MSU Energy Special Credit Report – Big bond, big potential return

The last two years have not brought the steep delevering that MSU Energy was hoping for, but the Argentine generator has made some progress. Net leverage has remained at 5x over the last two years, but that is because MSU paid down commercial debt. Although net debt only decreased by USD ~40m, commercial debt has been reduced from as high as USD 173m in 4Q20 to USD 26m today. The primary reasons for the slow deleveraging were capital controls, central bank restrictions, unrealized margin on gas procurement which shifted back to Cammesa and lower dispatch associated with higher diesel oil utilization.

MSU Energy had originally guided dispatch rates of 75%. It achieved this in 4Q20 and came close during 1Q21, 2Q21 and 3Q21. Since then, however, it has dropped significantly, to ~50%. Each 1pp of extra dispatch represents USD 0.6m in incremental EBITDA per year. If we add up the totals between 1Q21 and 1Q23, inclusive, we have USD 28m in incremental EBITDA the company didn’t earn.

The lower dispatch doesn’t seem to be MSU’s fault. It resulted from a combination of factors, staring with decreasing natural gas imports from Bolivia making CAMMESA allocate production to other plants. Then, high LNG prices caused higher diesel fuel utilization, and more recently, improved hydroelectric power conditions increased Argentine hydroelectric generation and made imported hydro power from Brazil more affordable.

Our expectation, now that the Vaca Muerta pipeline is close to being completed (at least the first stage, which brings the natural gas from Vaca Muerta, in Neuquen, to Buenos Aires) is that MSU’s, as well as many other plants, will be able to increase dispatch.

In addition, in a previous report, we noted the delays in payment terms by CAMMESA. The government market administrator paid the March invoice with an average term of 83 days, which is a significant improvement from the 102 days it took to pay December’s. That itself represents USD 12m less in working capital needs (See Figure 1).

With MSU’s 2025 bonds yielding over 30% at current prices of around ~70, we will later show that under “reasonable” exit yields, the upside of buying the bonds at this level and participating in an exchange is very high.

Does the company need to keep refinancing maturities in 2023? And in 2024?

If things continue as they are today, we don’t expect MSU Energy to have difficulties servicing the remaining debt maturities in 2023, that is, without the need to refinance them. On the asset side, we have USD 31m in cash as of 1Q21, and, let’s assume, nine months of EBITDA (USD ~120m being conservative), which will be used to repay USD 105m in maturities (USD 25m already paid in May), plus USD ~15m in capex, plus USD 38m in interest expense (USD 8m already paid). So, the company would be basically flat (including improvement in CAMMESA payment terms to 83 days), but if CAMMESA keeps improving its payment terms and dispatch is a little higher, maybe they can pull it off.

For 2024, there is USD 101m in maturities, USD 48m in interest expense and less than USD 10m in capex. These numbers mostly match an annual EBITDA of USD ~160m (again, bearish scenario) (See Table 1).

What to expect in an exchange?

If Argentina’s presidential elections in October-November result in an opposition win, as is widely expected, probably many companies, including MSU Energy, will be able to refinance debt maturities at better rates than today. After the final payment of the secured 2024 bonds in February 2024, the company can probably refinance the USD 600m 2025s into an amortizing 5-6 year bond (later, we’ll try to calculate how fast it could repay it) like most companies are doing. If tailwinds are strong, it could try to keep as much money as possible in case it has attractive project in its pipeline, or even get new money. Below, we present the more bearish scenario, but more benevolent outcomes include the refinancing of part or all of – or even increasing – domestic indebtedness and faster repayment of the international bonds.

MSU Energy will have a very, very tight situation in the next six quarters, with inflows matching outflows almost perfectly.

Although we expect MSU to refinance the 2025 bonds earlier, if it doesn’t, by the end of 2024 we would only have USD 600m of the 2025s and USD 160m in EBITDA (again, under a bearish scenario) for 2025, 2026 and 2027, and then EBITDA would drop to USD 110m starting in 2028, as the first 450MW of PPAs expire.

Under a pessimistic scenario where dispatch continues to be low, as it is today, in which EBITDA is USD 110m after 2027, the company would be debt-free by 2030. If we assume EBITDA levels of USD 180m through 2027 and USD 120m afterwards, MSU Energy could repay it in 2029.

As mentioned above, if domestic debt gets rolled over (entirely or in part), which has a very high probability of occurrence, there would be a cash portion in the exchange and repayment could even arrive early (ie 2028).

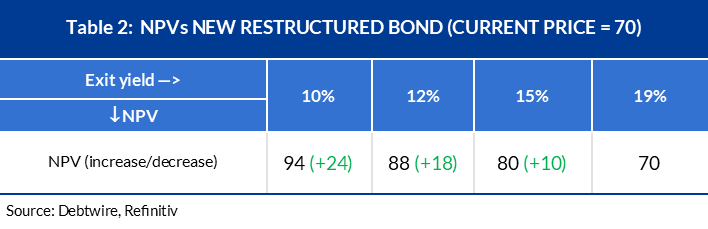

NPVs

We calculated a simple NPV assuming a scenario of 6.875% coupons until February 2025, and then 9% until 2030 (in the bearish EBITDA scenario). The exit yield that would make the trade neutral from current trading prices (of 70) we calculated to be 19%.

In a country with improved prospects and a company with such a simple capital structure and clear prospects, however, we believe 19% is too high and it should probably trade lower. Obviously “lower” is a very ambiguous word, but if the exit yield were to be 15%, the NPV would be 80 (10 points above the current trading price), if it were 12%, we would be at 88 (~18 points above) and if it were 10%, 94. All of these are very attractive scenarios for a potential investor.

A service of

Start your trial. Today

Explore unlimited content like this, available only in the platform.

Already a client? Sign in