Pension funds, former employees, and to-be-chosen DIP lender are primed to drive Yellow’s Chapter 11 cases

Since filing its bankruptcy petition, Yellow Corporation has signaled that it intends to use Chapter 11 to sell its assets and wind down. In its first day bankruptcy hearing, the company’s counsel expressed optimism that they “don’t think the secured debt is the fulcrum” because an asset sale would more than satisfy all funded debt claims and there would be “material proceeds” for unsecured creditors. If the debtors are correct, the focus of the bankruptcy cases is likely to turn to recoveries for the debtors’ employees and its general unsecured creditors. This, in turn, raises questions as to how significant claim pools, such as Worker Adjustment and Retraining Notification (WARN) Act claims and claims arising from the debtors’ wage, benefit and pension obligations could impact recoveries for general unsecured creditors.

In this article, the first of a three-part series, the Debtwire legal analyst team provides an overview of Yellow’s run-up to bankruptcy, identifies some of the parties who might play major roles in the bankruptcy cases and discusses how the Chapter 11 cases might unfold. In later installments Debtwire will examine the WARN Act claims that have been asserted in several class action lawsuits, as well as pension and other employee-related claims. We will also discuss where those claims might sit in the distribution waterfall and how recoveries for unsecured creditors could be impacted.

Company background

Yellow is a less-than-truckload (LTL)[1] carrier based in Nashville, Tennessee. According to the first day declaration (First Day Declaration) of Yellow’s Chief Restructuring Officer, Matthew Doheny, the company was founded in the 1920s as a freight carrier. After a period of deregulation in the 1980s, the company expanded in the early 2000s by acquiring other carriers. Before entering bankruptcy, Yellow operated several trucking brands – Holland, New Penn, YRC Freight and Reddaway (Opcos). The company also has an independent, non-union operating subsidiary third-party logistics (3PL) solutions provider, Yellow Logistics (Logistics), which operates six warehouses and provides outsourced storage, transportation and fulfilment services. Yellow was the third largest LTL freight carrier in the country and generated more than USD 5.2bn in operating revenue in 2022, says Doheny in his declaration.

Source: First Day Declaration

According to Doheny, prior to its bankruptcy filing Yellow was the largest union carrier in the country. Doheny said that before the layoffs, on 27 July, the company employed nearly 30,000 people, approximately 22,000 of whom are members of the International Brotherhood of Teamsters (IBT). OpCos YRC Freight, USFHolland, and New Penn, are parties to a National Master Freight Agreement, which is a collective bargaining agreement (CBA) with several local teamsters unions (Local Unions) that expires on 31 March 2024.

Capital structure: the US Treasury comes to Yellow’s aide during the COVID-19 pandemic

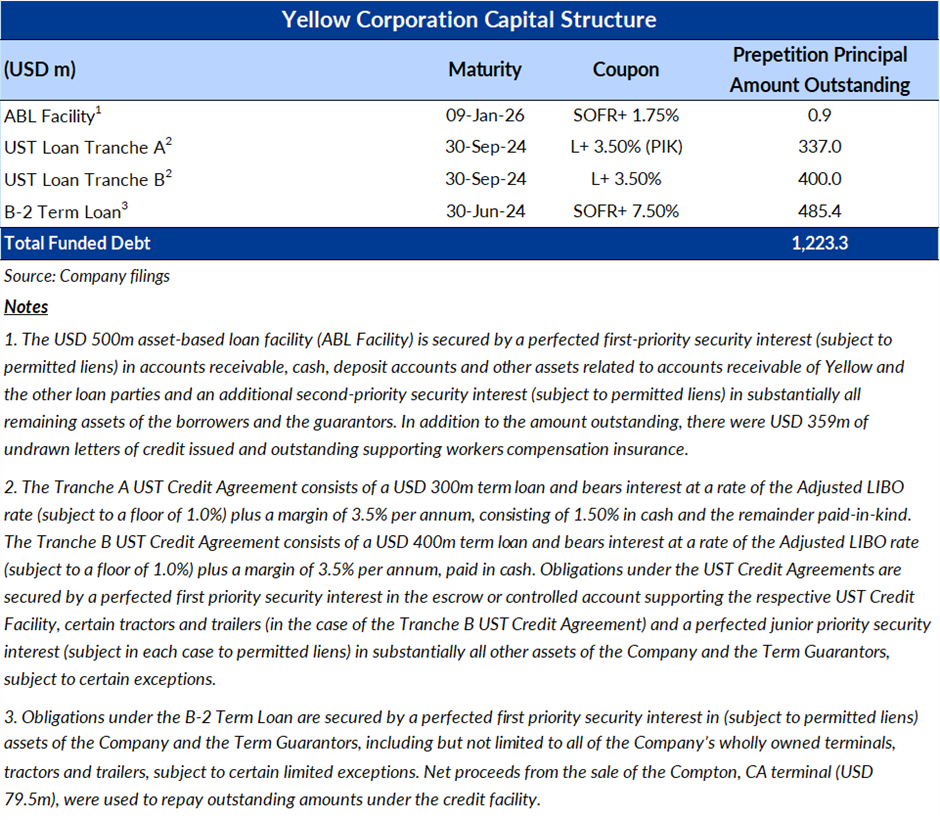

Yellow has approximately USD 1.223bn in outstanding funded debt, including a private B-2 term loan, two government term loans and an asset-based loan (ABL) facility. The B-2 term loan is a USD 600m facility that was issued by Apollo Global Management, LLC (Apollo) as lead lender, with Alter Domus as administrative agent. As discussed below, it has been reported that the loan has recently been purchased by Citadel Credit Fund. It matures on 30 June 2024.

During the COVID-19 pandemic, in July 2020, Yellow received two Coronavirus Aid, Relief and Economic Security (CARES) Act secured loans from the US Treasury for a total of USD 700m (Treasury Loans). Yellow borrowed the funds in separate Tranche A and Tranche B loans of USD 300m and USD 400m, respectively. They mature on 30 September 2024. According to Yellow’s 2022 Form 10-K (2022 10-K) as part of the consideration for the Treasury Loans, Yellow issued 15,943,753 shares of common stock to the US Treasury, which upon issuance had a fair value of USD 46.7m and constituted approximately 29.6% of Yellow’s common stock on a fully diluted basis. In its bankruptcy petition, Yellow states that the US Treasury currently holds 30.6% of the company’s shares.

Yellow also has an ABL facility arranged by Citizens Bank, Merrill Lynch, Pierce, Fenner & Smith,and CIT Finance LLC (ABL Facility). Yellow and the OpCos are borrowers under the facility, which is guaranteed by other subsidiaries. It has a maturity date of 9 January 2026, with a springing maturity 30 days prior to the maturity of the Apollo Loan or the Treasury Loans.

Yellow’s capital structure as of the petition date is summarized below:

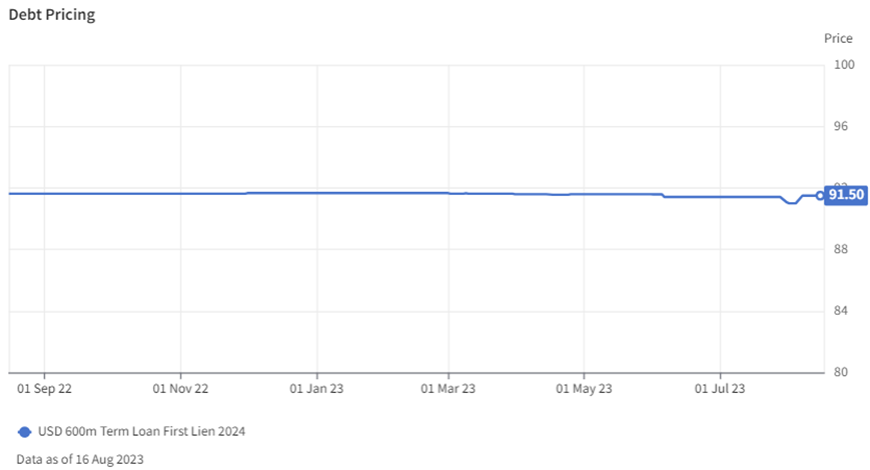

Yellow saw a steady decline in its stock price in the run-up to its bankruptcy filing. The company’s shares fell from USD 6.78 as of 17 August 2022 to as low as USD 0.57 as of closing on 27 July 2023 before climbing back to USD 2.48 per share on 7 August. As of 16 August, the shares had fallen back down to USD 1.10. In contrast, the pricing of the B-2 term loan has held relatively steady during the past couple of years, with a price of USD 91.63 on 16 July 2022 and USD 91.5 on 16 August 2023:

Source: Debtwire

The company’s pension plans

Yellow’s non-union and union employees participate in separate pension plans. The company states in its 2022 10-K that it sponsors three single-employer defined benefit pension plans for approximately 4,600 current and former non-union employees. The plans were closed to new participants as of January 2004 and benefit accruals were frozen as of July 2008. According to the 2022 10-K, as of 31 December 2022 the plan was underfunded by USD 97.6m. The company said that it expects cash contributions to be nominal for 2023 and the following years, “if required at all.”

According to the 2022 10-K, the company also contributes to several multi-employer pension plans for the 82% of its now former employees who are covered by CBAs, which determine the amount of the contributions. Those plans are not directly managed by the company and those assets and liabilities are not included in the company’s balance sheets. The multi-employer plans in which the debtors participated as of 31 December 2022 that the company labelled “individually significant” are the (i) Central States, Southeast and Southwest Areas Pension Fund (Central States Fund), (ii) the Teamsters National 401(k) Savings Plan, (iii) the Road Carriers Local 707 Pension Fund, and (iv) the Teamsters Local 641 Pension Fund. The debtors state in their 2022 10-K that the company contributed USD 111.5m to these plans in 2022, with USD 63m of that sum going to Central States and USD 21.7m to the Teamsters National 401(k) plan. In the 2022 10-K, the company notes that if it fails to make its required contributions to the plans it would be exposed to penalties, including withdrawal liabilities.

“One Yellow” and disputes with the International Brotherhood of Teamsters

Doheny says in his declaration that Yellow devised a plan called “One Yellow” that was aimed at integrating the operations of four of the company’s OpCo subsidiaries to eliminate inefficiencies and to create a super-regional company that would operate as “one company, one network, under one Yellow brand.” The company projected that the One Yellow project could result in up to USD 675m in additional annual revenue or 13.5% of the company’s revenue. According to Doheny, “the very survival of Yellow depended on completing One Yellow as soon as possible.”

Doheny also notes in the First Day Declaration that the company launched phase 1 of the One Yellow project in September 2022 and planned to implement phase 2, which contemplated a restructuring of 70% of the company’s network by the end of 2022. However, the company was prevented from implementing these changes by the IBT and the Local Unions, says Doheny. In a complaint filed in federal court in Kansas (IBT Litigation), the company alleges that the Local Unions breached the CBA by refusing to participate in change of operations hearings and by making any union approval of the operational changes contingent upon wage increases. The complaint further says that IBT, while not a party to the CBA, instigated, supported and ratified the unions’ breaches. Yellow seeks damages of USD 137m in lost savings and liquidity due to the delay in implementing the changes, and USD 1.5bn for loss of enterprise value due to the company’s liquidation. The unions and the IBT have filed a pending motion to dismiss in which they argue that the proposed changes violated the terms of CBA and “effectively gutt[ed]” it.

Yellow’s trouble with the unions was not limited to operational change disputes. On 18 July, the IBT announced that Yellow had failed to make a USD 50m contribution to the Central States Fund and that the latter’s board of trustees had voted to suspend health care benefits and halt pension accruals for Yellow employees, effective 23 July. On 19 July, the Central States Fund filed a complaint against Yellow and Opco Holland in the US District Court for the Northern District of Illinois seeking separate awards of approximately USD 4.3m in unpaid pension contributions, compelling the payment of future contributions and seeking to recover approximately USD 18.2m in unpaid health fund contributions.

In response to the failure to make payment, the IBT threatened a strike. Doheny says that the threatened strike caused the company’s individual shipments to drop from 40,000 to “near zero” over a four-day period. Although at the last minute IBT had Central States agree to defer the contributions for 30 days, thereby averting the strike, the action was “too little, too late” and the threatened strike had “sealed Yellow’s fate,” Doheny says.

According to the First Day Declaration, Yellow discontinued accepting new shipments the week of 24 July. In their first day motion to pay wages and employee benefits, the debtors state that by 2 August they had terminated all but 1,650 go forward employees who will help with the wind down. The company filed its bankruptcy petition on 6 August and is poised to continue these disputes in Chapter 11.

What could the Chapter 11 case look like?

DIP lending competitors

Given the factual complexities noted above, Yellow may not have a smooth trip through Chapter 11. One interesting development at the outset of the Chapter 11 cases has been the emergence of several parties who are vying to be DIP lender. The prepetition lenders led by Apollo originally offered a USD 142.5m debtor-in-possession (DIP) loan, which came with a USD 501.5m rollup of the prepetition B-2 term loan facility and a pricey 17% interest rate. It also set a short 90-day time frame for the sale of the company’s assets. However, on 15 August, it was reported that the Citadel Credit Fund purchased the loan after other bidders emerged on the scene who were willing to offer better DIP terms.

Prior to Yellow’s bankruptcy filing, hedge fund MFN Partners Management, LP (MFN) purchased 22,067,795 shares of the company’s common stock, representing 42.5% of the total common shares. At Yellow’s first day hearing it was revealed that MFN had offered to make a competing DIP loan, but at a cheaper interest rate and with a longer sale runway of 180 days. Originally proposed as a loan that would be pari passu with the DIP facility, MFN subsequently offered a junior loan. MFN’s interest in Yellow’s assets may be strategic as well as financial, given that it’s counsel, Dennis Dunne of Milbank, stated at the hearing that the fund also is the largest shareholder in Yellow’s former competitor, transportation logistics manager company XPO, Inc.

In addition, in what could be preparations for a possible credit bid, Patrick Nash of Kirkland & Ellis stated at the first day hearing on behalf of the debtors that a second party, LTL and truckload company Estes Express Lines, had offered a junior DIP loan.

Unsecured creditors’ committee

The DIP loan battle might hit more traffic now that the official committee of unsecured creditors (UCC) has been appointed. Yesterday, 16 August, the US Trustee announced that it had appointed a very large nine-member UCC, which may weigh in on the competing DIPs. But it’s not just the DIP loan that the UCC will weigh in on. Reflecting the importance to the bankruptcy cases of employee-related claims, the majority of the members on the UCC represent employee interests – the IBT, the Central States Fund, the New York State Teamsters Pension and Health Funds, the Pension Benefit Guaranty Corporation (PBGC) and a WARN Act class action plaintiff, meaning that the committee is likely to play an active role on the employee and pension issues noted above. The other four members of the UCC are trade creditors.

As will be discussed in later installments of this series, pension claims, and sometimes WARN Act claims, can be among the largest unsecured claims in a bankruptcy case. If Yellow or the PBGC terminate Yellow’s single-employer pension plans, the PBGC will be able to assert a claim for any underfunding of the plans. In addition, if the debtors withdraw from their multiemployer plans (such as the Central States Fund) they could face substantial withdrawal liability claims.

Sale of assets “free and clear” of pension and other liabilities

The complexities don’t end there for the UCC or the debtors. In a motion for a temporary restraining order (TRO) filed by Yellow in the IBT Litigation prior to the bankruptcy filing, the company warned that if it could not get TRO relief it would be “forced into a Chapter 7 liquidation.” However, Yellow subsequently changed course, and instead filed a Chapter 11 petition, together with a DIP motion seeking approval of a USD 142.5m DIP facility, as well as a motion to approve bid procedures to sell substantially all of its assets in one or more transactions. At Yellow’s first day hearing Nash emphasized that there is “no prospect of a going concern sale.” However, Doheny says in his declaration that if the company’s portfolio of real estate and equipment is sold at their appraised values, the proceeds “would exceed the aggregate amount of Yellow’s prepetition secured debt and the DIP facility.”

One business unit that may be particularly attractive to purchasers is the company’s Logistics subsidiary. Prior to the bankruptcy, on 28 July, Yellow issued a press release stating that it was “exploring options” and was in talks with “multiple prospective bidders” for the sale of Logistics, which the company said is one of the “fastest growing 3PLs in the industry.” Although Logistics’ employees are 100% non-union, it would still be liable for the pension obligations of each member of Yellow’s “controlled group,” which includes subsidiaries in which a parent corporation owns at least an 80% share, because it is a 100% owned subsidiary of Yellow.

A sale of some or all of Yellow’s assets pursuant to Bankruptcy Code section 363 could allow a purchaser to take them “free and clear” of all claims, including pension liabilities, with the company using the proceeds to pay creditors and wind down the debtors’ estates.[3] A debtor can sell assets free and clear of liens if the sale price is greater than the aggregate value of all liens on the property. In addition, a secured lender may credit bid its claim, that is it can offset its claim against the sale price.[4]

Other potentially attractive assets are the company’s real estate and tractors/trailers. Yellow’s 2Q23 report states that as of 30 June the book value of the company’s property and equipment was approximately USD 1.14bn. Doheny states in the First Day Declaration that Yellow’s real estate portfolio is “substantial” and consists of “hundreds of owned and leased properties.” According to the company’s 2022 10-K, Yellow owned 166 of the 308 service facilities that it operates. Some of Yellow’s terminals have been sold for significant value. The company reported in its 2022 10-K that it sold one terminal in 4Q22 for approximately USD 31m. In 2Q23 the company closed on a sale of its terminal in Compton, California for USD 80m. In addition to real estate, the company has significant personal property assets. In its 2022 10-K, Yellow said that as of 31 December 2022 it owned approximately 11,700 tractors and approximately 34,800 trailers.

In their bidding procedures motion, the debtors proposed a bid deadline of 15 October and an auction deadline of 18 October. Those dates reflect the milestones in the now-defunct Apollo DIP proposal. It remains to be seen whether these deadlines will be modified by the party that becomes DIP lender. If the ultimate DIP lender intends to credit bid its loan, it is possible that they will want to keep the sale on the same tight time frame to maximize their chances of success at auction. Whatever the milestones, the debtors will have a lot of parties to contend with in any sale process including potential bidders, the UCC, lenders, other employee and pension representatives and the US Trustee, among others.

IBT Litigation to enhance recoveries

These parties will no doubt be evaluating the IBT Litigation as well as the case progresses. Indeed, another question here is whether Yellow will proceed with its litigation with the IBT and the Local Unions now that it has filed for bankruptcy. Although an award or settlement could meaningfully augment the bankruptcy estate and the funds available for distribution to creditors, the likelihood that Yellow will succeed is far from clear. The IBT has moved to dismiss the case, arguing that Yellow and the OpCos failed to exhaust mandatory grievance procedures under the CBA before filing the lawsuit and that plaintiff Yellow, which is not a party to the CBA, can’t sue to enforce it. The IBT also argues that the complaint should be dismissed because Yellow fails to allege that IBT actually violated the agreement. The uncertainty surrounding the litigation at this early stage in the case makes it difficult to value Yellow’s claims. If the case is not settled or litigated to conclusion prior to the confirmation of any Chapter 11 plan, the debtors could propose to create a litigation trust, funded with sale proceeds, that would prosecute the claims to conclusion.

Final thoughts

It will be interesting to see who wins the DIP bidding war and whether the loan will be a financial investment or a strategic loan that could be a predicate to a credit bid. Today (17 August) at 1pm ET, Debtwire will live blog a hearing where Yellow will either seek approval of a consensual interim DIP financing proposal or hold a status conference to discuss ongoing DIP negotiations.

Ultimately, the choice of lender could influence bid terms such as the sale time frame and the amount of break-up fees. This, in turn, could impact the price that the debtors receive for their assets. And if the sales proceeds are sufficient to satisfy the secured debt claims, the debtors’ current and former employees and the pension funds will vie for the remaining proceeds. In the next two installments of this series, Debtwire will discuss the claims that those employees might bring and the relative priorities that those claims may have.

A service of

Start your trial. Today

Explore unlimited content like this, available only in the platform.

Already a client? Sign in