the Clearon acquisition took place (9 September 2022). Most of the contracts were filled by the time Solenis (post-acquisition) approached customers for contracts, resulting in a loss of business, with volumes not expected to recover this year.

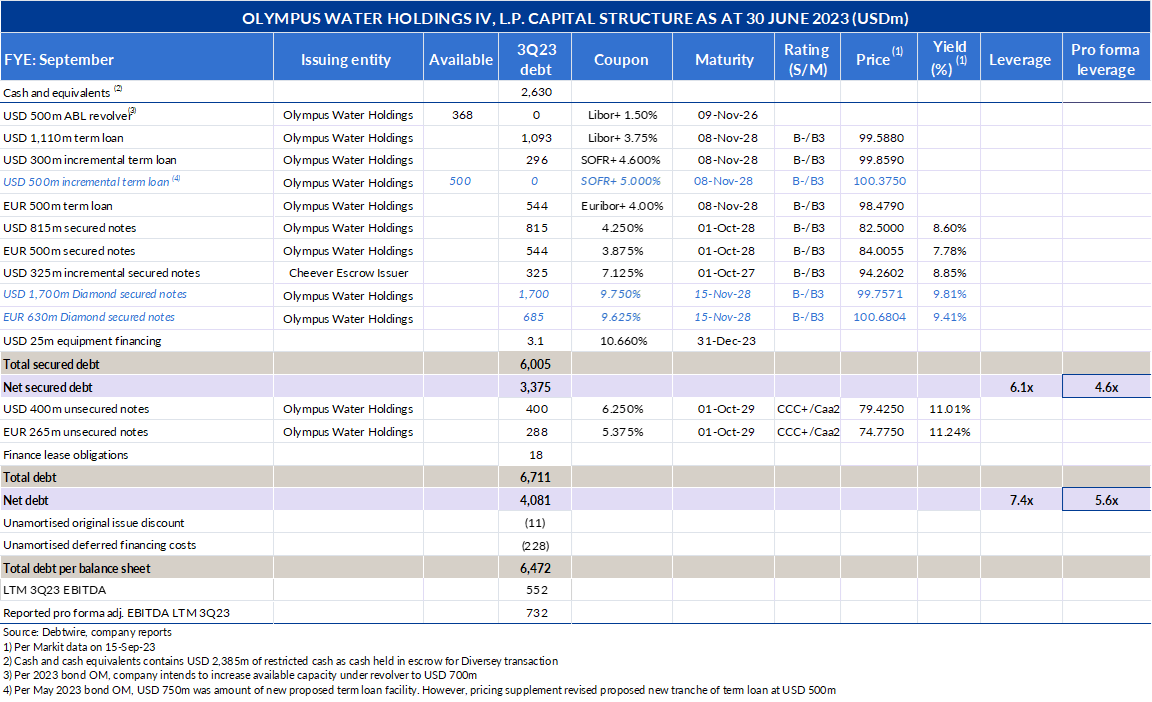

Free cash flow (FCF) turned positive to USD 141m (3Q22: negative USD 57m), driven mainly by working capital inflow owing to reduced inventory levels. Thus, higher cash generation and repayment of revolving credit facility (RCF) utilisation during the quarter manifest in leverage improving to 5.58x from 5.68x in the last quarter. Cash held in escrow of the newly-issued bonds (USD 2,385m) for the Diversey acquisition had a neutral impact on net debt.

Post-merger debt has been calculated considering the incremental term loan (closed on 5 July) and repayment of Diversey’s existing debt (because of a change-of-control provision). The cash balance is calculated using June’s closing cash balances of Solenis and Diversey, but adjusted for:

- Equity purchase price paid for the Diversey acquisition.

- Repayment of Diversey’s account receivables facility.

- Repayment of the RCF outstanding.

- Squaring off the derivative net liability position.

- Cash paid for acquisition transaction fees and other expenses.

PF leverage based on EBITDA (incl. synergies) comes to 5.4x, while leverage climbs to 6.6x if based off EBITDA (excl. synergies), as detailed above.

Bond prices have reacted positively (rising up to 6% over the past three months) to the improved performance, with the 3Q23 adj. EBITDA margin recording a new high when compared with the past eight quarters.

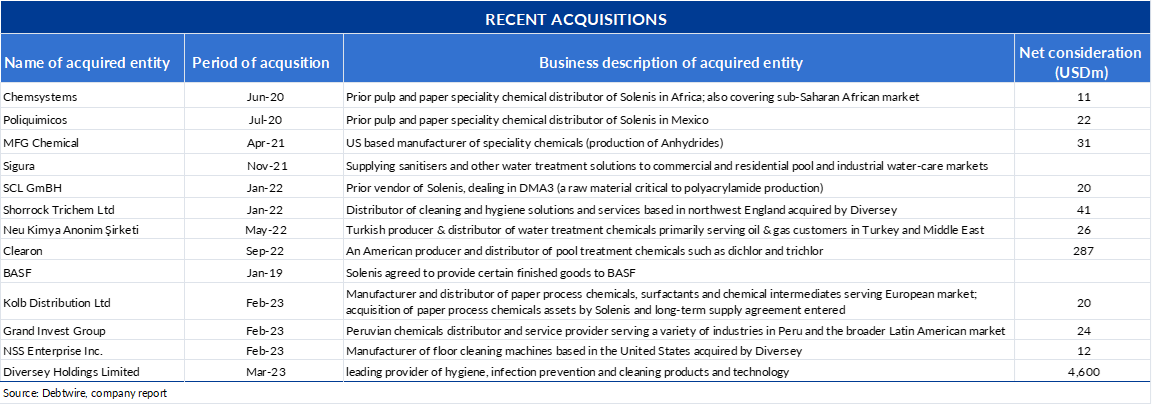

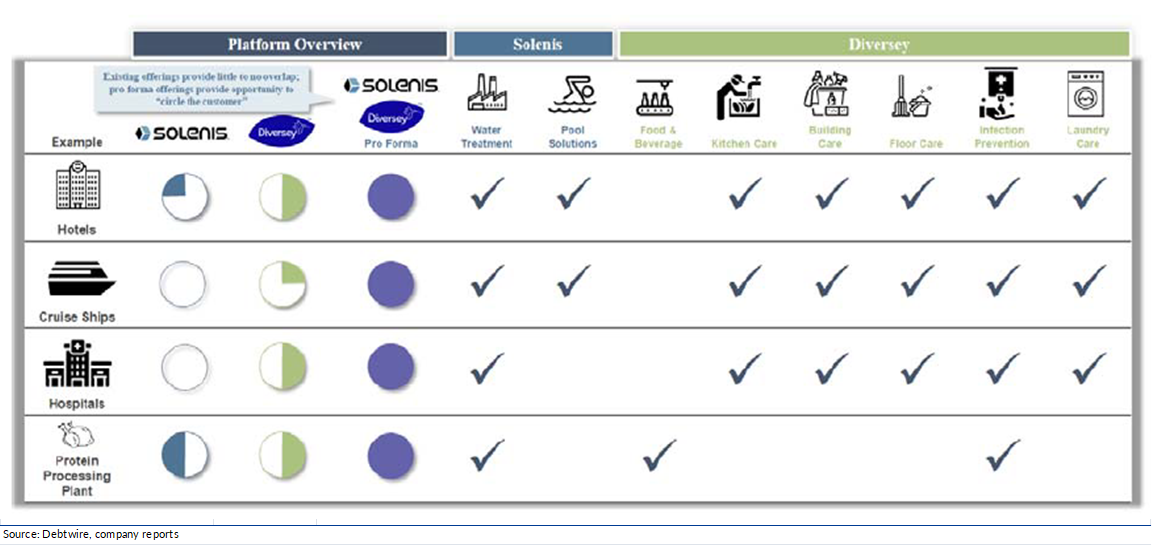

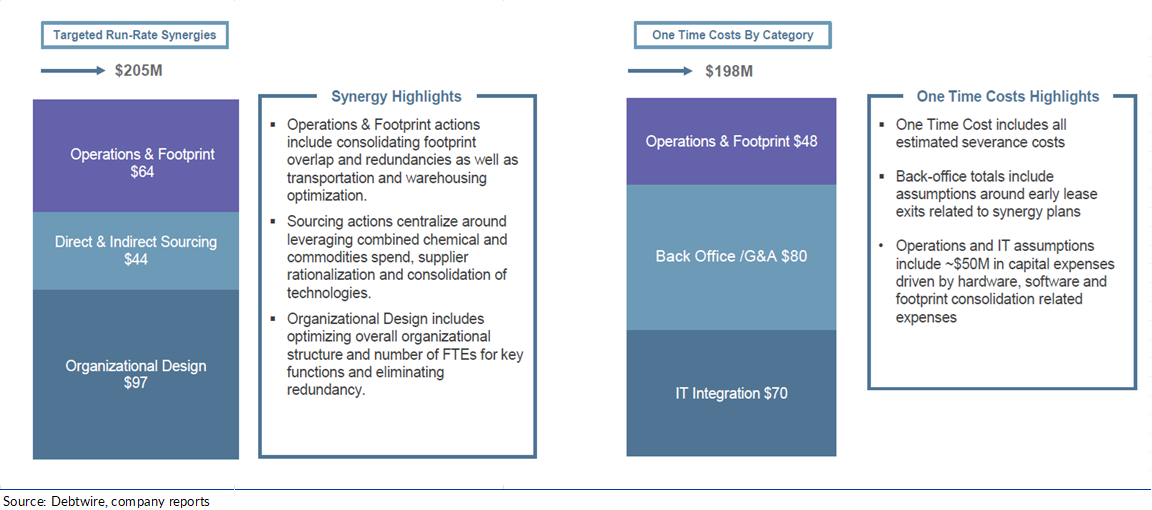

Acquisitions: the company has a history of expanding via acquisitions, with the latest being Diversey. Management believes the acquisition will provide cross-selling opportunities (see table below), with the combined entity becoming a ‘one-stop shop’ for water treatment, cleaning and hygiene solutions customers. Below is a summary of acquisitions and Diversey acquisition synergies expected to be realised 24 months from the close of the transaction.

Outlook: in addition to the acquisitions, we expect the following factors to impact revenue and margins:

Risks/issues:

- Industry-wide issues like the substitution of printed material with electronic media are likely to impact Graphic and Speciality Paper end-market sales, and a longer-lasting de-stocking trend may affect sales. Also, the energy crisis in Europe has pushed many industry players to Asia, offering the benefits of lower labour/energy costs. This increased competition could impact margins globally. On the other hand, according to Moody’s Chemicals industry report, EBITDA growth is set to improve in 2024.

- The company has confirmed that besides Europe, curtailments have started in the Americas as well, thereby impacting demand in the main regions where Solenis operates.

- Management clarified in the latest earnings call that price increases will not continue at the same level as the first two quarters and a 90-day lag following increases in raw materials prices is set to resume in the future. This may have an adverse impact on margins.

- Margins are being pressured by zero-margin sales under the reverse supply agreement (RSA) with BASF (entered in January 2019, maturing in November 2028).

- Per Diversey’s last annual report, controls to ensure the existence of inventory, timing of revenue recognition and accuracy of customer rebates have not been effectively designed, documented and maintained. In the absence of an effective system of controls/disclosure, additional costs for remediation need to be undertaken.

Management mitigants/actions:

- Company sales are 97% recurring (per May’s bond OM), providing stability to revenue. Also, a diversified business model limits the obsolescence risk, as no product/solution represents a material part of the business.

- For the Clearon business to recover: the rationale for the Clearon acquisition was to take advantage of:

- Its increased trichlor production.

- Plant location not being on the Gulf Coast, insulating it from natural disasters.

- To capture its blue-chip customer base and pitch to big-box retailers such as The Home Depot, Lowe’s, Sam’s Club, etc.

- To reduce reliance on third-party suppliers for trichlor.

Trichlor is a highly regulated recreational water treatment and industrial hygiene biocide used to sanitise both water and surfaces. In the current year, Solenis has been unable to secure customer contracts on account of the acquisition timing (as explained above). However, management clarified that the company has already managed to secure contracts with customers for next year and is confident of recovering lost volumes.

- Management efforts in the PS of building spa business, upgrading to mass/dealer-branded volume, and focus on On-Time-In-Full (OTIF) measures should boost revenue and margins.

- In addition, management efforts in other segments such as selling out underutilised low-margin facilities like the BASF supply agreements, selective trading of price for volume, and building a corporate account programme is expected to enhance volumes.

- To align with reduced demand, the company is throttling back the number of hours/shifts.

- The Diversey acquisition should expand the sale of water treatment products to Diversey’s existing customer base within the food and beverage chemicals market, and realise additional manufacturing absorption benefits.

- Solenis has a proven track record of synergy realisation, with 97.6% of Solenis acquisition synergies realised and 50% (up to March) of Clearon acquisition synergies realised (projected full realisation at the time of transaction: September 2024). Therefore, we expect a staged realisation of Diversey acquisition synergies as projected to boost margins.

However, we feel the limited business overlap between the two entities, higher interest rates, weaker market fundamentals and higher capital expenditure (capex) heightens the execution risk of the merger. In our view, the realisation of synergies and business potential translating into higher revenue/margins in line with expectations remains to be seen. Buysiders have expressed concerns over the merger and the inflated EBITDA adjustments, as reported.

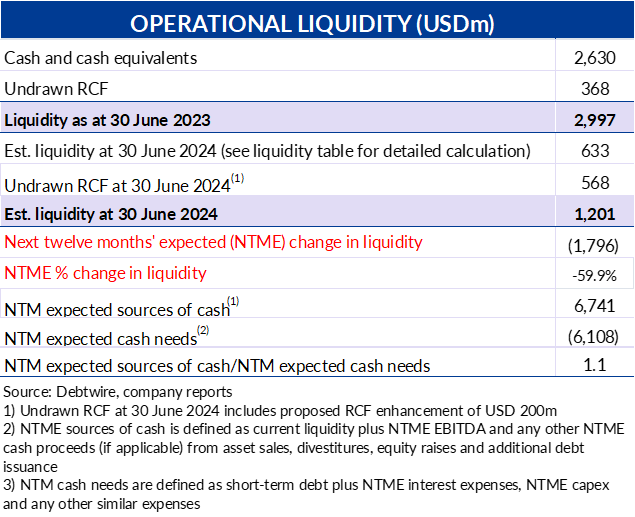

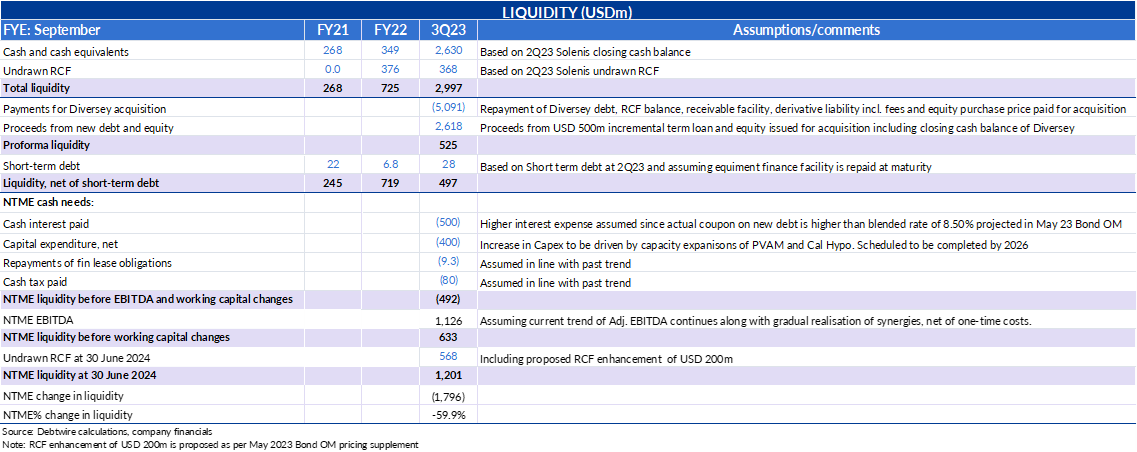

In view of the above, we expect the next twelve months (NTME) adj. EBITDA of USD 1,126m if the improved performance trend continues in line with Moody’s expectation of EBITDA growth in 2024 (Moody’s Chemical Industry report, 30 March). We consider a gradual realisation of merger synergies, net of one-off costs, as projected.

Other assumptions considered for calculating liquidity needs for the next two years include:

- Higher capex assumed as capacity expansion for polyvinyl amine (PVAM) at the Virginia facility costing USD 150m, and calcium hypochlorite (cal-hypo) at the US and South African facilities costing USD 100m; target completion by 2026. Moreover, the remaining capex for Project Mega is assumed to be incurred in NTME. (Diversey’s manufacturing consolidation project of combining five plants into four plants and co-locating its main warehouse and manufacturing capabilities should add capacity and drive annual cost savings of USD 30m).

- Higher cash interest assumed on the back of new debt issued at a higher rate than the blended rate of 8.50% projected in guidance, per May’s bond OM.

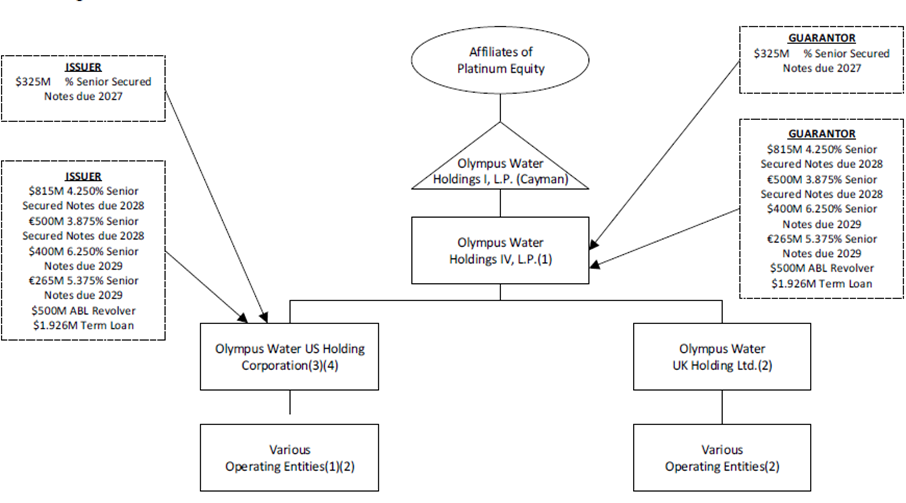

Liquidity: new debt has been issued by escrow issuer Diamond Escrow Issuer LLC since debt was issued prior to the acquisition. The acquisition will be effected pursuant to a merger of Diamond Merger Limited, a wholly-owned subsidiary (WOS) of Merger Sub, which is to merge with Diversey following which Diversey, will be a direct WOS of Parent (as defined in Issuer Summary above). As at 30 June, proceeds from new debt are held as restricted cash and disclosed separately.

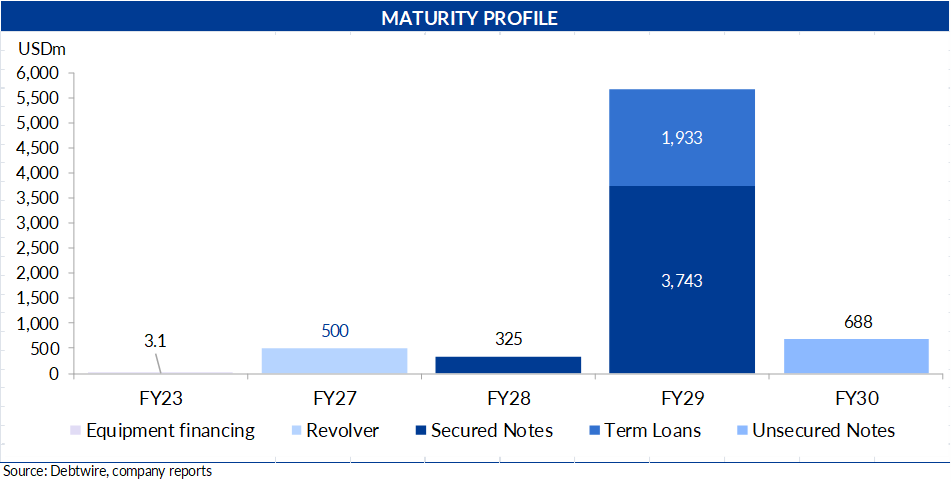

Solenis had an undrawn RCF of USD 368m as at 30 June, with an enhancement of USD 200m (existing RCF limit: USD 500m) proposed, as per the pricing supplement of May’s bond OM. Working capital needs are supported by an ING Receivables Financing facility of EUR 110m expiring on 31 January 2024. Also, with the company’s earliest maturity of long-term debt being FY27, we do not anticipate any short-term liquidity constraints.

The May 2023 Pricing Supplement for the bond OM revised the ratio requirement for the consolidated first-lien and consolidated senior secured debt ratio to not exceed 5x instead of 5.1x stated earlier. No revision has been made to the consolidated total debt ratio at 6.25x. As at 30 June, the company was in compliance with the stipulated ratio requirements. However, post-merger, all the ratios will only be maintained if the projected synergies materialise.

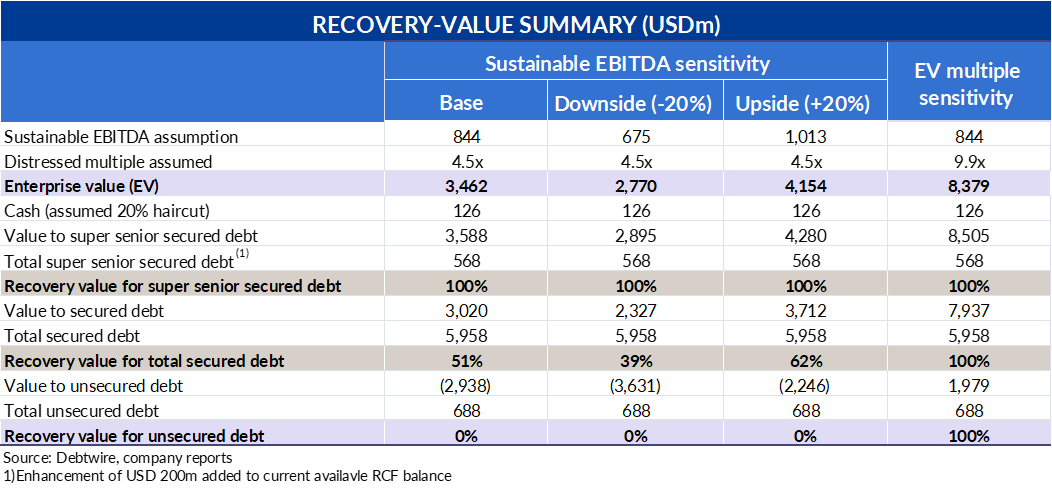

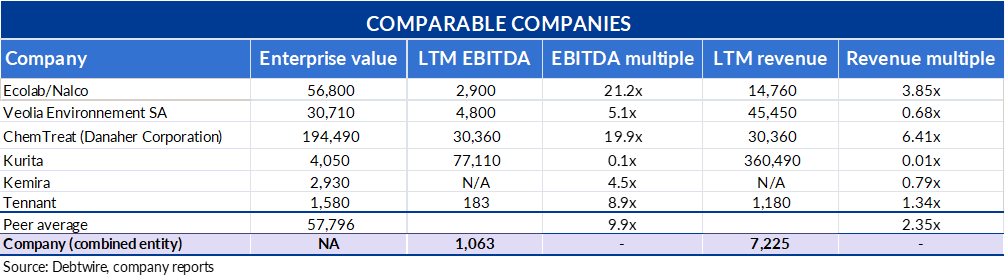

Recovery-value analysis: based on the assumptions below, we calculate the recovery value for Solenis’ senior secured debt (comprising the senior secured notes and term loans) to be around 51% in a distressed base-case scenario in FY24E and 0% recovery for the unsecured debt (senior notes). In a distressed scenario in FY24E (a 30% probability), we assume industry conditions do not improve as expected and curtailments continue, raw materials prices remain at higher levels, and a lack of pass-through contracts pressures margins. Non-realisation of synergies and business potential, as projected, coupled with continuing higher costs (energy/labour) are likely to further deteriorate EBITDA. In such a scenario, we assume EBITDA of USD 844m (a 25% haircut in our base-case scenario) and 20% haircut to post-merger cash. We show recovery calculations based on the lowest multiple (enterprise value/EBITDA multiple) of 4.5x and peer average of 9.9x. Note that peers are diversified corporations (Ecolab & Danaher) and not exact competitors of Solenis.

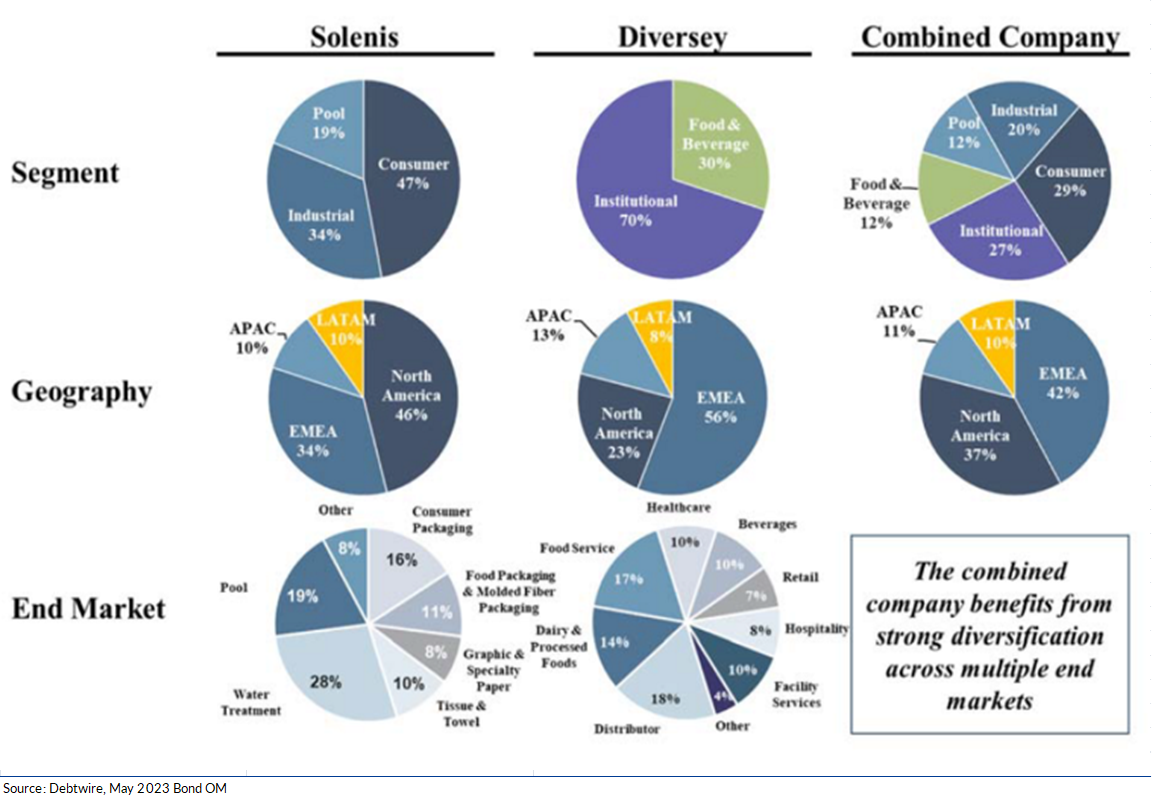

Revenue breakdown: historically, the company’s business segments were pulp & paper, industrial water and RSAs. A business segment revision took place in October 2021 following which:

- The Pulp & Paper segment was renamed CS, and food was reallocated to this segment.

- Industrial Water was renamed as IS and pulp was reallocated to this segment along with inclusion of RSA.

- A new PS segment was created to account for the contribution of Sigura’s Pools segment (incl. residential and commercial pools).

Post-Diversey acquisition, the segment, regions and end-markets of the combined entity will be as follows:

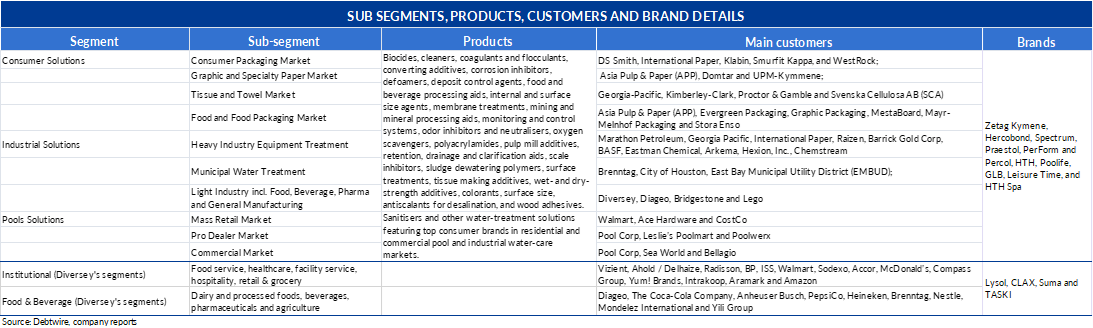

Main sub-segments, products, customers of the business include:

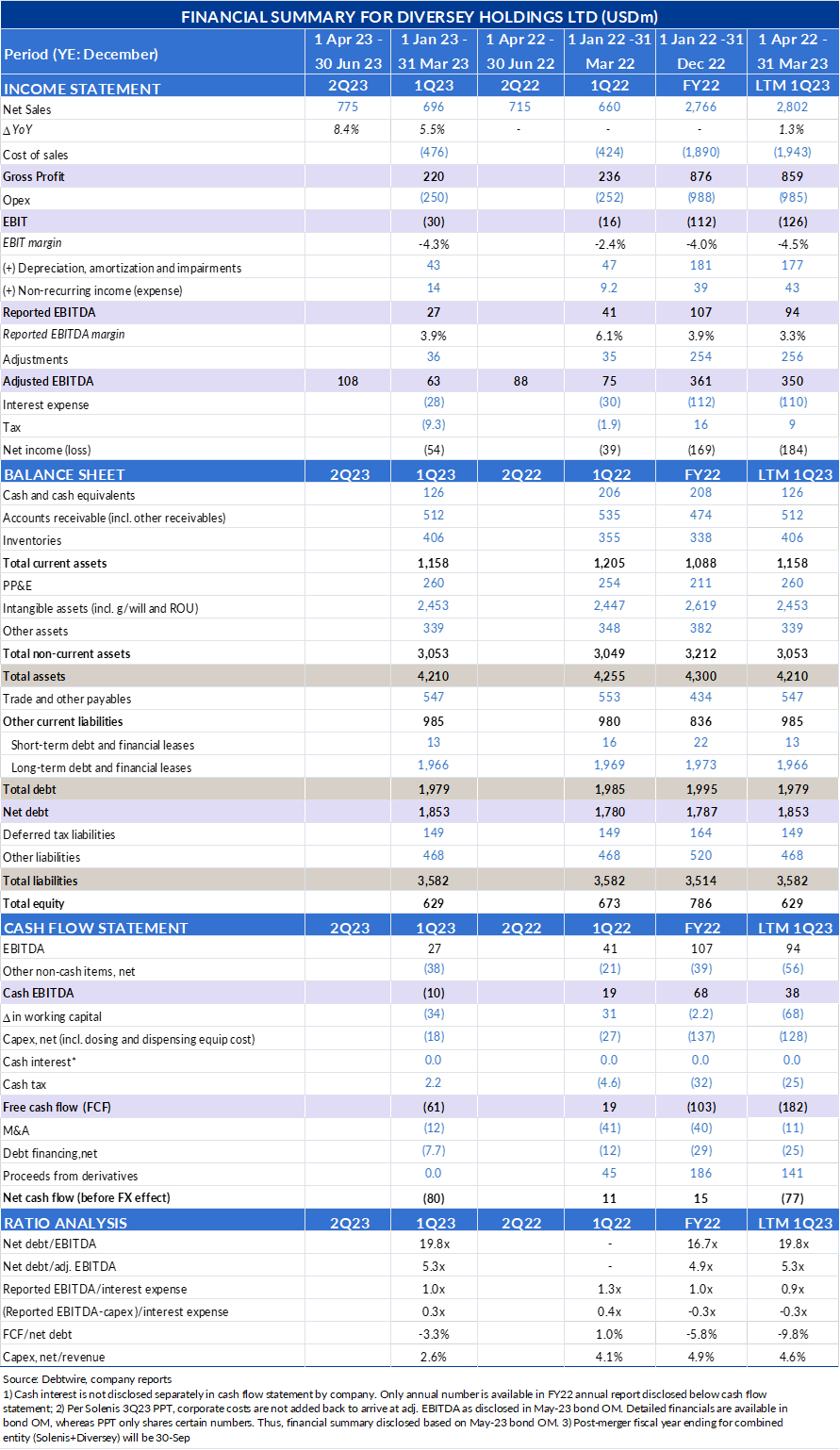

Ratings downgrade: Moody’s downgraded Solenis’ rating to B3 from B2 on 15 May, expressing concerns over the realisation of expected synergies from the latest acquisition (Diversey), while synergies from the Clearon acquisition are yet to be fully realised. Moody’s also raised concerns on credit quality post-merger given Diversey’s lower EBITDA margins and limited business overlap in challenging operating environment.

S&P affirmed its B- rating on Diversey merger on 15 May and removed ratings from CreditWatch placed on 9 March following the company’s merger announcement. S&P draws comfort that post-merger leverage is not much higher than current levels and liquidity sources to remain 1.2x of cash needs. S&P highlighted that the company faces integration risk, inherent in a transformative acquisition.

Corporate structure:

Source: Debtwire, bond OM

Business description: Solenis, headquartered in Delaware, the US, is a leading supplier of specialty chemicals and services to the pulp & paper, mining, food & beverage, paper generation, petroleum refining, chemical processing, general manufacturing and municipal/pool markets. The company has 49 manufacturing facilities, 11 labs consisting of R&D centres and Customer Applications serving 24,500 customers.

Diversey, headquartered in South Carolina, the US, is a leading global supplier and manufacturer of sustainable, high-performance hygiene, retail and grocery, infection prevention and cleaning solutions to the facility management, retail, healthcare, hospitality, food and beverage, commercial laundry, food service, education and government, dairy, agriculture and buildings service contractors markets. It has 21 manufacturing facilities and seven labs serving 85,000 customers.

Post-merger, Solenis will have approximately 15,600 employees spread across the North Americas, EMEA, and APAC regions.

On 9 November 2021, Solenis business was purchased from CD&R Seahawk Holdings, L.P and BASF Nederland B.V. for a net cash price of USD 5.10bn. Thus, Solenis was acquired by Platinum Equity in 2021 and Platinum combined Solenis with existing portfolio company Sigura. Post-merger Bain Capital, the majority shareholder in Diversey, will hold a minority stake in Solenis.

A service of

Start your trial. Today

Explore unlimited content like this, available only in the platform.

Already a client? Sign in