Restructuring experts gear up for busy 2H23 as high rates create refi plight

The long wait for a surge in restructuring activity in the US is expected to end in the coming months as leveraged borrowers and their backers come to terms with the need to fix capital structures that are unsustainable in a world of high interest rates and inflation.

Advisors and their clients are racing to figure out how to rightsize balance sheets created prior to 2022, when floating rate debt was inexpensive and financial sponsors and lenders made underwriting decisions on the expectation that companies would be sold at a premium prior to the debt maturing.

Instead of smooth sailing, benchmark rates for floating rate debt have jumped from zero to over 500bps, according to Federal Reserve data, and valuations for private market companies have reset, impeding M&A activity.

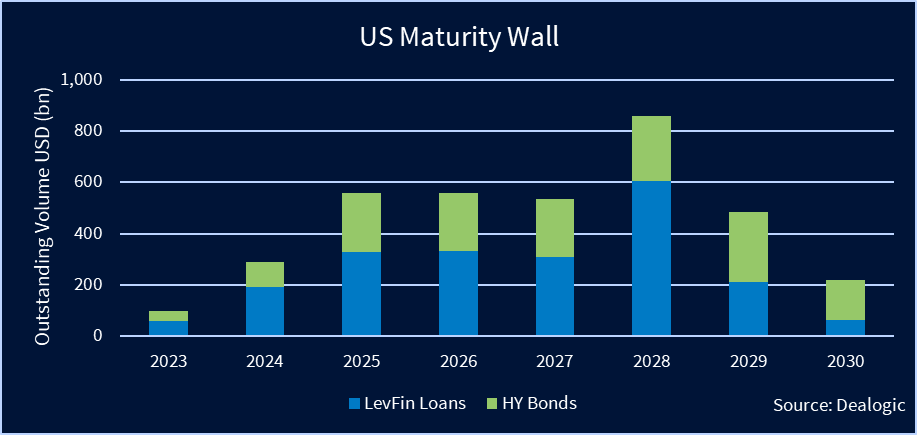

Now over USD 1.5tn in syndicated high yield bonds and loans issued by 1,264 companies matures by the end of 2026, according to Dealogic data.

While some companies will be able to refinance their upcoming debt, many first need to reduce leverage through options like raising preferred equity and buying back debt at a discount, restructuring bankers and attorneys said.

Fixed loss

“We’re talking to lots and lots of companies that have 2024, 2025, 2026 maturities, and if they had to refinance their entire capital structures today, they couldn’t afford it,” said Bill Derrough, co-head of capital structure advisory at Moelis.

Alex Stevenson, a managing director at Lincoln International, said that he is seeing an increase in companies with 2024 and 2025 maturities that don’t generate enough EBITDA to service their debt obligations at current interest rates, so refinancing the debt with traditional lenders may not be feasible.

Kroll Bond Rating Agency estimates that with benchmark rates above 5% and overall rates at 12% or more, around 16% of the 2,000 private middle market companies tracked by the credit ratings agency, that were underwritten with positive cash flow, will not be able to generate enough cash flow to cover their interest expense.

The full effect of rate increases will take some time to work its way through the market with companies feeling the impact in the second half of the year, said Bill Cox, global head of corporate, financial and government ratings at KBRA.

In the syndicated market, LoansIntel data shows that the average interest coverage for over 500 companies tracked by the independent credit research firm fell to 1.92x in 1Q23 from 2.79x in 1Q22. Around a quarter of the companies have ratios below 1.5x.

Compounding the problem, many companies are facing materially higher operating costs than originally budgeted when they issued debt, said Houlihan Lokey Managing Director Tuck Hardie.

“People describe it as a balloon. You squeeze it on one side and it’s going to pop out on the other. What’s happening now is it’s getting squeezed on both sides and it’s going to [explode],” Hardie noted.

Companies and financial sponsors have employed aggressive tactics to raise new cash to cover liquidity shortfalls. But liability management transactions have often only delayed bankruptcy filings like in the recent cases of Envision Healthcare and Diamond Sports.

Advisors said that in many cases the real solution for companies is to reduce their debt loads.

“If the company doesn’t have financial stability, it can have infinite basket capacity and that won’t make the company whole,” said Alice Eaton, deputy chair of restructuring at Paul Weiss.

Preferred alternative

Many companies are exploring raising preferred equity from either existing backers or new investors to help deleverage, several advisors said.

In recent cases, Radiology Partners has been working with Barclays to raise preferred equity as the US’s largest provider of radiology deals with declining liquidity, while industrial group BrandSafway’s sponsors have proposed injecting cash to help facilitate a refinancing of the industrial group’s USD 2.8bn first lien term loan that matures in June 2024.

Alternative credit funds, private equity funds with credit vehicles and hedge funds are providing solutions through preferred shares or holdco PIK notes, Stevenson said.

Preferred shares, unlike debt instruments, typically do not count towards a company’s leverage and can be highly customized, though the capital is costly with investors looking for ROIs that approach financial sponsors’ target returns.

Last year, struggling movie theater chain AMC Entertainment Holdings issued a new class of preferred shares to all common investors and later sold USD 110m of preferreds to Antara Capital in a transaction that also saw Antara exchange USD 100m of second lien notes due 2026 for preferreds. The investor has since started selling off the preferreds in the open market ahead of AMC’s contested plan to convert the preferred shares to its common stock.

Moelis’s Derrough said he is seeing companies couple raising preferred with a plan to buy back existing debt at a discount to take advantage of the depressed trading prices of expensive loans and bonds.

Some restructurings will require a series of transactions that will see a company raise preferred equity and then reduce leverage through the repurchase of debt and creditors agreeing to swap debt for equity, he added.

Lenders are proving largely supportive of the moves, advisors said. Ad hoc groups are approaching companies with their own ideas for how to restructure balance sheets through debt-for debt exchanges and debt-for-equity swaps, noted Simpson Thacher partner Patrick Ryan.

“There’s almost an efficient pragmatism that’s taken hold in the restructuring world,” said Ryan, who heads the firm’s global banking and credit practice. “Everyone is kind of looking at what works best for all involved constituents or what gets the best overall recovery short of a Chapter 11.”

Even so, advisors said they expect some restructuring efforts to end in bankruptcy filings, but they don’t foresee a rapid uptick in companies rushing to file.

Chapter 11 filings jumped to 127 with USD 54bn in total liabilities in 1H23 compared to 77 cases with USD 26bn in liabilities in 1H22, according to Debtwire data that tracks cases with over USD 10m in liabilities.

“I don’t think it will be one big wave. It will be a constant flow as companies work through their maturities and capital structure needs,” said Paul Weiss’s Eaton.

Simpson Thacher’s head of restructuring, Sandy Qusba, said Chapter 11 cases for middle market companies will likely increase as smaller firms struggle to access capital markets.

“This is not like a crazy, crazy hot market, but it’s a busy market and there are a lot of cases out there. I don’t see this changing. I see 2024 being very similar to 2023, strong and steady,” added Michael Eisenband, global co-leader of the corporate finance and restructuring segment at FTI Consulting.

A service of

Start your trial. Today

Explore unlimited content like this, available only in the platform.

Already a client? Sign in