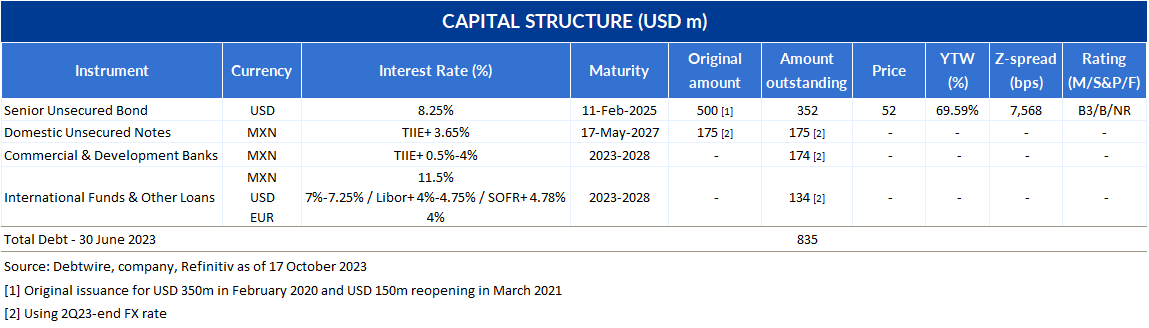

Operadora Mega Special Credit Report – …and an exchange offer it is!

We said in Part II of our Operadora Mega 2Q23 Credit Report that we saw a Findep-like exchange offer as the most likely option for the Mexican non-bank financial institution (NBFI) to address the maturity of its international bonds due 2025. And that possibility has become a reality, as the company has just launched such a deal (even before we were expecting it, as we had in mind a transaction in early 2024).

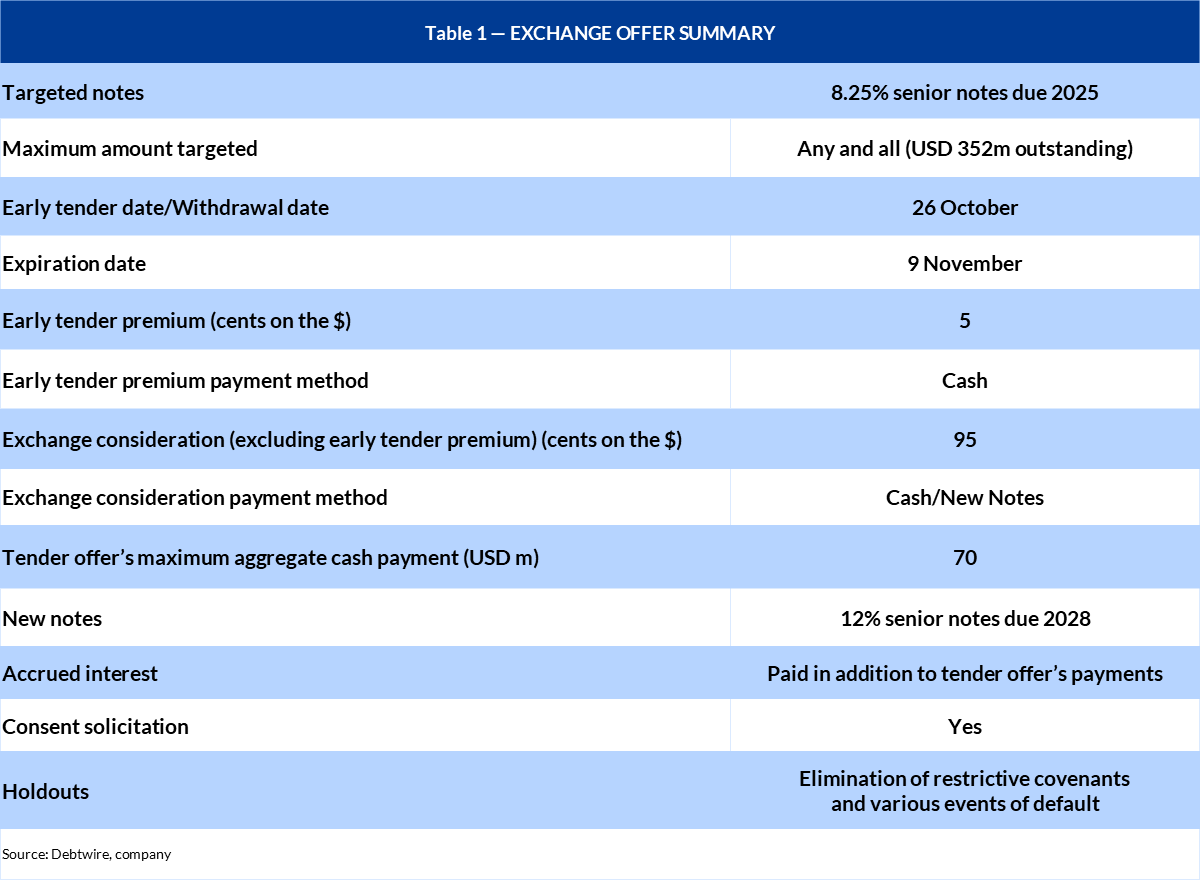

The offer, as we expected, highly resembles the one carried out by peer Findep in January of this year, with a partial repayment in cash and new notes that extend the maturity by five years. The most significant difference, probably, is the interest rate to be borne by the new notes, which will increase the existing coupon by 375bps straight away (compared to Findep’s step-up coupon – a 200bps initial increase followed by a subsequent 200bps raise).

If the bonds are tendered by the 26 October early deadline, the total consideration will be equal to par. Table 1 provides a summary of the exchange offer’s main terms.

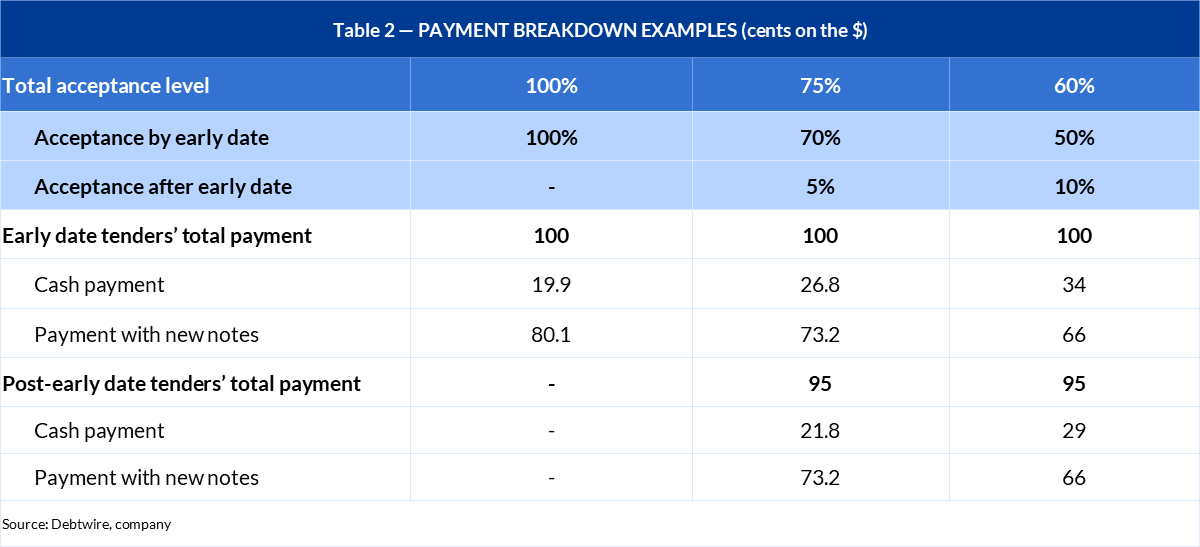

Since the aggregate cash payment offered by the company is capped at USD 70m (with the cash payment on the accrued interest coming in addition to that amount), the portion that would be repaid in cash depends on the total tender level. Furthermore, while the five cents-on-the-dollar early tender premium will be paid in cash in all cases, the total cash repayment to be received by holders tendering their notes will also depend on whether the tenders made by the rest of the holders happen before or after the early date (for instance, a total tender level of 100% doesn’t result in the same outcome if all is tendered by the early date or if only half of that percentage comes before and the other half after).

For this reason, the deal’s announcement included three examples of potential scenarios, and the resulting payment breakdowns. For the sake of simplicity (and because they seem reasonable), we’re going to use them, and a summary can be found in Table 2.

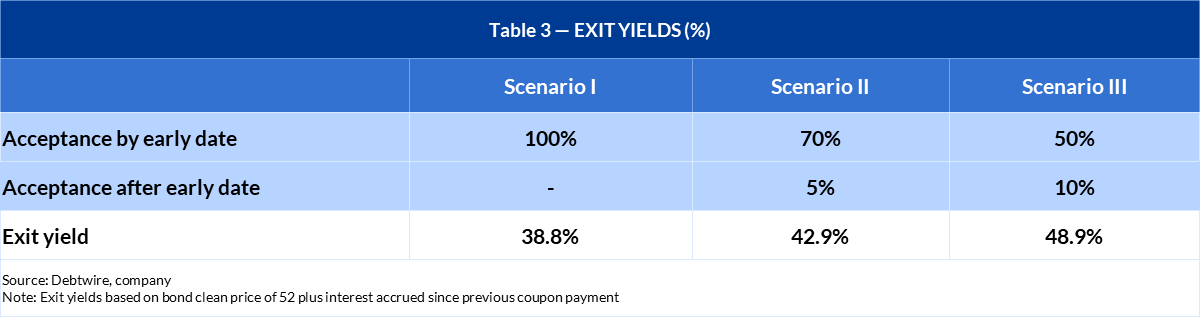

At current market prices for the bonds, and with the exact terms of the exchange offer now in hand, an analysis of the net present values (NPVs) under those three scenarios shows yields of between 38.8% and 48.9% (See Table 3).

As we indicated in the 2Q23 Credit Report (Part II), we consider a level of tenders of around two-thirds of the amount outstanding as highly feasible (although we would assume almost all the tenders would come prior to the early tender deadline), so the intermediate scenario (scenario II) presented by the company could be a good approximation for the exit yield.

The launch of an exchange offer with a partial cash component seems to validate our previously stated view of a strategy based on a division of the bullet payment currently scheduled for February 2025 into more gradual and manageable payments.

However, we reiterate that, while this strategy reduces the refinancing risk, it doesn’t eliminate it completely.

Moreover, we need to stress the fact that the terms of the new notes announced now (with a straightaway coupon increase, instead of the step-up structure we had included in our previous estimates) will put additional pressure on the company’s liquidity going forward.

A service of

Start your trial. Today

Explore unlimited content like this, available only in the platform.

Already a client? Sign in