Small business loan servicer Kabbage hits Chapter 11 to wind down PPP portfolio left out of AmEx acquisition

Kabbage filed a Chapter 11 petition late on Monday (3 October) in the US Bankruptcy Court for the District of Delaware, reporting both assets and liabilities of USD 500m to USD 1bn. The lion’s share of the company’s debt obligations consist of PPP loan advances totaling USD 541m, but Kabbage also notes in its early bankruptcy court filings that its role as a PPP loan servicer has made it a target of class action litigation and government regulatory investigations.

The Chapter 11 case is assigned to Judge Craig Goldblatt in Wilmington, who has not yet scheduled a first day hearing.

The company

An online loan servicer founded in 2008, Kabbage is now in the midst of winding down its business after a sale of substantially all Kabbage assets to AmEx in October 2020, according to a first day declaration from Deborah Rieger-Paganis of AlixPartners, a restructuring advisor to Kabbage.

Initially, Kabbage focused on providing a lending platform for small businesses that relied on machine learning algorithms, public data and other information that allowed the company to quickly evaluate loan applications and disburse funds. Rieger-Paganis said that over the years, Kabbage expanded, adding business segments that provided flexible lines of credit to small businesses, business checking accounts, online bill payment, cash flow visualization tools, and e-gift certificates. The “substantial majority” of the Kabbage business was purchased by AmEx for USD 750m in October 2020.

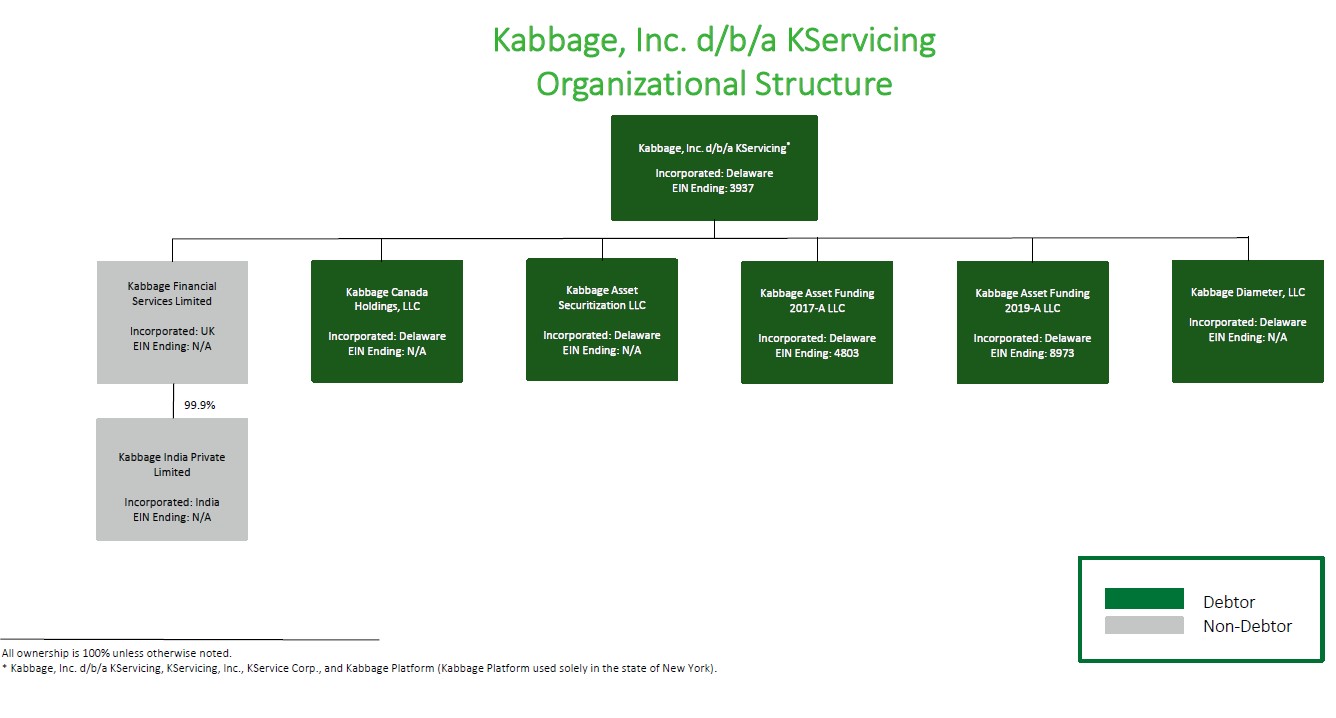

The debtor entities, now operating as KServicing, take pains in the first day declaration and a press release announcing the Chapter 11 filing to differentiate themselves from the Kabbage business that AmEx bought in October 2020. In essence, the debtor appears to be a remnant of the legacy Kabbage business—a servicer of a portfolio of PPP and other small business loans that did not travel with the rest of Kabbage into AmEx’s ownership through that 2020 transaction.

The portfolio of PPP loans, issued through the US Small Business Administration (SBA) as part of the federal government’s COVID-19 economic relief package, totals about USD 1.3bn, while Kabbage also services another USD 17m in non-PPP small business loans. Rieger-Paganis said that the USD 17m in legacy loans that Kabbage still services are all owned by Celtic Bank.

As Rieger-Paganis explains in her declaration, “The legacy entities remaining after the close of the AmEx Transaction are the Debtors in these Chapter 11 Cases. Notably, no directors or executive officers remain today from the pre-sale entity, and an entirely new leadership team and board, including independent directors, is in place today.”

Kabbage became an authorized PPP lender in April 2020, and to better partner with the SBA, overhauled its lending platform to increase automation and “expeditiously collect, analyze, verify, and approve PPP Loan applications consistent with the U.S. government’s public mandate to quickly get funds in the hands of borrowers in the midst of a pandemic,” said Rieger-Paganis. From April 2020 to September 2021, those automated systems helped the company become the second largest PPP lender in the nation, delivering more than USD 7bn in PPP loans to some 300,000 borrowers.

“As the nation witnessed the disastrous impact of COVID-19, the Company was instrumental in getting necessary funds to small businesses as quickly as the SBA desired and as a result preserved hundreds of thousands of jobs,” Rieger-Paganis said in the declaration.

Kabbage’s PPP business consisted of three categories of loans: those that the company originated and pledged to the Federal Reserve’s Paycheck Protection Program Liquidity Facility (PPPLF); those owned by partner banks Customers Bank (CUBI) and Cross River Bank (CRB) that are serviced by Kabbage; and those that Kabbage itself originated, funded and serviced for its own account.

Of what was originally a multi-billion-dollar loan portfolio, Kabbage has “successfully serviced” about 80% of the loans, meaning that borrowers either repaid the PPP loans, obtained loan forgiveness, or lenders received repayment through a federal government guaranty program, said Rieger-Paganis. As of 30 September, Kabbage is still servicing USD 541m of PPPLF loans, USD 181m of CUBI loans, USD 604m of CRB loans, and USD 2m of the loans Kabbage originated on its own.

The debt

Kabbage’s debt consists of a remaining USD 541m owed on loan advances that it pledged to the PPPLF.

Rieger-Paganis explained that the PPPLF was established in April 2020 and allowed the Federal Reserve and PPP lenders to enter funding agreements. Under the arrangement, Kabbage had to request advances from the PPPLF, which were then secured by the PPP loans that Kabbage originated using that funding.

The descent

Although Kabbage managed to successfully process more than 270,000 PPP loans, its remaining loan portfolio, about 48,000 loans as of 30 September, totaling USD 1.3bn, “has presented a number of challenges for the company,” said Rieger-Paganis.

“Initially heralded for staving off the potentially deleterious effects of COVID-19 health measures on small businesses, the now-concluded PPP faces scrutiny due to lender confusion with deciphering unclear and frequently-evolving SBA guidance, or lack thereof, limited information technology systems, and incidents of borrower misrepresentations,” the first day declaration said.

Rieger-Paganis continued, “Despite adherence to express SBA guidance, the Company is embroiled in government investigations, litigations, and stakeholder disputes related to the PPP program. The hindsight investigations and misdirected scrutiny severely hamper the Company’s ability to accomplish its mission of servicing the balance of the PPP Loans in its Loan Portfolio and have caused significant additional costs to winding down its business.”

The company’s financial wherewithal has dwindled as it has shelled out funds to deal with various investigations – including by state regulators in Massachusetts and Texas, a Congressional subcommittee and the Federal Trade Commission – and lawsuits that include an action Kabbage brought against CUBI, and a class action brought by borrowers against Kabbage, according to Rieger-Paganis.

Kabbage has spent an estimated USD 19m in 2022 on professional fees related to the various investigations and court disputes. As it enters Chapter 11 protection, Kabbage has about USD 11m in unrestricted cash on hand, and does not believe it has the resources to remain in operation long enough to service all of its remaining loan portfolio, the loans in which have maturity dates as late as 2026.

“Given the Debtors’ financial distress, they are utilizing the bankruptcy process to obtain a respite from having to constantly defend against the Disputes, to provide a single forum to address the Disputes, and to hopefully emerge in a position to complete their wind down efforts for the benefit of tens of thousands of remaining borrowers and the Debtors’ stakeholders that provided those loans to the borrowers,” Rieger-Paganis said.

The Chapter 11 case, proposed liquidation plan

Prior to entering the bankruptcy process, Kabbage attempted to negotiate settlements of various disputes with key stakeholders. The company intends to continue those discussions during the Chapter 11 case, and has already proposed a liquidation plan that lays out two potential scenarios based on the outcome of the settlement talks.

One scenario would see Kabbage continue servicing its PPP and other small business loans—either through an agreement with the Federal Reserve and partner banks CRB and CUBI to pay the costs of servicing the loans following the effective date of Kabbage’s plan, or through a transfer of the servicing rights for the loans to a third party, with the Federal Reserve or the partner banks paying the costs of making that transfer, according to Rieger-Paganis.

A second scenario under the proposed Chapter 11 plan would play out if the Federal Reserve and CUBI do not agree, during the early stages of the bankruptcy case, to a funding arrangement that would allow Kabbage to continue servicing its loan portfolio. In that situation, Rieger-Paganis said, the plan provides for a rejection of the loan servicing agreements Kabbage has with the partner banks. This plan scenario would also include Kabbage’s continuing to service the PPPLF loans until the effective date of the plan, at which point, the collateral for the company’s PPPLF debt—namely, the underlying PPP loans that Kabbage used the Federal Reserve advances to fund—would be transferred back to the Federal Reserve.

“At the time of filing these Chapter 11 Cases, the Debtors were quite close to an agreement with the Federal Reserve, and discussions with CUBI had progressed significantly in the days leading up to filing these Chapter 11 Cases,” Rieger-Paganis said. “In both scenarios, any costs associated with the transfer of servicing obligations will not be borne by the Debtors, and the Debtors will make commercially reasonable efforts to assist the Partner Banks and the Federal Reserve, as applicable, with such transfer of the Debtors’ servicing obligations to a third-party loan servicer prior to the applicable transfer date.”

The advisors

A service of

Start your trial. Today

Explore unlimited content like this, available only in the platform.

Already a client? Sign in